Markets are generally quite in Asian session today, in consolidation mode. Australian and New Zealand Dollar remain the worst performed. While Dollar is recovering slightly, it’s trading below last week’s high, except versus Aussie and Kiwi. Sterling is supported by hope of a Northern Ireland deal with EU but lacks follow through buying. Yen is also mixed together with Swiss Franc and Euro.

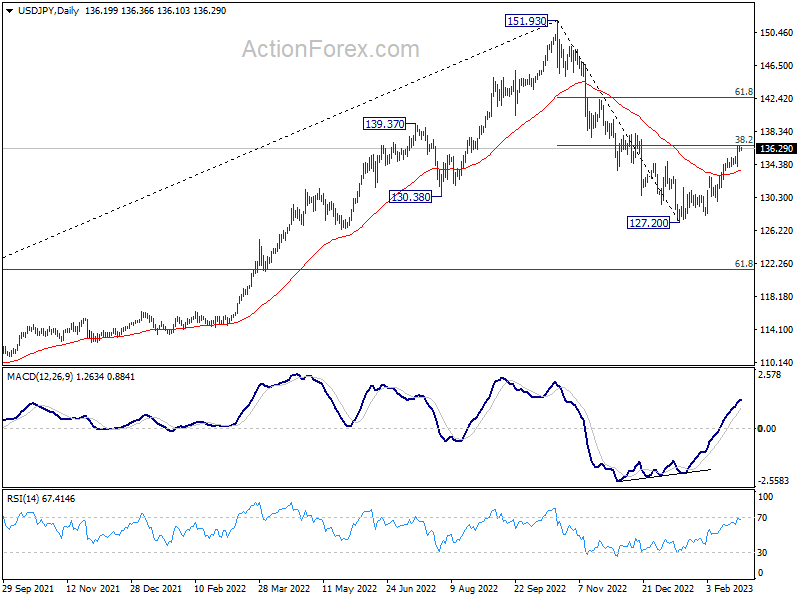

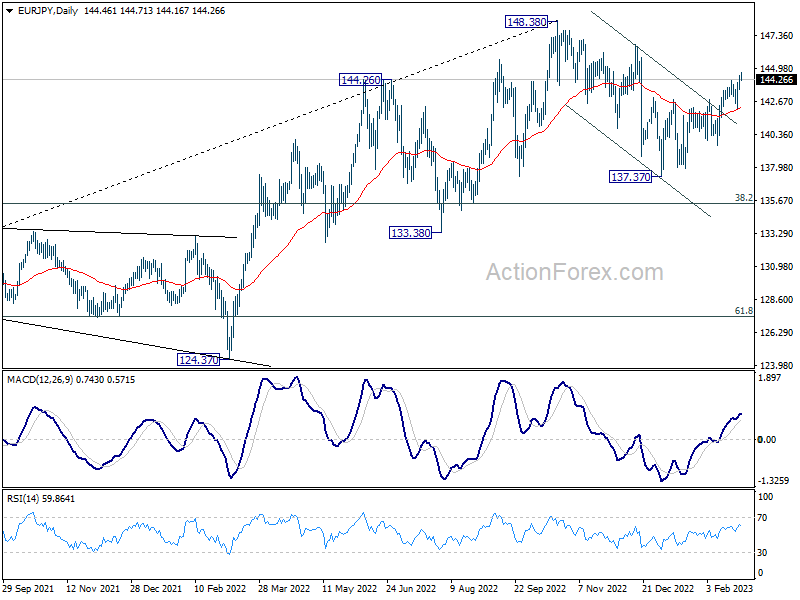

Technically, both EUR/JPY and GBP/JPY resuming near term rallies by taking out 144.15 and 163.73 temporary tops. Further rise is expected to 146.71 resistance and 169.26 resistance respectively. A key to decide Yen’s near term fortune lies on whether USD/JPY could break through 38.2% retracement of 151.93 to 127.20 at 136.64 to secure bullish reversal. Let’s see.

In Asia, Nikkei closed up 0.08%. Hong Kong HSI is down -0.30%. China Shanghai SSE is down -0.06%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is down -0.0029 at 0.502. Overnight, DOW rose 0.22%. S&P 500 rose 0.31%. NASDAQ rose 0.63%. 10-year yield dropped -0.027 to 3.922.

ECB Vujcic: We should persevere if core inflation persists

ECB Governing Council member Boris Vujcic told Bloomberg TV yesterday, “as long as core (inflation) persists at the levels we’re talking about and this is significantly higher than our rates are and significantly higher than where are target is, we should persevere.”

The markets have been raising their bets on higher interest rates and are betting tightening extending into 2024. Vujcic said, “I think this repricing in a way is what we did during our last projections, where we projected basically higher inflation for longer, core inflation which turns out to be stickier than most people probably expected.”

“Probably markets are now repricing and saying ‘OK, we might see higher rates for maybe longer,'” he said.

BoJ Wakatabe: Dangers of secular stagnation and Japanification not yet passed

Deputy Governor Masazumi Wakatabe said, “the mild-inflation regime has not come to an end, and we should say that the potential dangers of secular stagnation and Japanification have not yet passed.”

“When an exogenous shock occurs, there is an adjustment from the old to a new price system. After adjustment, the rising inflation rate is likely to return to the steady-state inflation rate,” he said.

