Dollar turned mixed in Asian session as traders are awaiting fresh inspirations from economic data and comments from Fed officials. The FOMC is clearly split in way with some policymakers advocating a “hold” in June. Nevertheless, they’re unified in another way that even a “hold” doesn’t necessarily means a “pause”, not to mention a “peak”. The greenback, in any case, will look into today’s ADP employment and ISM manufacturing, as well as tomorrow’s non-farm payroll data for more guidance.

Australian Dollar is recovering mildly, with help from China’s manufacturing data, but upside is limited. Yen is turning softer again after this week’s rebound is losing momentum. Sterling is holding on to gains against Euro and Swiss Franc, as well as Dollar. Meanwhile, Canadian Dollar is sluggish together with New Zealand Dollar.

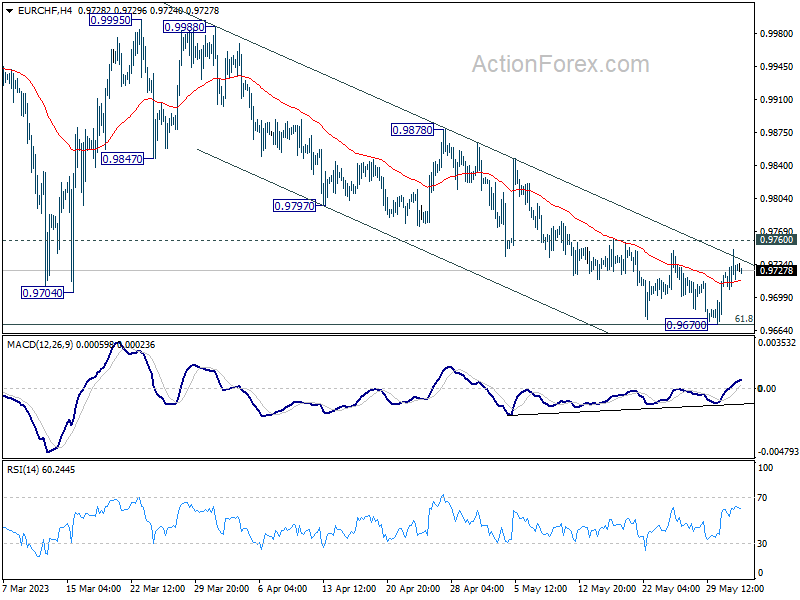

Technically, Euro is clearly weaker this week after downside surprising in France and Germany inflation data. Yet, EUR/CHF is still working hard to form a bottom and focuses will be on 0.9760 minor resistance today. Firm break there should confirm short term bottoming at 0.9670 and bring stronger rebound back to 0.9797/9878 resistance zone. The next move will depend on markets’ reaction to today’s Eurozone CPI data.

In Asia, Nikkei closed up 0.84%. Hong Kong HSI is up 0.54%. China Shanghai SSE is up 0.28%. Singapore Strait Times is up 0.12%. Japan 10-year JGB yield is down -0.0081 at 0.425. Overnight, DOW dropped -0.41%. S&P 500 dropped -0.61%. NASDAQ dropped -0.63%. 10-year yield dropped -0.063 to 3.637.

SNB Jordan: We don’t see a big risk in over-tightening monetary policy

SNB Chairman Thomas Jordan recently warned yesterday that the more inflation is entrenched in the perception of companies and households, the harder it is to bring it down. He highlighted the urgency of the situation, stating, “We have to bring it back below 2% as soon as possible.”

Discussing the bank’s approach towards interest rates, Jordan assured that Switzerland’s are “still very low”. “We don’t see a big risk in over-tightening monetary policy. It is not something that will damage financial stability in general in Switzerland,” he affirmed.

Regarding the financial stability issues surrounding Credit Suisse, Jordan clarified that it was an individual case where the problem was not interest rates, but rather a “lack of trust of market participants in an institution.”

Looking ahead, market expectations suggest a 25bps rise from the current 1.5% level when the central bank delivers its next assessment in June.

BoE Mann: Inflation gap in the UK more persistent than others

BoE policymaker, Catherine Mann, has highlighted the unique and mounting inflation problem that Britain is facing in comparison to the United States and the Eurozone.

Mann pointed to both large-scale price increases and the rising persistence of these underlying pressures as causes for concern. She emphasized, “The gap (between headline and core CPI) that I have in my country is more persistent than the gaps that we see in either of my neighbours, the U.S. or the euro area.”

The gap she refers to is the disparity between headline inflation (which includes volatile commodities like food and energy) and core inflation (which excludes these commodities).

Notably, Mann underscored the role of British businesses and increased wages in maintaining high core inflation. She explains that businesses in the UK have been successful in passing on price rises, contributing to this persistent inflation gap. This, coupled with increased wages, suggests that headline inflation has been slower to recede towards the core rate than it has in other regions.

“There is a gap between the headline, which is incorporating energy which went up really high and now has come down, and core where we do start to see the implications coming through pricing channels, through wage negotiations, into something that is persistent,” Mann explained.

