Yen’s weakness is currently a clearer development in the rather indecisive markets. Germany and UK benchmark yields are extending near term rally while US 10-year yield stands firm above 3.7%. On the other hand, 10-year JGB yield is still capped by BoJ imposed ceiling. Dollar is mixed for now after traders refused to commit over yesterday’s CPI data. On other hand Sterling looks ready to ride on any upside surprise in today’s consumer inflation data. A question is whether the Pound’s rally, if happens, could take Euro and Swiss higher, or pressured them.

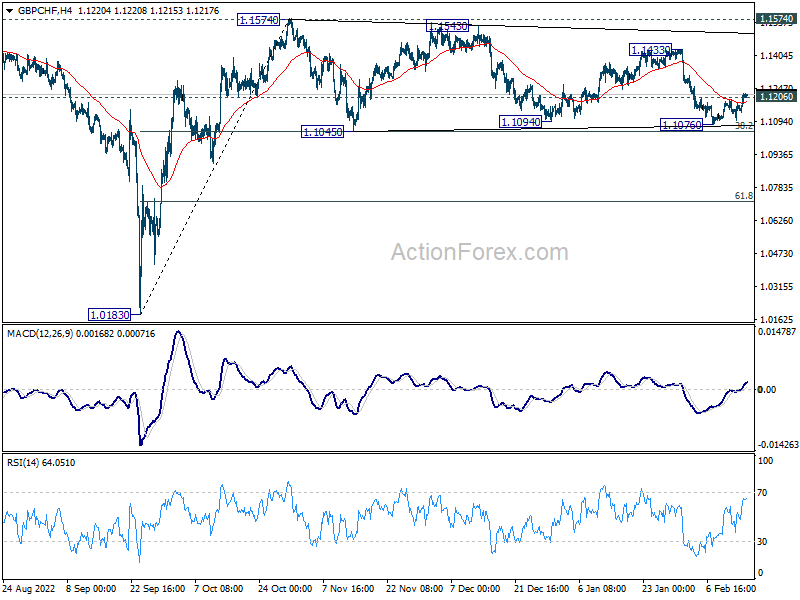

Technically, GBP/CHF is making some progress in breaking 1.1206 minor resistance. Upside acceleration today would add to the case that whole corrective pattern from 1.1574 has completed. 1.1433 resistance should be the next target. Firm break there will set the stage to resume larger rally from 1.0813 through 1.1574 later in the month. Let’s see how it goes.

In Asia, Nikkei closed down -0.42%. Hong Kong HSI is down -1.51%. China Shanghai SSE is down -0.47%. Singapore Strait Times is down -1.06%. Japan 10-year JGB yield is down -0.007 at 0.503. Overnight, DOW dropped -0.46%. S&P 500 dropped -0.03%. NASDAQ rose 0.57%. 10-year yield rose 0.044 to 3.761.

Fed Harker: It’s going to be above 5%

Philadelphia Fed President Patrick Harker commented on yesterday’s inflation report and said “it was good and it was moving down, but not quickly.” He added that FOMC will have to “let the data dictate” tightening, and, “It’s going to be above 5% in the Fed funds rate. How much above 5? It’s going to depend a lot on what we’re seeing.”

“In my view, we are not done yet… but we are likely close,” he said. “At some point this year, I expect that the policy rate will be restrictive enough that we will hold rates in place and let monetary policy do its work,” he noted in a prepared speech”.

“Rates are now at a level that allow us to slow down and proceed cautiously and, to my mind, the days of us raising 75 basis points at a time have surely passed,” Harker said. “Just at the last meeting, I voted for a hike of 25 basis points — what some would call slow but actually is closer to cruising speed when it comes to tightening.”

Fed Williams: We need all the gears turning at the right pace

York Fed President John Williams said yesterday, “We will we stay the course until our job is done… We must restore balance to the economy and bring inflation down to 2 percent on a sustained basis.”

