Dollar faced broad sell-off overnight after the less hawkish than expected Fed rate hike and press conference, with Euro emerging as the biggest winner against the greenback. Sterling and Swiss Franc followed suit, while Australian and New Zealand dollars also strengthened but lagged on a weekly basis.

Attention now shifts to BoE and SNB rate decisions. Both are expected to continue their rate hike cycles, but uncertainties remain about the path ahead. Any outcome perceived as less hawkish could push Euro further up, aided by an extended rally in EUR/CHF and a stronger rebound in EUR/GBP.

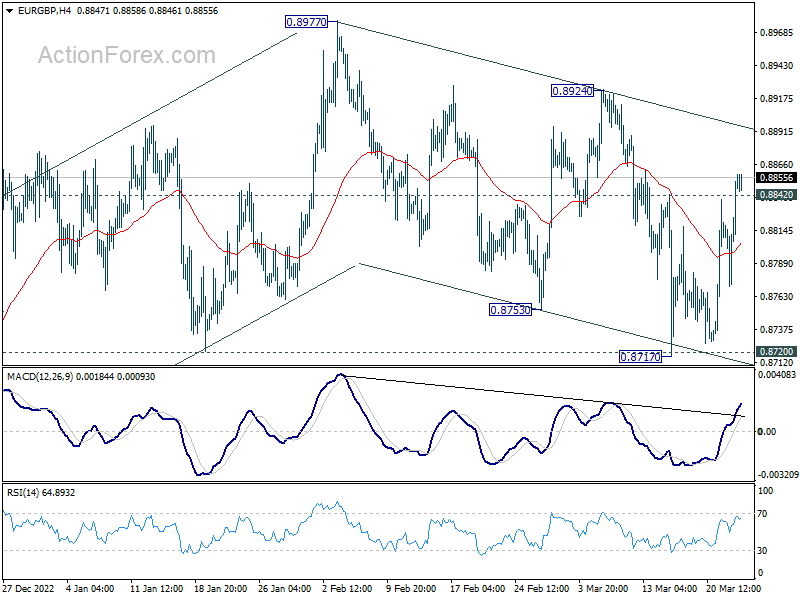

Technically, EUR/GBP’s break of 0.8842 minor resistance affirm the case that corrective fall from 0.8977 has completed with three waves down to 0.8717, after drawing support from 0.8720. Further break of 0.8924 resistance will send the cross through 0.8977 to resume whole rise from 0.8545 (2022 low).

In Asia, Nikkei closed down -0.17%. Hong Kong HSI is up 1.74%. China Shanghai SSE is up 0.48%. Singapore Strait Times is down -0.14%. Japan 10-year JGB yield is down -0.0295 at 0.305. Overnight, DOW dropped -1.63%. S&P 500 dropped -1.65%. NASDAQ dropped -1.60%. 10-year yield dropped -0.106 to 3.500

S&P 500 down, reacted more to Yellen than Powell?

US markets experienced a complex development overnight due to simultaneous reactions to two events. Initially, the markets responded bullishly to the Fed’s less hawkish than expected rate hike and press conference. However, just an hour before the close, sellers jumped in, and the three major indexes closed -1.6% lower.

The selloff might be more attributed to Treasury Secretary Janet Yellen’s comments at a Senate committee. She explicitly stated, “I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits.”

Yellen further elaborated, “when a bank failure is deemed to create systemic risk, which I think of as the risk of a contagious bank run…we are likely to invoke the systemic risk exception, which permits the FDIC to protect all depositors, and that would be a case-by-case determination.”

Meanwhile, Asian markets have remained sluggish and mixed today, without any apparent signs of bearishness carried over. It may take some more time to understand the unfolding situation fully.

Technically, near term outlook in S&P 500 isn’t too bearish yet given it’s holding inside a near term channel. However, break of 3901.27 support will argue that the corrective rebound from 3808.85 has completed at 4039.49, after hitting falling trend line resistance. Deeper selloff would then follow through 3808.86 to resume whole decline from 4195.44.

Fed softened hawkish tone, but not dovish

In light of the Fed announcement and press conference overnight, it appears that another 25bps rate hike is likely in May, followed by a prolonged pause with no rate cut expected until next year. The overall picture remains hawkish, albeit not as much as after Fed Chair Jerome Powell’s earlier testimony this month.