Fed Jefferson: A pause in June doesn’t mean rates have peaked

Comments from top officials from Fed suggested a pause in interest rate hikes in June while possible, shouldn’t be misinterpreted as a sign that peak rates for the cycle have been reached.

Fed Governor, Philip Jefferson, clarified, “A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.”

Jefferson, suggested that skipping a rate hike at an upcoming meeting would provide an opportunity for the committee to review more data before deciding on the extent of any further policy tightening.

Philadelphia Fed President, Patrick Harker, echoed this sentiment, albeit with a more forceful argument for the need to ‘skip’ rather than ‘pause’. “I am in a camp increasingly coming into this meeting of thinking that we really should skip, not pause,” he remarked.

Harker believes the current policy is nearing, if not already at, a restrictive level and suggests a period of careful reflection before further action is taken.

Harker added, “I think we have to be ready that we might have to do more and I’m fully aware we have to do that and willing to do that, but I want to give it a little bit of time.”

IMF sees opportunity for Japan to re-anchoring Inflation Expectations

IMF chief economist, Pierre-Olivier Gourinchas, suggested that a unique opportunity may be presenting itself in Japan to re-anchor inflation expectations to BoJ’s target. However, he cautioned that the process won’t be instantaneous.

“There’s an opportunity right now,” Gourinchas said, “but it will take time. It won’t happen overnight.” Achieving this re-anchoring requires convincing the public that Japan won’t slide back into deflation – a challenge given the country’s prolonged struggle with price stagnation. Gourinchas believes it’s “too early” for the BoJ to tighten policy, stressing the need for careful handling of the situation.

Pointing to the global trend of persistent inflation despite initial expectations of transitory dynamics, Gourinchas warned, “Obviously, the history of the last two years is one where inflation that was supposed to be transitory, turned out to be not transitory. We could have similar dynamics in Japan.” Given this possibility, he underscored the need for vigilance and readiness to tighten monetary policy if inflation remains too high.

Regarding potential strategies for policy tightening, Gourinchas suggested a cautious approach. “It’s probably safer to first move away from the control of long-term yields. And then, if the need arises to tighten monetary policy, it can do so as part of the usual tightening of the policy rate,” he proposed. However, he acknowledged that executing this transition would be technically complex.

Japan PMI manufacturing finalized at 50.6, a decisive turnaround

Japan PMI Manufacturing was finalized at 50.6 in May, up from April’s 49.5. That’s the first expansionary reading since October 2022, signalling a modest overall improvement in operating conditions. Also, business optimism reached highest level since January 2022, while supplier performance stabilized.

Tim Moore, Economics Director at S&P Global Market Intelligence, said: “The latest au Jibun Bank PMI survey highlights a decisive turnaround in manufacturing sector performance during May and brings to an end a six-month period of weakening business conditions.”

China Caixin PMI manufacturing rose to 50.9, activity improved

China Caixin PMI Manufacturing rose from 49.5 to 50.9 in May, signaling the first improvement in the health of the sector since February. Caixin noted stronger increase in output as firms saw fresh upturn in new business. Input costs fell solidly. Employment, however, continued to decline as business confidence softened.

Wang Zhe, Senior Economist at Caixin Insight Group said: “In a nutshell, manufacturing activity improved in May. Both supply and demand expanded, but employment sank to a three-year low. Businesses stepped up purchasing, inventories of raw materials grew marginally, logistics picked up, prices continued to slump, and manufacturers’ optimism wavered.”

Looking ahead

Eurozone CPI flash and ECB meeting accounts are the main feature in European session. Eurozone will also release unemployment rate and PMI manufacturing final. UK will release PMI manufacturing final, M4 money supply and mortgage approvals.

Later in the day, US ISM manufacturing and ADP employment will take center stage. Weekly jobless claims will also be released.

