Australian Dollar is trading broadly lower after RBA opted to keep interest rates on hold. However, the currency’s losses remain contained was not too much out of expectations. RBA’s continued bias towards tightening, albeit arguably less emphatic than before, is currently helping to limit Aussie’s downside, keeping it within Monday’s trading range, waiting for a potential breakout. The New Zealand Dollar is also trending weaker, closely following its Australian counterpart.

Meanwhile, Japanese Yen is extending its recent downward trajectory, despite 10-year JGB yield hovering around 0.6% mark. Positive investor sentiment in Japan, buoyed by Nikkei’s post-BoJ rally, continues to weigh on the Yen. The focus now shifts to which Yen cross might break out of its recent range first.

On the other side of the coin, Dollar is today’s strongest performer, trailed by British Pound and Swiss Franc. The greenback’s path could be influenced by today’s ISM manufacturing index, although the primary market-moving event is likely to be Friday’s non-farm payrolls report.

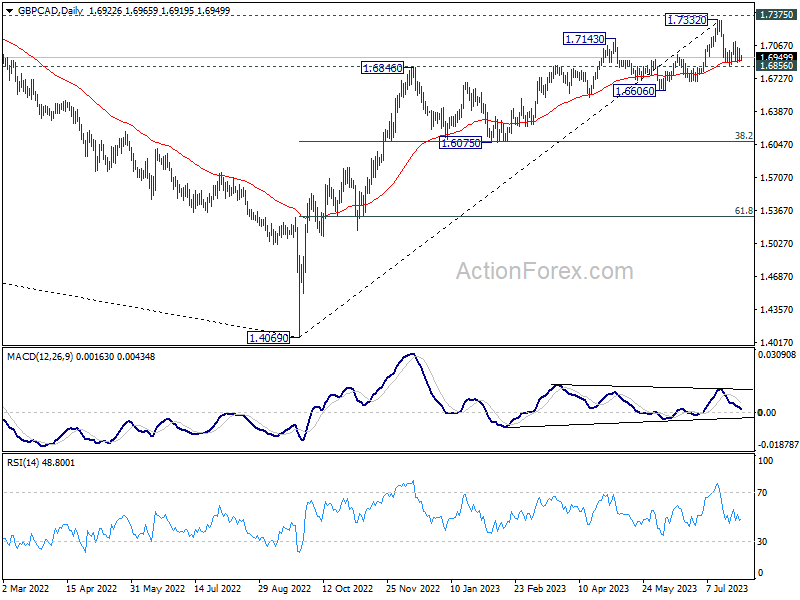

Technically, GBP/CAD now gyrating in tight range just above 55 D EMA (now at 1.6911). Medium term momentum as been diminishing somewhat as seen in D MACD. Risk of a major pull back is increasing considering that it’s also in proximity to 1.7375 long term structural resistance. Firm break of 1.6856 could set up a medium term corrective fall through 1.6606 support, with prospect of falling to as low as 1.6075 cluster support (38.2% retracement of 1.4069 to 1.7332 at 1.6086. This week’s BoE rate decision and Canada employment data could be the trigger of the start of this down move.

In Asia, at the time of writing, Nikkei is up 0.79%. Hong Kong HSI is down -0.35%. China Shanghai SSE is down -0.11%. Singapore Strait Times is up 0.00%. Japan 10-year JGB yield is down -0.0010 at 0.602. Overnight, DOW rose 0.28%. S&P 500 rose 0.15%. NASDAQ rose 0.21%. 10-year yield dropped -0.010 to 3.959.

RBA on hold, keeps tightening bias

RBA kept its cash rate target at 4.10%, retaining a hawkish bias. The bank noted, “Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe.” However, RBA underscored that any future decision will be data-dependent and based on an “evolving assessment of risks.”

Explaining the decision to hold rates, RBA stated that “higher interest rates are working to establish a more sustainable balance between supply and demand in the economy and will continue to do so.” Amidst “uncertainty” surrounding the economic outlook, maintaining the current rate provides “further time” to assess the impact of previous hikes.