“We need all the gears turning at the right pace to restore balance between demand and supply in the entire economy,” said Williams. “We still have some way to go to achieve that goal.”

He expects core inflation, as measured by core PCE reading at 4.4% in December, to fall to 3% this year and then 2% over the next few years. Growth will likely slow to just 1% this year, with unemployment rate to rise to between 4% and 5%.

RBA Lowe: I don’t think we’re at the peak of interest rate yet

RBA Governor Philip Lowe said in a Senate hearing, “I don’t think we’re at the peak (on interest rate) yet, but how far we have to go up I don’t know.” He noted that inflation, which is currently sitting at 7.8%, was still “wage too high”. Unemployment would need to rise before there were any major changes to inflation.

“I understand why some people focus on the risks on the one side, but we’ve got to be attentive to the risk from higher inflation,” Lowe warned. “It’s corrosive for the economy. And all the evidence is if inflation stays high for too long, expectations adjust and that leads to higher interest rates and more unemployment..”

“The risks are two sided, and we’re trying to navigate our way through a narrow path.”

Looking ahead

UK inflation data is the major focus in European session, with CPI and PPI featured. Eurozone will release trade balance and industrial production.

Later in the day, US retail sales will take center stage, and Empire State manufacturing, industrial production, NAHB housing index and business inventories will be featured. Canada will release housing starts, manufacturing sales and wholesale sales.

USD/JPY Daily Outlook

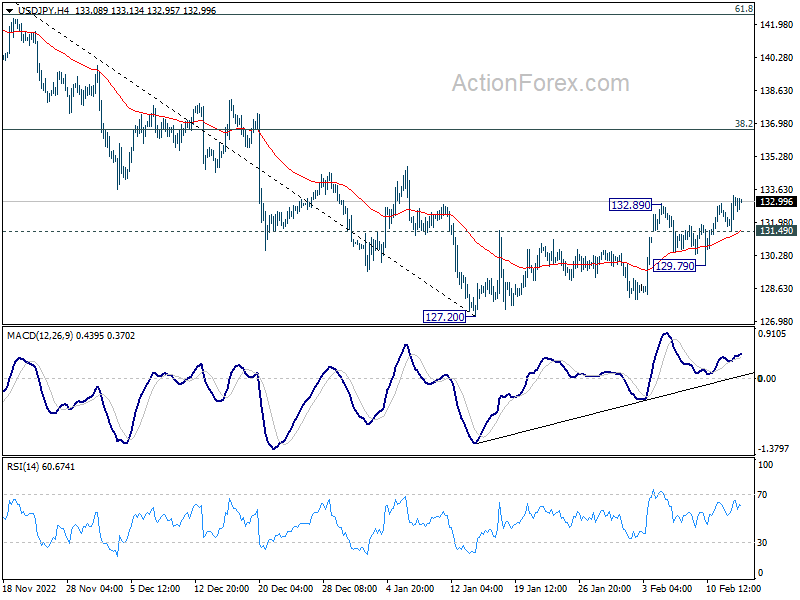

Daily Pivots: (S1) 131.97; (P) 132.65; (R1) 133.77; More…

Intraday bias in USD/JPY stays on the upside at this point. Rebound from 127.20 short term bottom should extend to 38.2% retracement of 151.93 to 127.20 at 136.64, even as a correction to the decline from 151.39. On the downside, break of 131.49 minor support will turn intraday bias neutral again first.

