Global market sentiment shows signs of stabilization in Asia today, marked by gains in major indices like Nikkei Hong Kong’s HSI. This shift indicates that the markets have largely absorbed the impact of Moody’s downgrade of China’s rating outlook, redirecting attention towards economic data and central bank policies. The spotlight is now on BoC’s interest rate decision and the release of US ADP private employment report.

In the currency markets, Australian Dollar is showing resilience, trading higher despite the release of GDP data that fell short of expectations. Canadian Dollar, meanwhile, is having a slight uptick as traders await BoC’s decision, speculating on whether the central bank will adopt a dovish stance given current economic conditions. However, the New Zealand Dollar is emerging as the strongest performer, outpacing its Australian and Canadian counterparts. Concurrently, Dollar, Euro, and Yen are showing signs of softening, while Sterling and Swiss Franc are mixed.

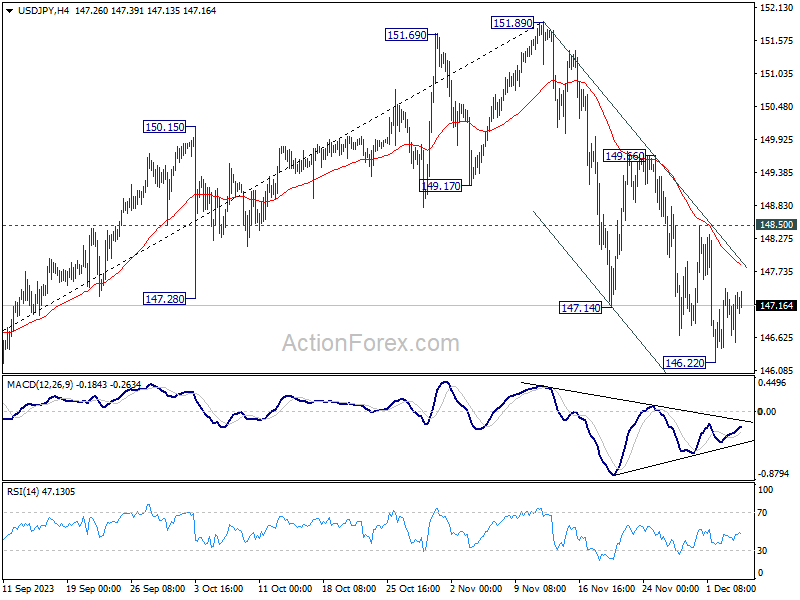

Technically, USD/JPY is staying in consolidation above 146.22 for now. Despite the steep decline in the US 10-year yield overnight, the pair has yet to react, but this could change with a delayed response. In any case, outlook will stay bearish as long as 148.50 resistance holds. Break of 146.22 temporary low will resume the fall from 151.89 to 145.06 key support level next.

In Asia, at the time of writing, Nikkei is up 1.92%. Hong Kong HSI is up 1.15%. China Shanghai SSE is up 0.12%. Singapore Strait Times is down -0.04%. Japan 10-year JGB yield is down -0.0322 at 0.640. Overnight, DOW fell -0.22%. S&P 500 fell -0.06%. NASDAQ rose 0.31%. 10-year yield fell -0.117 to 4.171.

Australia’s Q3 GDP growth slows to 0.2% qoq, per capita output declines

Australia’s GDP for Q3 showed a modest increase of 0.2% qoq, falling short of the expected 0.5% qoq growth. On a year-on-year basis, GDP grew by 2.1%. However, a contrasting picture emerges when considering GDP on a per capita basis, which revealed a decline of -0.5% qoq and a -0.3% yoy.

Katherine Keenan, ABS head of national accounts, said: “This was the eighth straight rise in quarterly GDP, but growth has slowed over 2023.” She pointed out that government spending and capital investment were the primary contributors to GDP growth in this quarter.

Specifically, government final consumption expenditure rose by 1.1%. Additionally, gross fixed capital formation also saw a 1.1% rise.

An interesting aspect of the September quarter’s GDP was the contribution of 0.4% points from changes in inventories. Notably, mining inventories increased by AUD 2.4B, a reflection of the larger fall in exports compared to production volumes.

