In the aftermath of US CPI release, the forex markets are staying in a state of consolidation, with mixed reactions. Initially, there was an attempt to sell Dollar following the data, but this momentum quickly dissipated as the data largely aligned with market expectations. Headline CPI showed a gradual decline, albeit at a slow pace, while core CPI indicated stagnant disinflation. It may not be the right time to place significant bets on the greenback yet, especially considering FOMC rate decision and publication of new economic projections scheduled for tomorrow. The anticipation of these events has left room for potential market shifts, keeping market players cautious for now.

In terms of overall market movements, the forex markets today are somewhat mixed, indicative of a typical consolidation mode. Dollar, Australian Dollar, and Canadian Dollar are leaning towards the softer side. In contrast, Japanese Yen is showing strength, attempting a rebound from this week’s pullback. Euro and Swiss Franc are also on the firmer side, while Sterling appears softer, influenced by UK job data that indicated further cooling in wage inflation.

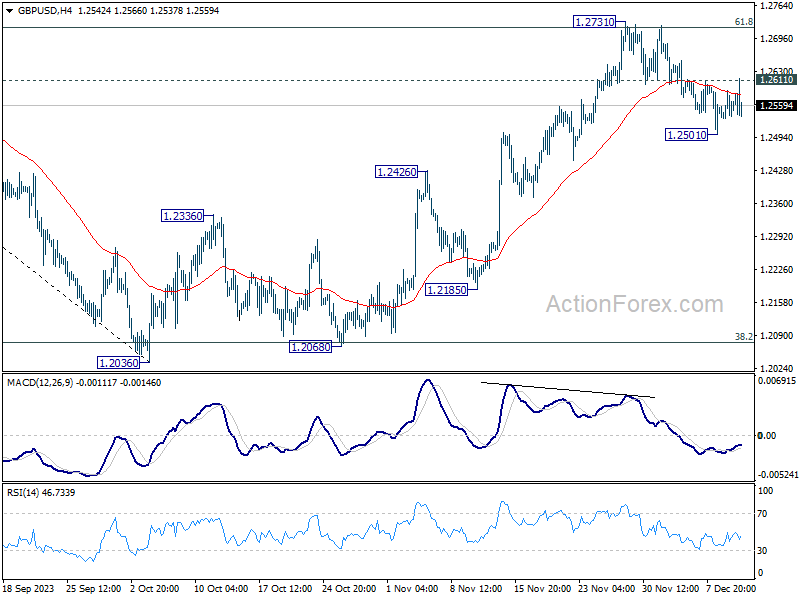

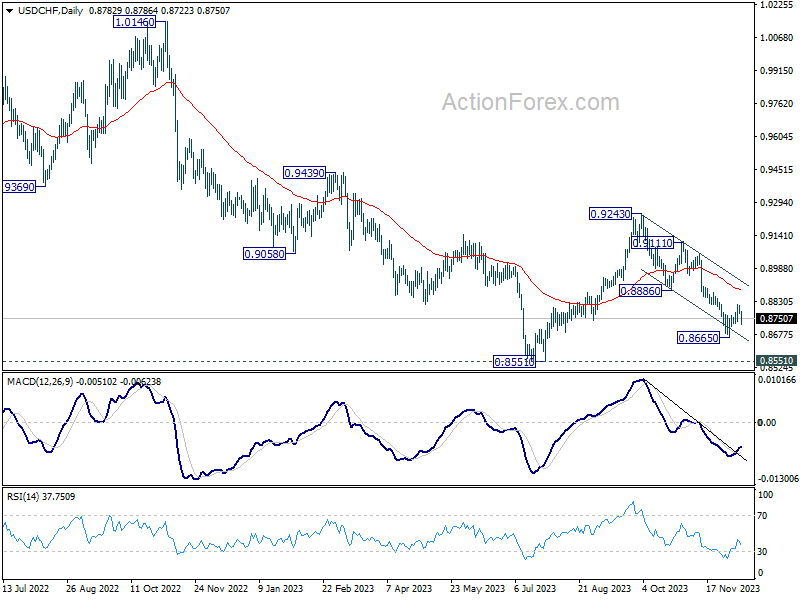

From a technical standpoint, Dollar’s rally against European majors remains a possibility, contingent on certain key levels holding in various Dollar pairs. These critical levels include 1.0816 minor resistance in EUR/USD, 1.2611 minor resistance in GBP/USD, and 0.8727 minor support in USD/CHF. Should these levels be decisively broken it could signal resurgence of broad-based Dollar weakness, or at least against Europeans.

In Europe, at the time of writing, FTSE is up 0.14%. DAX is down -0.10%. CAC is flat. Germany 10-year yield is down -0.0482 at 2.227. UK 10-year yield is down -0.099 at 3.980. Earlier in Asia, Nikkei rose 0.16%. Hong Kong HSI rose 1.07%. China Shanghai SSE rose 0.40%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield fell -0.0409 to 0.738.

US CPI ticks down to 3.1% in Nov, core CPI unchanged at 4%

The latest CPI data for US in November aligns closely with market expectations. CPI rose 0.1% mom while CPI core ex food and energy) rose 0.3% mom. Energy index down -2.3% mom, food index rose 0.2% mom.

For the 12 months period, CPI slowed from 3.2% yoy to 3.1% yoy. Core CPI was unchanged at 4.0% yoy. Energy index was down -5.4% yoy while food index was up 2.9% yoy.

German ZEW rises to 12.8 on increasing expectation of ECB rate cut

German ZEW Economic Sentiment rose slightly from 9.8 to 12.8 in December, above expectation of 8.8. Current Situation Index rose from -79.8 to -77.1, but missed expectation of -75.5.

