Australian Dollar is leading other commodity currencies higher, in otherwise quiet markets today. US and Canada will be on holiday while European calendar is near empty. Trading should remain relatively subdued. RBNZ rate hike is a major focus this week while PMIs will also catch much attention. Yet, the key is whether risk markets could break out of consolidations and resume near term rally. Such development could dictate the movements in the currency markets, in particular Dollar.

Technically, GBP/CAD is worth a note. So far, price actions from 1.6075 are more likely a consolidation pattern. That is, falls from 1.6690 and that from 1.6846, are not completed that. Break of 1.6075 will target 100% projection of 1.6846 to 1.6099 from 1.6690 at 1.5943. However, firm break of 1.6296 resistance will argue that whole three wave decline from 1.6846 has finished and bring stronger rise back to 1.6690. The next move could depend much on whether Canadian CPI (Tue) would agree to BoC’s pause.

In Asia, Nikkei rose 0.07%. Hong Kong HSI is up 1.15%. China Shanghai SSE is up 1.92%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is up 0.0030 at 0.506.

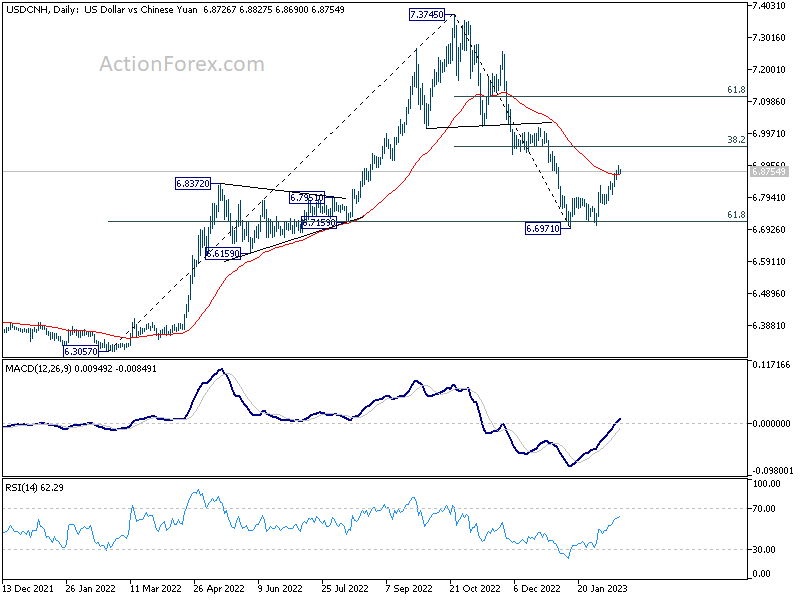

USD/CNH extending rebound towards 6.9559 fibonacci level

Chinese Yuan weakened notably last week as the dispute with US over “spy balloons” continued. The meeting between US Secretary of State Antony Blinken and China’s top diplomat Wang Yi in Munich yielded no results.

In a separate statement, China warned “If the U.S. insists on taking advantage of the (spy balloon) issue, escalating the hype, and expanding the situation, China will follow through to the end, and the U.S. will bear all the consequences.”

In an interview with NBC, Blinken said “there was no apology” from China. “I told him quite simply that that was unacceptable and can never happen again,” he said.

USD/CNH’s down leg from 7.3745 should have completed at 6.6971. Further rebound should be seen to 38.2% retracement of 7.3745 to 6.6971 at 6.9559. Reaction from there would reveal whether USD/CNH is heading for another down leg through 6.6971, or stronger rise to 61.8% retracement at 7.1157.