While the central bank anticipates recent data to be “consistent” with an inflation return to its 2-3% target over the forecast horizon, it warned of “significant uncertainties”.

RBA expressed concerns about the surprising persistence of services price inflation overseas, which could potentially reflect in Australia. Additionally, it mentioned uncertainties about “how firms’ pricing decisions and wages will respond to the slowing in the economy at a time when the labour market remains tight.” Also, it stated that “the outlook for household consumption is also an ongoing source of uncertainty.”

Japan PMI manufacturing finalized at 49.6, but business optimism elevated

Japan PMI Manufacturing was finalized at 49.6 in July, down from June’s 49.8. That also marked the second month of concurrent decline in output and new orders. Usamah Bhatti at S&P Global Market Intelligence highlighted the significant role of “quicker deterioration in new order inflows” and also “sustained” decline in production.

Despite these struggles, inflationary pressures showed signs of abating as the rate of input cost inflation was the slowest since February 2021. However, selling price inflation was “unchanged” and “sharp overall” as Japanese manufacturers passed on a portion of higher cost burdens to clients.

The industry displayed robust optimism about the future, with the second-highest positive sentiment recorded in the last 18 months, driven by expectations of a boost in domestic and international demand owing to new product launches and the ongoing mitigation of COVID-19 and inflation-related influences.

China Caixin PMI manufacturing down to 49.2, first contraction in three months

China’s Caixin PMI Manufacturing index slipped from 50.5 to 49.2 in July, marking the first contraction in three months and falling below the expected 50.3. According to Caixin, there was a marginal contraction in output, and total sales plummeted due to a more pronounced decline in new export orders. Additionally, both input costs and output charges saw a decrease.

Senior Economist at Caixin Insight Group, Wang Zhe, highlighted the deteriorating situation, stating, “Overall, manufacturing conditions contracted in July, with supply, demand, exports, and employment all deteriorating. Prices continued to decline, inventories rose without companies adjusting them, and logistics times increased.” He noted that manufacturers’ optimism remained, but it had weakened.

Wang further explained, “China’s economic recovery in the first quarter exceeded expectations, but the momentum weakened in the second. Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted.”

Looking ahead

Eurozone PMI manufacturing final and unemployment rate, Germany unemployment, UK PMI manufacturing final will be released in European session. Later in the day, US ISM manufacturing will be the highlight, construction spending will also be released.

AUD/USD Daily Report

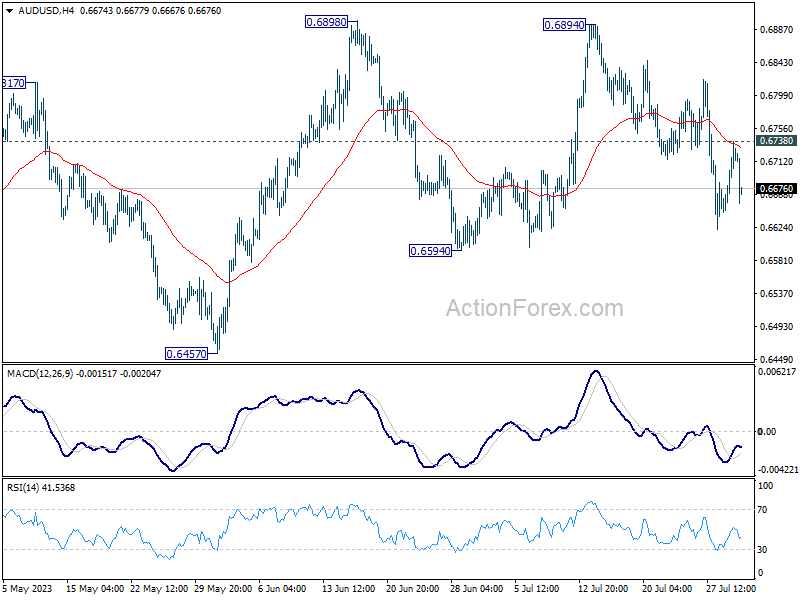

Daily Pivots: (S1) 0.6663; (P) 0.6701; (R1) 0.6755; More…

AUD/USD’s recovery was rejected by 55 4H EMA and retreated sharply since then. Intraday bias remains neutral first. While deeper fall cannot be ruled out, strong support should be seen from 0.6594 to complete to corrective pattern from 0.6898. On the upside, break of 0.6738 resistance will turn bias back to the upside for retesting 0.6894/8 resistance zone. However, sustained break of 0.6594 will dampen this view and bring deeper fall towards 0.6457.