As anticipated, Fed raised interest rates by 25bps to 4.75-5.00%. While the tightening bias was maintained, the statement softened its tone, stating, “some additional policy firming may be appropriate.” Despite recent market turmoil, median projections still indicated an interest rate peak of 5.1% this year, suggesting one more 25bps hike before pausing until next year. The median projection for 2024 interest rate increased from 4.1% to 4.3%, signaling a slower path of rate cuts.

During the post-meeting press conference, Powell acknowledged that “financial conditions seem to have tightened” recently, adding that if the situation persists, it could “easily have a significant macroeconomic effect, and we would factor that into our policy decisions.” While he admitted that a pause was considered during the meeting, he emphasized that a rate cut this year was “not our baseline expectation,” stating, “the key is we have to have policies tight enough to bring inflation down to 2%.”

Suggested readings on Fed:

- FOMC’s Fight Against Inflation Finely Balanced

- FOMC Hikes Rates, But End of Tightening Cycle Coming Into View

- Suderman Says: Rates Up as Expected, But Peak in Sight?

- FOMC Hikes Policy Rate by 25 Basis Points, Cautions on Bank Stress

- Fed hikes 25 bps, terminal rate forecast unchanged at 5.1%

- (FED) Federal Reserve Issues FOMC Statement

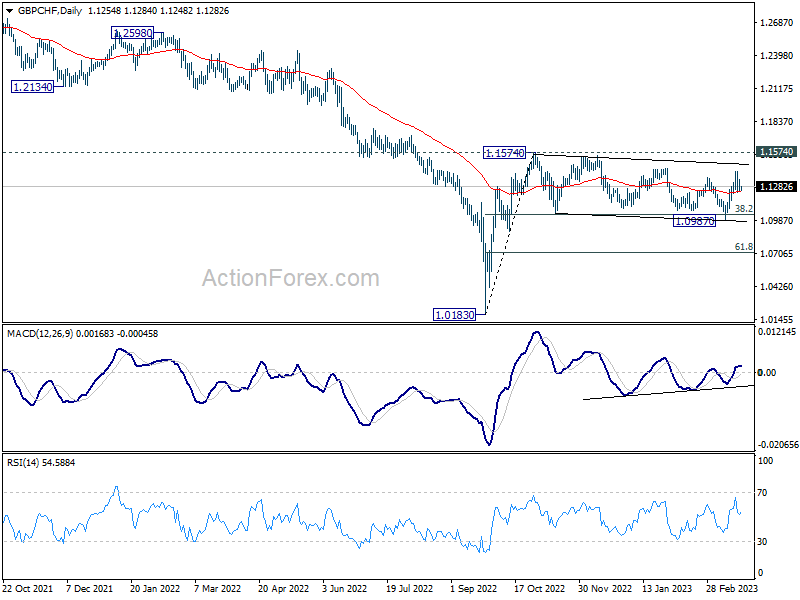

GBP/CHF extending range trading ahead of BoE and SNB

BoE and SNB are both expected to raise interest rates today. A 25bps hike by BoE to 4.25% is widely anticipated, though the case for a subsequent pause has been shaken by the reacceleration of consumer inflation in February. The Monetary Policy Committee is known for its divided outlook on the amount of tightening needed, and today’s voting should continue to reflect this pattern.

An explicit indication of a pause could put downward pressure on Sterling, but such a signal is unlikely to emerge. Instead, BoE is more likely to adopt a non-committal stance, waiting for incoming data and the next economic projections in May before making a firm judgment.

Concurrently, SNB is expected to hike by 50bps to 1.50%. Market expectations suggest a possible 25bps hike in June to a terminal rate of 1.75%, followed by a pause. However, the SNB’s comments and projections could reshape these expectations.

Here are some previews for BoE and SNB:

- UK Inflation Will Strengthen the Hawks

- BoE Rate Decision: One Last Hike Before Hitting Pause?

- BoE Preview: 25 bps Hike and Done?

- Bank of England Preview – Final Hike in Store

- Bank of England & Swiss National Bank Both Set to Hike

- Will the SNB Roil Markets With a Hike Amid Credit Suisse Crisis?

GBP/CHF is still bounded in medium term sideway consolidation from 1.1574. Outlook is kept bullish as the crosses quickly recovered after breaching 38.2% retracement of 1.0183 to 1.1574 at 1.1043 briefly. A break through 1.1574 resistance to resume the rise form 1.0184 is expected. But that might not happen today, unless there is some drastic surprise from BoE or SNB.