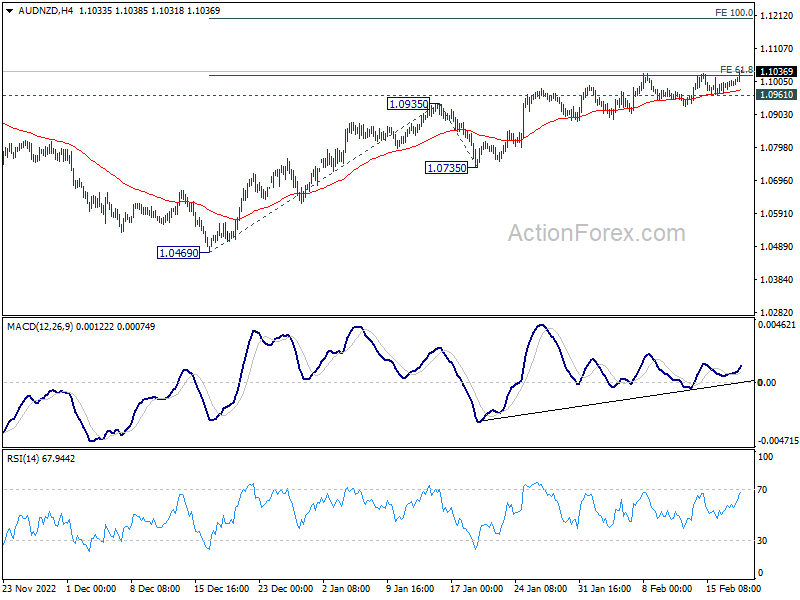

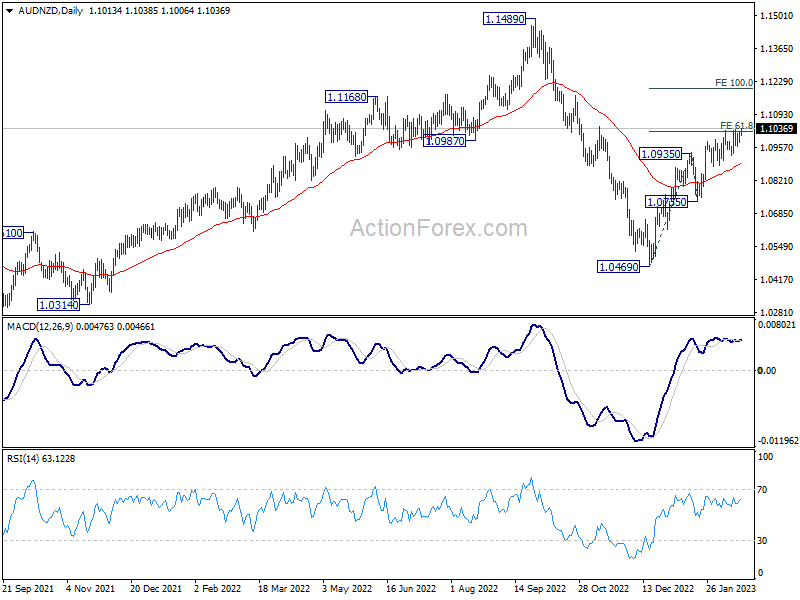

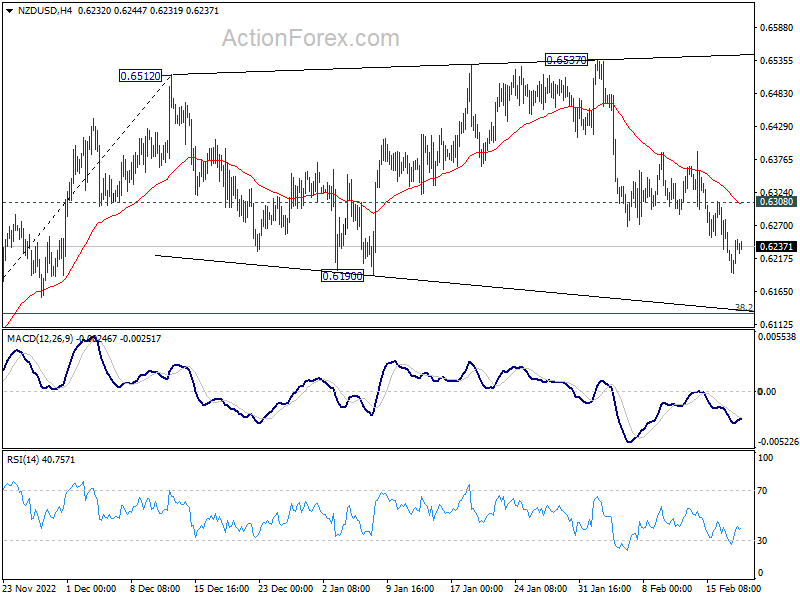

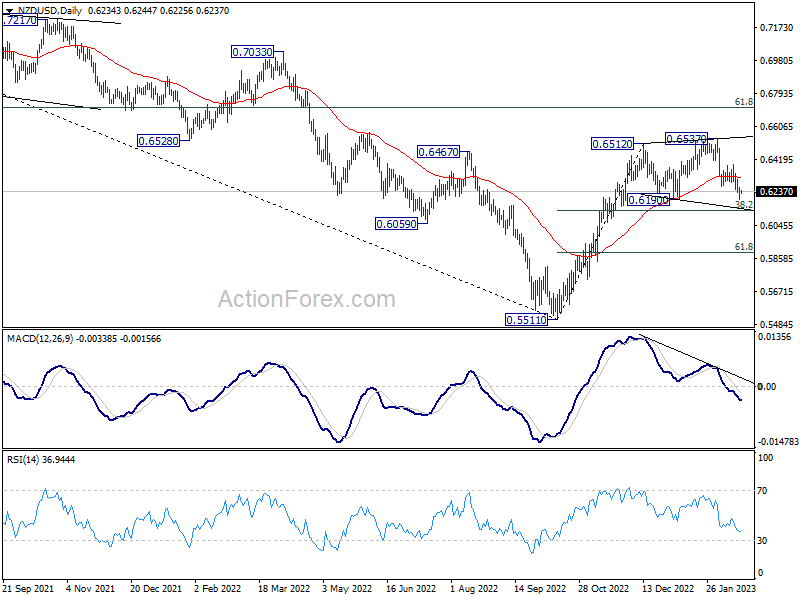

A look at AUD/NZD, NZD/USD ahead of this week’s RBNZ

New Zealand Dollar is trading with a soft tone in Asian session today. While a rate hike is expected from RBNZ this week, there are chatters of the possibility of smaller hike, or even a pause, in response to the damage done by cyclone Gabrielle. There are also some speculations of a slight dovish twist which might signal a lower terminal rate. But traders will still need to wait for RBNZ Governor Adrian Orr’s statement before making adjustment on their bets.

For now, AUD/NZD is extending the rally from 1.0469 despite loss of upside momentum. Further rise is expected as long as 1.0961 support holds. Sustained trading above 61.8% projection of 1.0469 to 1.0935 from 1.0735 at 1.1023 could prompt upside re-acceleration to 100% projection at 1.1201.

As for NZD/USD, it’s still extending the fall from 0.6537, which is seen as the third leg of the consolidation pattern from 0.6512. Deeper decline is expected as long as 0.6308 minor resistance holds, for 38.2% retracement of 0.5511 to 0.6512 at 0.6130. But strong support should be seen there to bring rebound. However, sustained break of 0.6130 will raise the change of near term reversal and target 61.8% retracement at 0.5893.