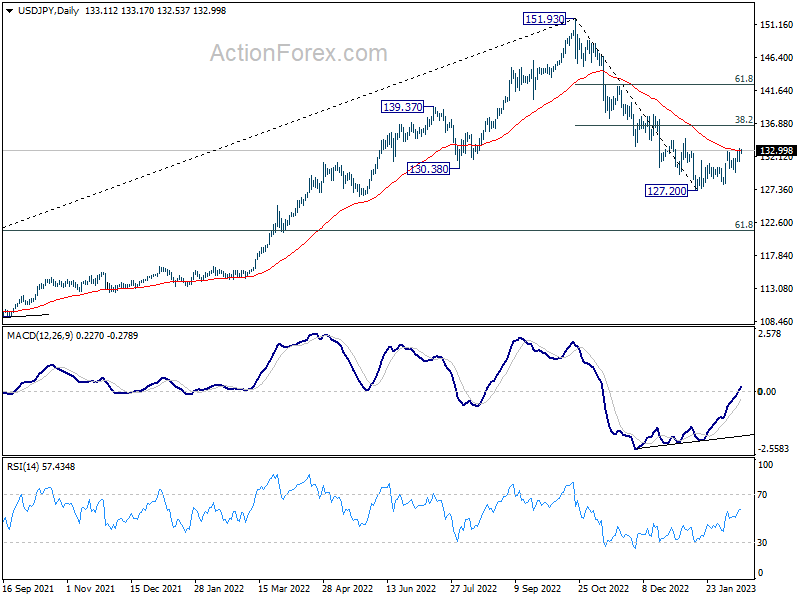

In the bigger picture, prior of 55 week EMA (now at 131.47) raises the chance of medium term bearish reversal, but that’s not confirmed yet. Strong rebound from current level, followed by sustained break of 38.2% retracement of 151.93 to 127.20 at 136.64 will argue that price actions from 151.93 is merely a corrective pattern. However, rejection by 136.64 will solidify medium term bearishness for 61.8% retracement of 102.58 to 151.93 at 121.43 and 38.2% retracement of 75.56 to 151.93 at 122.75.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Dec | -0.40% | 0.00% | -0.20% | 0.10% |

| 07:00 | GBP | CPI M/M Jan | -0.40% | 0.40% | ||

| 07:00 | GBP | CPI Y/Y Jan | 10.30% | 10.50% | ||

| 07:00 | GBP | Core CPI Y/Y Jan | 6.20% | 6.30% | ||

| 07:00 | GBP | RPI M/M Jan | 0.10% | 0.60% | ||

| 07:00 | GBP | RPI Y/Y Jan | 13.20% | 13.40% | ||

| 07:00 | GBP | PPI Input M/M Jan | 0.80% | -1.10% | ||

| 07:00 | GBP | PPI Input Y/Y Jan | 15.40% | 16.50% | ||

| 07:00 | GBP | PPI Output M/M Jan | -0.20% | -0.80% | ||

| 07:00 | GBP | PPI Output Y/Y Jan | 14.40% | 14.70% | ||

| 07:00 | GBP | PPI Core Output M/M Jan | 0.70% | 0.10% | ||

| 07:00 | GBP | PPI Core Output Y/Y Jan | 11.90% | 12.40% | ||

| 10:00 | EUR | Eurozone Trade Balance (EUR) Dec | -16.0B | -15.2B | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | -0.80% | 1.00% | ||

| 13:15 | CAD | Housing Starts Jan | 252K | 249K | ||

| 13:30 | CAD | Manufacturing Sales M/M Dec | 0% | |||

| 13:30 | CAD | Wholesale Sales M/M Dec | 0.50% | |||

| 13:30 | USD | Empire State Manufacturing Index Feb | -15.6 | -32.9 | ||

| 13:30 | USD | Retail Sales M/M Jan | 1.70% | -1.10% | ||

| 13:30 | USD | Retail Sales ex Autos M/M Jan | 0.90% | -1.10% | ||

| 14:15 | USD | Industrial Production M/M Jan | 0.40% | -0.70% | ||

| 14:15 | USD | Capacity Utilization Jan | 79.00% | 78.80% | ||

| 15:00 | USD | NAHB Housing Market Index Feb | 37 | 35 | ||

| 15:00 | USD | Business Inventories Dec | 0.40% | 0.40% | ||

| 15:30 | USD | Crude Oil Inventories | 2.4M |

{kind=link}