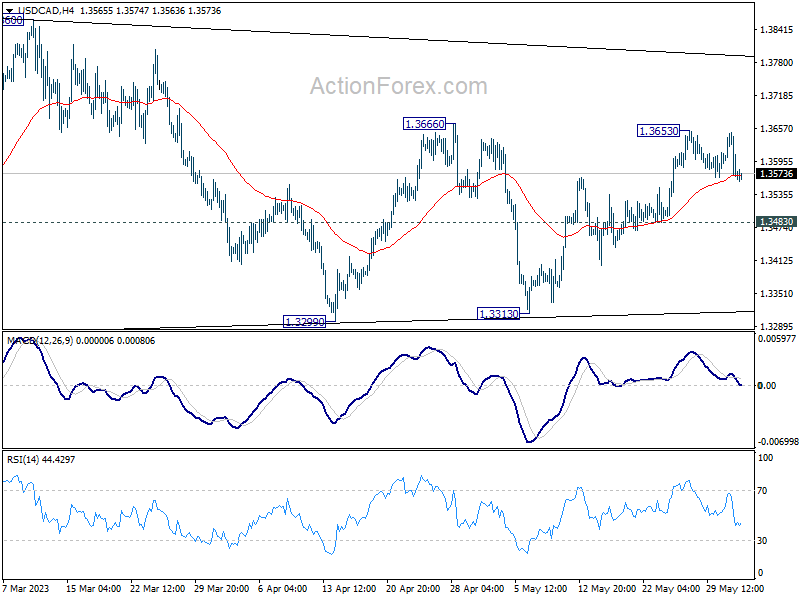

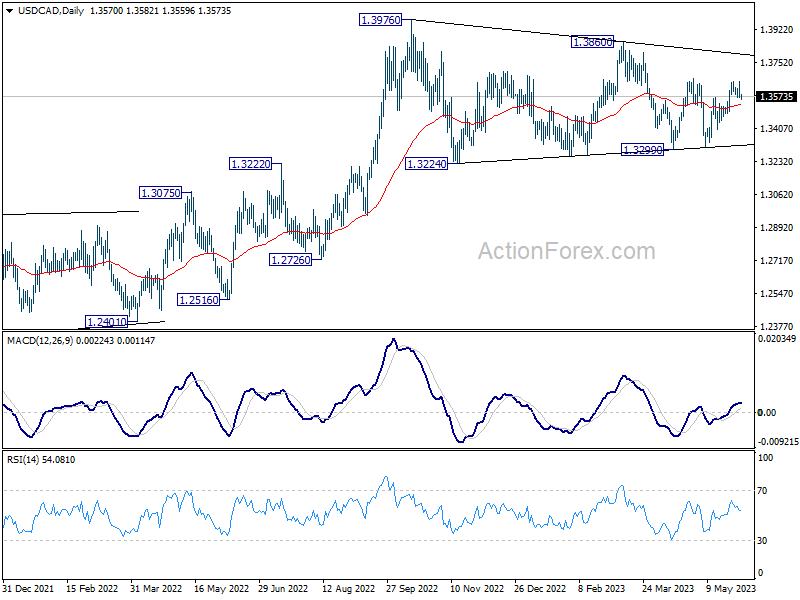

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3545; (P) 1.3599; (R1) 1.3629; More….

USD/CAD is staying in range below 1.3653 and intraday bias remains neutral. Price actions from 1.3976 are seen as a triangle consolidation pattern. Above 1.3666 will target 1.3860 resistance first. Firm break of 1.3860 will argue that larger up trend is ready to resume through 1.3976 high.

In the bigger picture, rise from 1.2005 (2021 low) is expected to resume through 1.3976 after consolidation from there completes. On decisive break of 1.3976, next target will be 1.4667/89 long term resistance zone. This will remain the favored case as long as 38.2% retracement of 1.2005 to 1.3976 at 1.3233 holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Capital Spending Q1 | 11.00% | 5.50% | 7.70% | |

| 00:30 | JPY | Manufacturing PMI May F | 50.6 | 50.8 | 50.8 | |

| 01:30 | AUD | Private Capital Expenditure Q1 | 2.40% | 1.10% | 2.20% | 3.00% |

| 01:45 | CNY | Caixin Manufacturing PMI May | 50.9 | 49.5 | ||

| 06:00 | CHF | Trade Balance (CHF) Apr | 2.6B | 3.73B | 4.53B | |

| 06:00 | EUR | Germany Retail Sales M/M Apr | 0.80% | 0.90% | -2.40% | -2.20% |

| 07:30 | CHF | Manufacturing PMI May | 44.5 | 45.3 | ||

| 07:45 | EUR | Italy Manufacturing PMI May | 45.8 | 46.8 | ||

| 07:50 | EUR | France Manufacturing PMI May F | 46.1 | 46.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI May F | 42.9 | 42.9 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI May F | 44.6 | 44.6 | ||

| 08:30 | GBP | Manufacturing PMI May F | 46.9 | 46.9 | ||

| 08:30 | GBP | Mortgage Approvals Apr | 54K | 52K | ||

| 08:30 | GBP | M4 Money Supply M/M Apr | -0.20% | -0.60% | ||

| 09:00 | EUR | Eurozone Unemployment Rate Apr | 6.50% | 6.50% | ||

| 09:00 | EUR | Eurozone CPI Y/Y May P | 6.30% | 7.00% | ||

| 09:00 | EUR | Eurozone CPI Core May P | 5.50% | 5.60% | ||

| 11:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 11:30 | USD | Challenger Job Cuts May | 175.90% | |||

| 12:15 | USD | ADP Employment Change May | 167K | 296K | ||

| 12:30 | USD | Initial Jobless Claims (May 26) | 236K | 229K | ||

| 12:30 | USD | Nonfarm Productivity Q1 | -2.70% | -2.70% | ||

| 12:30 | USD | Unit Labor Costs Q1 | 6.30% | 6.30% | ||

| 13:30 | CAD | Manufacturing PMI May | 50.2 | |||

| 13:45 | USD | Manufacturing PMI May F | 48.5 | 48.5 | ||

| 14:00 | USD | ISM Manufacturing PMI May | 47 | 47.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid May | 52.5 | 53.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index May | 50.2 | |||

| 14:00 | USD | Construction Spending M/M Apr | 0.10% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 106B | 96B | ||

| 15:00 | USD | Crude Oil Inventories | -1.4M | -12.5M |

{kind=link}