RBNZ to hike 50bps; PMIs in focus

RBNZ is expected to slow the pace of tightening this week, and raise the OCR by 50bps to 4.75%. With inflation remaining strong, RBNZ should maintain the stance that more rate hikes are underway. There are some expectations that OCR would rise further to 5.25% this year before peaking. In other central bank activities, RBA and Fed will publish monetary policy meeting minutes.

On the data front, flash PMIs would be the major focuses of the week, along with Germany ZEW and Ifo, Canada CPI and retail sales, as well as US PCE inflation. Here are some highlights for the week:

- Monday: UK Rightmove house price, Eurozone consumer confidence.

- Tuesday: New Zealand PPI; Australia PMIs, RBA minutes; Japan PMI manufacturing; Swiss Trade balance; Eurozone PMIs; Germany ZEW; UK PMIs; Canada CPI, retail sales; US PMIs, existing homes sales.

- Wednesday: New Zealand trade balance; Japan corporate services prices; Australia wage price index, construction work done; RBNZ rate decision; Germany CPI final, Ifo business climate; Swiss Credit Suisse economic expectations; Canada house price index; FOMC minutes.

- Thursday: Australia private capital expenditure; Eurozone CPI final; US GDP revision, jobless claims.

- Friday: Japan CPI; Germany GDP final, Gfk consumer climate; UK Gfk consumer confidence; US personal income and spending with PCE inflation, new home sales.