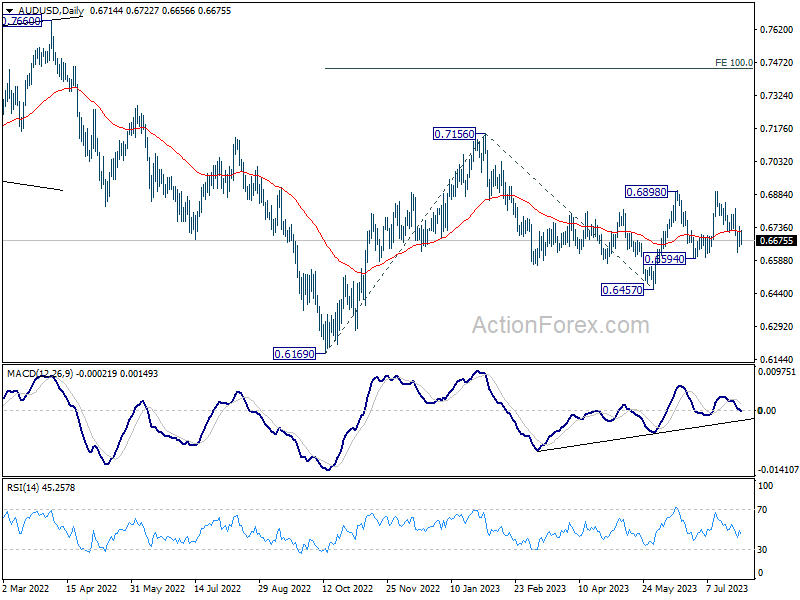

In the bigger picture, outlook is mixed for now as AUD/USD failed to sustain above both 55 D EMA (now at 0.6720) and 55 W EMA (now at 0.6784). On the upside, break of 0.65898 resistance will solidify the case that down trend from 0.8006 (2021 high) has already completed, and target 0.7156 resistance for confirmation. However, break of 0.6457 will likely resume the down trend through 0.6169 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | 3.50% | -2.20% | -2.30% | |

| 23:01 | GBP | BRC Shop Price Index Y/Y Jun | 7.60% | 8.40% | ||

| 23:30 | JPY | Unemployment Rate Jun | 2.50% | 2.60% | 2.60% | |

| 00:30 | JPY | Manufacturing PMI Jul F | 49.6 | 49.4 | 49.4 | |

| 01:30 | AUD | Building Permits M/M Jun | -7.70% | -7.90% | 20.60% | |

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 49.2 | 50.3 | 50.5 | |

| 04:30 | AUD | RBA Interest Rate Decision | 4.10% | 4.35% | 4.10% | |

| 07:45 | EUR | Italy Manufacturing PMI Jul | 43.9 | 43.8 | ||

| 07:50 | EUR | France Manufacturing PMI Jul F | 44.5 | 44.5 | ||

| 07:55 | EUR | Germany Unemployment Change Jun | 15K | 28K | ||

| 07:55 | EUR | Germany Unemployment Rate Jun | 5.70% | 5.70% | ||

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 38.8 | 38.8 | ||

| 08:00 | EUR | Italy Unemployment Rate Jun | 7.70% | 7.60% | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 42.7 | 42.7 | ||

| 08:30 | GBP | Manufacturing PMI Jul F | 45 | 45 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.50% | 6.50% | ||

| 13:30 | CAD | Manufacturing PMI Jul | 48.9 | 48.8 | ||

| 13:45 | USD | Manufacturing PMI Jul F | 49 | 49 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | 46.5 | 46 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 42.3 | 48.1 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 41.8 | |||

| 14:00 | USD | Construction Spending M/M Jun | 0.60% | 0.90% |

{kind=link}