On the other hand, trade in services had a negative impact on growth. Imports of services surged by 8.4%, significantly outpacing the 1.9% growth in services exports.

BoJ’s Himino stresses patience in monetary easing to prevent return to “frozen state”

BoJ Deputy Governor Ryozo Himino, in a speech today, affirmed the central bank’s commitment to continued monetary easing. He noted, “the Bank will patiently continue with monetary easing until sustainable and stable achievement of the price stability target, accompanied by wage increases, comes in sight.”

He acknowledged the positive changes in firms’ wage- and price-setting behavior, noting “solid progress” and “signs in the right direction.” However, he warned of the risks of reverting to a deflationary state if a virtuous cycle between wages and prices is not established.

Explaining further, Himino commented on the longstanding norm in Japan where neither wages nor prices could rise significantly. “Japan had worked for many years to break free from this,” he added, “and simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome either.”

Himino highlighted the longstanding norm in Japan where “neither wages nor prices could rise”. He stressed that Japan’s efforts to break free from this stagnation, adding, “simply returning to such a frozen state after the current high inflation comes down would not be a desirable outcome”.

He also outlined the multiple challenges facing Japanese monetary policy, including addressing current inflation, supporting moderate economic recovery, encouraging wage increases, and preventing a return to deflation. “The Bank is struggling to find a solution and this is by no means an easy task,” he admitted.

BoC set to stand pat, will dovish shift follow?

BoC is widely expected to hold overnight rate target steady at 5.00% today, amidst a backdrop of increasing economic challenges. Current market climate suggests the potential for a slightly dovish shift in the central bank’s statement. However, while there is speculation among some investors about the possibility of BoC commencing rate cuts as early as the second quarter of next year, it seems premature for the central bank to signal any definite intentions in this regard at the current juncture.

Governor Tiff Macklem’s recent comments have significantly influenced market expectations. He noted that “the excess demand in the economy that made it too easy to raise prices is now gone” and the economy is “approaching balance”. His observation that softening economic activity will exert “more downward pressure on inflation” and the acknowledgment that “interest rates may now be restrictive enough” have nearly eliminated the odds of further rate hikes.

In a recent Reuters poll, a majority of economists, specifically 18 out of 26, projected that BoC’s rate would decrease to 4.0% or lower by the end of 2024. Nevertheless, Macklem is expected to reiterate that discussions about rate cuts are still premature, indicating a cautious approach from the central bank in the face of uncertain economic conditions.

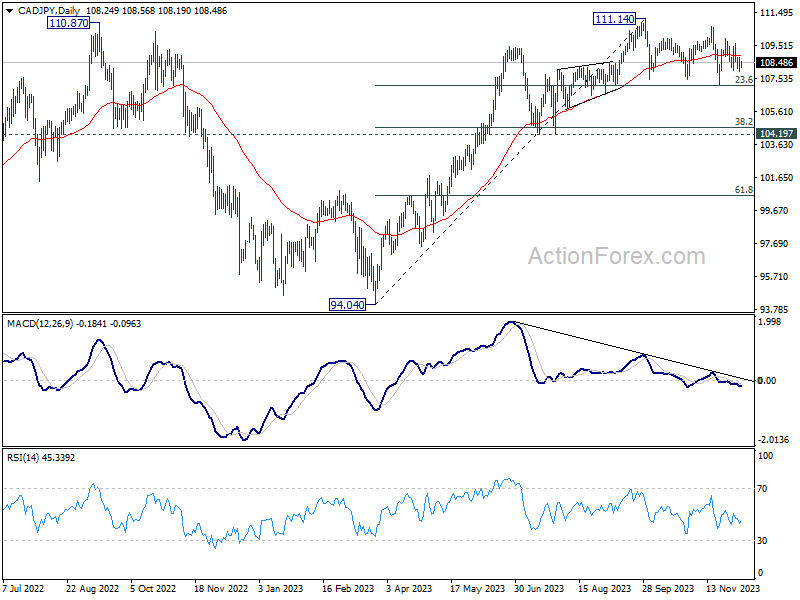

CAD/JPY has been bounded in range trading below 111.14 since September. The pull back is so far rather shallow as contained by 23.6% retracement of 94.04 to 111.14 at 107.10. There is not sign of trend reversal, and another rise through 111.14 is still in favor. However, considering bearish divergence condition in D MACD, upside potential could be relatively limited.