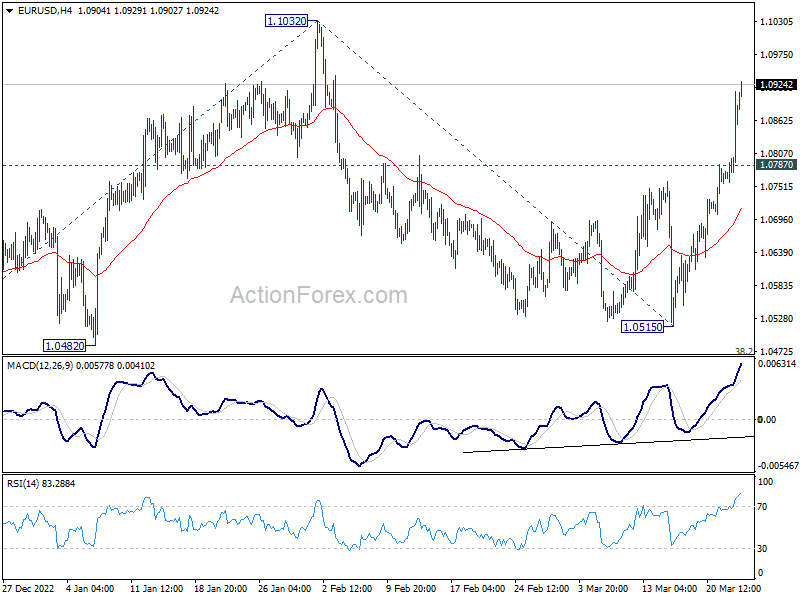

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0772; (P) 1.0842; (R1) 1.0926; More…

EUR/USD’s rise from 1.0515 accelerates higher and intraday bias stays on the upside for retesting 1.1032 high. Decisive break there will resume whole up trend from 0.9534 and target 1.1273 fibonacci level next. On the downside, below 1.0787 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

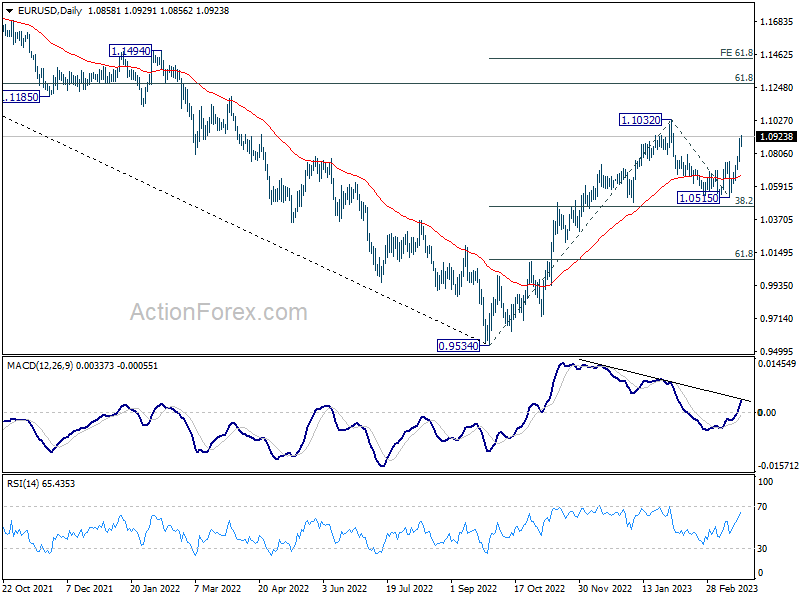

In the bigger picture, rise from 0.9534 (2022 low) is in progress with 38.2% retracement of 0.9534 to 1.1032 at 1.0460 intact. The strong support from 55 week EMA (now at 1.0623) was also a medium term bullish sign. Next target is 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273. Sustained break there will solidity the case of bullish trend reversal and target 1.2348 resistance next (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:30 | CHF | SNB Interest Rate Decision | 1.50% | 1.00% | ||

| 12:00 | GBP | BoE Rate Decision | 4.25% | 4.00% | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 7–0–2 | 7–0–2 | ||

| 12:30 | USD | Current Account (USD) Q4 | -217B | |||

| 12:30 | USD | Initial Jobless Claims (Mar 17) | 195K | 192K | ||

| 14:00 | USD | New Home Sales Feb | 650K | 670K | ||

| 14:30 | USD | Natural Gas Storage | -58B |

{kind=link}