“So the important point is how this rate is affected. Of course, it is possible that cost-push factors will remain, but whether they will push up the steady-state inflation rate is uncertain,” Wakatabe said, adding that it was “well known that cost-push inflation does not last long.”.

BoJ Uchida: Shouldn’t modify easy policy just because there are side-effects

Incoming BoJ Deputy Governor Shinichi Uchida told an upper house confirmation hearing, “BOJ must maintain monetary easing. It shouldn’t modify easy policy just because there are side-effects. Rather, it must come up with ideas” to mitigate the costs and help sustain stimulus.

He also noted it’s premature to discuss an exit from the ultra-loose monetary policy. Any exit would involve adjustments in the interest targets and the balance sheet. “In what order and at what timing the BOJ will make these adjustments will depend on economic and financial developments at the time,” Uchida said.

Japan industrial production down -4.6% mom in Jan, expected to rebound in Feb

Japan industrial production declined -4.6% mom in January, much worse than expectation of -2.6% mom.

Upon the release of the data, the METI downgraded its assessment of industrial production, saying that it has weakened. Never the less, the ministry forecast industrial production to bounce back by 8.0% in February, and then a further 0.7% in March.

Retail sales rose 6.3% yoy, above expectation of 4.0% yoy.

Australia retail sales rose 1.9% mom in Jan, flat on average over the past few months

Australia retail sales turnover rose 1.9% mom to AUD 35.09B in January, above expectation of 1.6% mom. Compared with January 2022, sales turnover was up 7.5% yoy.

Ben Dorber, ABS head of retail statistics, said: “The rebound in retail turnover in January followed a substantial fall of 4.0 per cent in December and a large rise of 1.7 per cent in November.

“Looking through this volatility shows that turnover is at a similar level to September 2022, and on average, growth has been flat over the past few months.”

NZ ANZ business confidence rose to -43.3, firms wary but getting on with the job

New Zealand ANZ Business Confidence improved form -52.0 to -43.3 in February. Own Activity Outlook rose from -15.8 to -9.2.

Looking at some details, export intentions ticked up from -5.4 to -5.2. Investment intentions rose from -13.7 to -4.9. Employment intentions jumped from -11.1 to -3.4. Pricing intentions dropped from 62.4 to 58.8. Cost expectations dropped from 91.3 to 88.3. Inflation expectations ticked down from 5.99 to 5.94.

ANZ said: “The shock value of the November Monetary Policy Statement appears to have faded into the rear-vision mirror as firms focus on the risks and opportunities that are front and centre…. Opportunity is clearly still knocking. That said, the level of most indicators remain subdued – firms are still very wary, and understandably so. But they are getting on with the job.”

Looking ahead

Germany import price, France GDP, Swiss KOF and GDP will be featured in European session. Later in the day, Canada will release GDP. US will release goods trade balance, house price index, Chicago PMI and consumer confidence.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 143.88; (P) 144.22; (R1) 144.86; More….

EUR/JPY’s rebound from 137.37 resumed by breaking through 144.15 resistance. Intraday bias is back on the upside. As noted before, corrective fall from 148.38 has completed at 137.37 already. Further rise should be seen to 146.71 resistance and then 148.38 high. For now, outlook will stay cautiously bullish as long as 142.13 support holds, in case of retreat.

In the bigger picture, as long as 55 week EMA (now at 139.21) holds, larger up trend from 114.42 (2020 low) is still in progress for 149.76 long term resistance. However, firm break of 55 week EMA will bring deeper fall to 38.2% retracement of 114.42 to 148.38 at 135.40. Sustained break there will raise the chance of trend reversal, and target 61.8% retracement at 127.39.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Industrial Production M/M Jan P | -4.60% | -2.60% | 0.30% | |

| 23:50 | JPY | Retail Trade Y/Y Jan | 6.30% | 4.00% | 3.80% | |

| 00:00 | NZD | ANZ Business Confidence Feb | -43.3 | -52 | ||

| 00:30 | AUD | Current Account Balance (AUD) Q4 | 14.1B | 6.8B | -2.3B | 0.8B |

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.40% | 0.40% | 0.30% | |

| 00:30 | AUD | Retail Sales M/M Jan | 1.90% | 1.60% | -3.90% | -4.00% |

| 05:00 | JPY | Housing Starts Y/Y Jan | 6.60% | -1.20% | -1.70% | |

| 07:00 | EUR | Germany Import Price Index M/M Jan | 0.40% | -1.60% | ||

| 07:45 | EUR | France GDP Q/Q Q4 | 0.10% | 0.10% | ||

| 08:00 | CHF | KOF Economic Barometer Feb | 98 | 97.2 | ||

| 08:00 | CHF | GDP Q/Q Q4 | 0.30% | 0.20% | ||

| 13:30 | CAD | GDP M/M Dec | 0.20% | 0.10% | ||

| 13:30 | USD | Goods Trade Balance (USD) Jan P | -91.0B | -90.3B | ||

| 13:30 | USD | Wholesale Inventories Jan P | 0.10% | 0.10% | ||

| 14:00 | USD | Housing Price Index M/M Dec | -0.20% | -0.10% | ||

| 14:00 | USD | S&P/CS Composite-20 HPI Y/Y Dec | 6.80% | 6.80% | ||

| 14:45 | USD | Chicago PMI Feb | 45 | 44.3 | ||

| 15:00 | USD | Consumer Confidence Feb | 108.5 | 107.1 |

{kind=link}