Eurozone ZEW Economic Sentiment rose sharply from 13.8 to 23.0, well above expectation of 11.2. Current Situation Index, however, fell marginally by -0.9 pts to -62.7.

ZEW President Achim Wambach noted the slight improvement in Germany’s economic outlook could be attributed to doubled expectations of interest rate cuts by ECB in the medium term. In particular, significantly more optimistic expectations are observed in the construction industry.

UK payrolled employment fell -13k in Nov, unemployment rate steady at 4.2% in Oct

UK payrolled employment fell slightly by -13k in November, compared with October. Comparing with November 2022, payrolled employment rose 1.1% yoy or 333k. Meanwhile monthly pay increased by 5.3% yoy, slowed from 6.2% yoy.

In the three months to October, unemployment rate was unchanged at 4.2% yoy. Average earnings (including bonus) growth slowed from 8.0% yoy to 7.2% yoy, below expectation of 7.7% yoy. Average earnings (excluding bonus) growth slowed from 7.7% yoy to 7.3% yoy, below expectation of 7.4% yoy.

Australia’s Westpac consumer sentiment rose to 82.1, still far from upbeat

The latest release from Australia reveals a modest uptick in Westpac Consumer Sentiment Index, which rose by 2.7% mom to 82.1 in December. Despite this increase, Westpac’s analysis describes the sentiment as “still very weak,” emphasizing that “consumers remain far from upbeat.”

Regarding RBA’s next meeting on February 5-6, Westpac said, the “there is now a higher bar” to further tightening. It highlights the “subdued growth profile” and a “particularly weak household sector” underscored by the recent consumer sentiment results, suggesting that these factors might raise the threshold for another rate hike.

However, it’s important to note the central bank’s stance towards inflation. RBA has expressed a “very low tolerance for any upside surprises” in inflation rates, making the upcoming inflation data and the detailed quarterly release, due in late January, pivotal for February policy decision.

Australia’s NAB business confidence and conditions decline, signaling continued soft growth

Australia NAB Business Confidence fell from -3 to -9 in November. Business Conditions fell from 13 to 9. Trading conditions fell from 19 to 13. Profitability conditions fell from 11 to 6. Employment conditions were unchanged at 8.

NAB Chief Economist Alan Oster remarked, “Both confidence and conditions declined in the month and after a period of relative stability through mid-2023 appear to be softening further.” He pointed out that, excluding the pandemic period, business confidence is at its weakest since around 2012. This was a time characterized by significantly weaker conditions and slowing growth in advanced economies.

Despite these declines, Oster noted that business conditions remain above average, reflecting their strong starting point. He emphasized the importance of monitoring whether this drop in confidence continues and if a trend develops in business conditions. For the moment, these indicators suggest “ongoing soft growth in Q4”.

Japan’s PPI slows to weakest pace since February 2021

Japan’s PPI slowed notably from 0.9% yoy to 0.3% yoy in November, but beat expectation of 0.1% yoy. That’s nonetheless still the weakest pace since February 2021. November marked the 11th straight month in which the pace slowed.

Export prices was unchanged at 0.9% yoy. Import price decline slowed from -12.7% yoy to -9.7% yoy, staying negative for the eighth month.

During the month, PPI rose 0.2% mom. Import prices rose 0.7% mom. Export prices fell -0.2 %Mom.

Producer price growth stayed below the most recent consumer inflation reading for a third month. Growth in consumer prices excluding fresh food inched up to 2.9% in October.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8770; (P) 0.8793; (R1) 0.8807; More….

Intraday bias in USD/CHF stays neutral at this point. Further rise remains in favor with 0.8727 minor support intact. Above 0.8819 will resume the rebound from 0.8665 short term bottom to 0.8886 support turned resistance first. However, firm break of 0.8727 will retain near term bearishness, and turn bias back to the downside to resume the fall from 0.9243 through 0.8665.

In the bigger picture, price actions from 0.8551 are currently seen as part of a corrective pattern to the decline from 1.0146 (2022 high). Fall from 0.9243 is seen as the second leg for now. Deeper decline could be seen to 0.8551 low but strong support should be seen there to bring rebound. Meanwhile, break of 0.9111 resistance will argue that the third leg has started already, and target 0.9243 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 2.70% | -2.60% | ||

| 23:50 | JPY | PPI Y/Y Nov | 0.30% | 0.10% | 0.80% | 0.90% |

| 00:30 | AUD | NAB Business Confidence Nov | -9 | -2 | -3 | |

| 00:30 | AUD | NAB Business Conditions Nov | 9 | 13 | ||

| 07:00 | GBP | Claimant Count Change Nov | 16.0K | 20.3K | 17.8K | 8.9K |

| 07:00 | GBP | ILO Unemployment Rate (3M) Oct | 4.20% | 4.20% | 4.20% | |

| 07:00 | GBP | Average Earnings Including Bonus 3M/Y Oct | 7.20% | 7.70% | 7.90% | 8.00% |

| 07:00 | GBP | Average Earnings Excluding Bonus 3M/Y Oct | 7.30% | 7.40% | 7.70% | |

| 10:00 | EUR | Germany ZEW Economic Sentiment Dec | 12.8 | 8.8 | 9.8 | |

| 10:00 | EUR | Germany ZEW Current Situation Dec | -77.1 | -75.5 | -79.8 | |

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Dec | 23 | 11.2 | 13.8 | |

| 11:00 | USD | NFIB Business Optimism Index Nov | 90.6 | 90.7 | 90.7 | |

| 13:30 | USD | CPI M/M Nov | 0.10% | 0.10% | 0.00% | |

| 13:30 | USD | CPI Y/Y Nov | 3.10% | 3.10% | 3.20% | |

| 13:30 | USD | CPI Core M/M Nov | 0.30% | 0.30% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 4.00% | 4.00% | 4.00% |

{kind=link}