On the other hand, firm break of 107.10 could indicate that deeper decline is underway to 38.2% retracement of 104.60, or even further to 61.8% retracement at 100.57. However, such a significant decline would likely require concurrent dovish policy shifts from BoC and hawkish turn from BoJ, potentially materializing early in the next year.

Elsewhere

Germany factor orders, UK PMI construction, and Eurozone retail sales will be released in European session. Later in the day, US will release ADP employment and trade balance. In addition to BoC rate decision, Canada will release labor productivity, trade balance, and Ivey PMI.

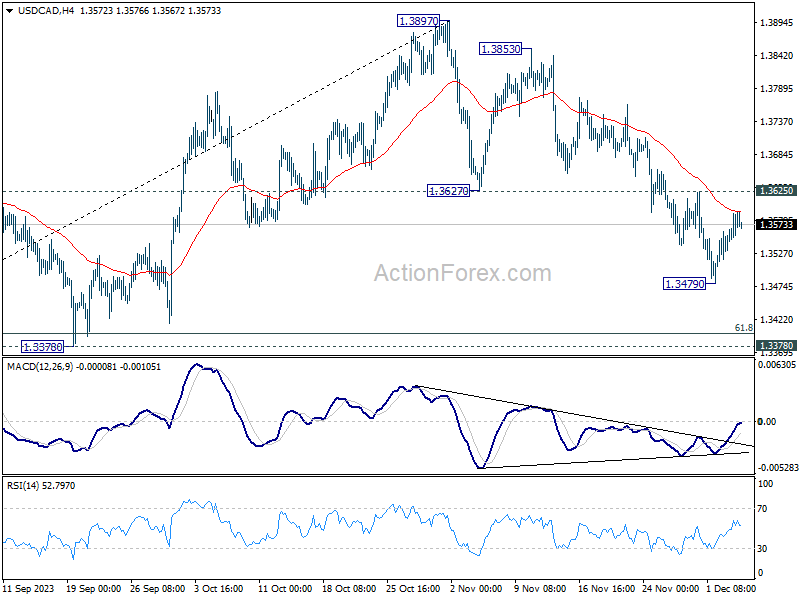

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3551; (P) 1.3574; (R1) 1.3615; More…

No change in USD/CAD’s outlook and intraday bias stays neutral at this point. Below 1.3479 will resume the corrective fall from 1.3897. But downside should be contained by 1.3378 support, which is close to 61.8% retracement of 1.3091 to 1.3897 at 1.3399, to bring rebound. On the upside, break of 1.3625 resistance will indicate short term bottoming, and turn bias back to the upside for stronger rise.

In the bigger picture, rise from 1.3091 is seen as the fifth leg of the whole rise from 1.2005 (2021 low). Further rally is expected as long as 1.3378 support holds, to 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. However, decisive break of 1.3378 will dampen this view and bring deeper fall back to 1.3091 instead.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.20% | 0.40% | 0.40% | |

| 07:00 | EUR | Germany Factory Orders M/M Oct | 0.50% | 0.20% | ||

| 09:30 | GBP | Construction PMI Nov | 47.1 | 45.6 | ||

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.20% | -0.30% | ||

| 13:15 | USD | ADP Employment Change Nov | 120K | 113K | ||

| 13:30 | CAD | Labor Productivity Q/Q Q3 | 0.20% | -0.60% | ||

| 13:30 | CAD | Trade Balance (CAD) Oct | 1.8B | 2.0B | ||

| 13:30 | USD | Trade Balance (USD) Oct | -63.0B | -61.5B | ||

| 13:30 | USD | Nonfarm Productivity Q3 | 4.70% | 4.70% | ||

| 13:30 | USD | Unit Labor Costs Q3 | -0.80% | -0.80% | ||

| 15:00 | CAD | BoC Rate Decision | 5.00% | 5.00% | ||

| 15:00 | CAD | Ivey PMI Nov | 54.2 | 53.4 | ||

| 15:30 | USD | Crude Oil Inventories | -1.3M | 1.6M |

{kind=link}