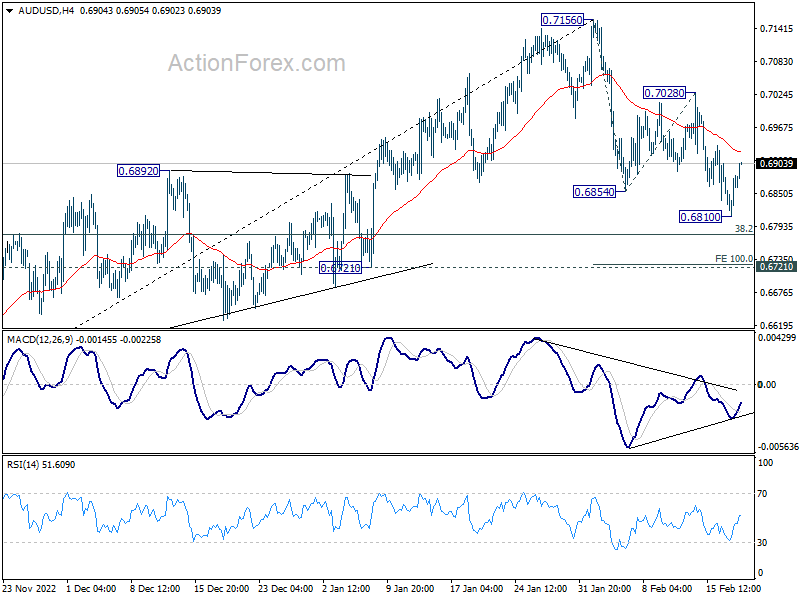

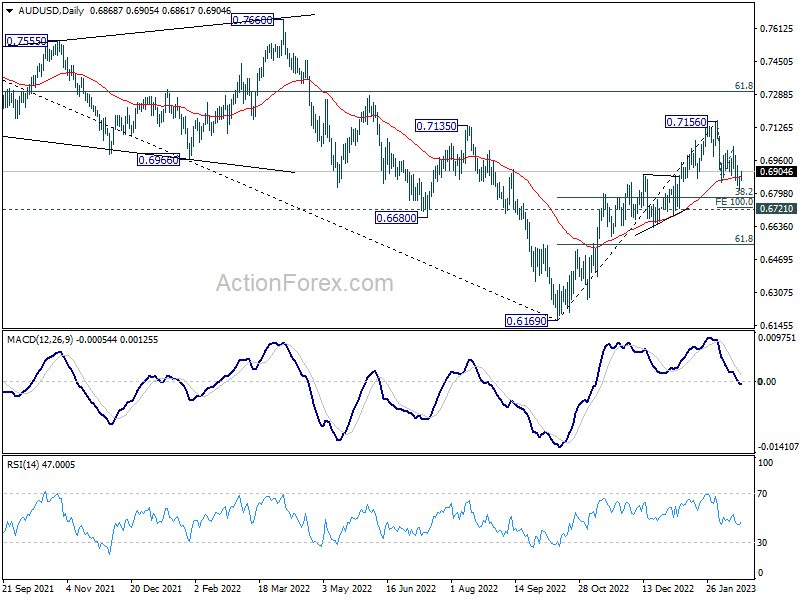

AUD/USD Daily Report

Daily Pivots: (S1) 0.6833; (P) 0.6858; (R1) 0.6905; More…

Intraday bias in AUD is turned neutral as recovery from 1.6810 extends. Risk will stay mildly on the downside as long as 0.7028 resistance holds. Below 0.6180 will resume the corrective fall from 0.7156, and target 100% projection of 0.6854 to 0.7028 from 0.6854 at 0.6736, which is close to 0.6721 key structural support. Strong support is expected there to bring rebound.

In the bigger picture, corrective decline from 0.8006 (2021 high) should have completed with three waves down to 0.6169 (2022 low). Further rally should be seen to 61.8% retracement of 0.8006 to 0.6169 at 0.7304. Sustained break there will pave the way to retest 0.8006. This will now remain the favored case as long as 0.6721 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | Rightmove House Price Index M/M Feb | 0.00% | 0.90% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Feb P | -19 | -21 |

{kind=link}