Dollar was sold off overnight after weaker than expected ISM Services data, and the weakness persisted following comments from Fed Chair Jerome Powell. Powell downplayed the significance of recent robust labor and inflation figures, suggesting them as fluctuations in “bumpy road” of moderating demand and inflation. This narrative reinforces the market’s anticipation that Fed is still leaning towards three rate cuts this year over just two. Though, the upcoming non-farm payroll data remains crucial for further adjustments in these expectations.

In the broader currency markets risk-on sentiment seems to prevail, more evident in the commodity markets than in equities. Australian dollar leads as the strongest currency for the week so far, fueled by significant rally in commodities like Copper. New Zealand dollar follows as the second strongest. Japanese Yen languishes as the weakest, with Swiss Franc and Dollar also underperforming.

Euro, Sterling, and Canadian Dollar occupy the middle ground in the currency spectrum, with Euro slightly edging out after surviving lower-than-expected Eurozone CPI data yesterday. Attention now shifts to release of ECB minutes today. But it is unlikely that they will offer any groundbreaking revelations given ECB officials’ clear communication regarding the consensus for June first rate cut.

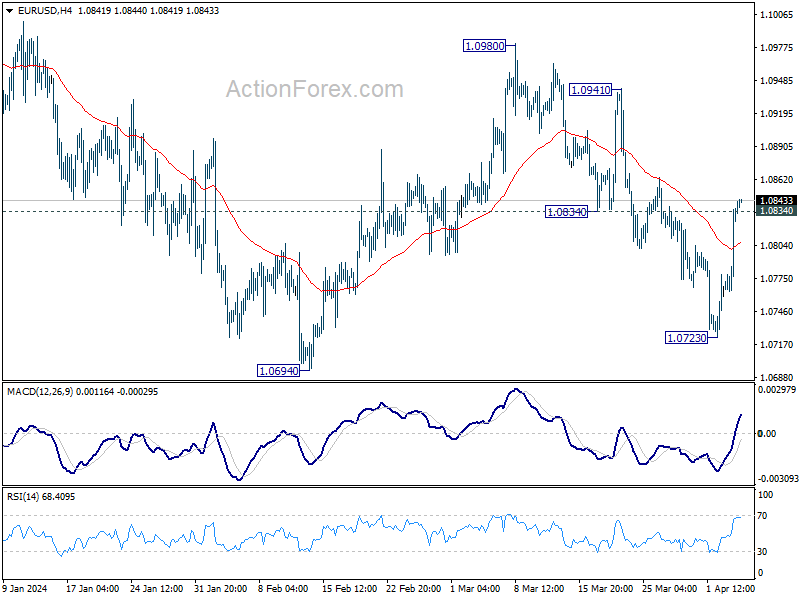

Technically, it now looks like EUR/USD’s fall from 1.0980 has completed with three waves down to 1.0723, ahead of 1.0694 support. Further rally would be mildly in favor as long as 55 4H EMA (now at 1.0805) holds, for 1.0941/80 resistance zone. But sustained break of the EMA will argue that rise from 1.0723 is merely a brief recovery and bring retest of 1.0694/0723 support zone instead.

In Asia, at the time of writing, Nikkei is up 1.27%. Japan 10-year JGB yield is up 0.0114 at 0.778. Singapore Strait Times is up 0.61%. Hong Kong and China are on holiday. Overnight, DOW fell -0.11%. S&P 500 rose 0.11%. NASDAQ rose 0.23%. 10-year yield fell -0.010 to 4.355.

Fed Powell downplays significance of recent strong labor market and inflation data

Fed Chair Jerome Powell downplayed the significance of recent labor market and inflation data that surpassed expectations, he noted that these developments do not significantly alter the Fed’s overall economic outlook.

“Recent readings on both job gains and inflation have come in higher than expected,” Powell said at a forum at Stanford University overnight. However, he was quick to clarify that these developments do not fundamentally shift the broader economic narrative, which he described as “one of solid growth, a strong but rebalancing labor market, and inflation moving down toward 2 percent on a sometimes bumpy path.”

In discussing the Federal Reserve’s approach to monetary policy easing, Powell affirmed the “meeting by meeting” decision-making process and acknowledged that rate cuts are “likely to be appropriate at some point this year.”

Yet, he stressed the prerequisite of having “greater confidence” in inflation’s downward path towards 2% target before any interest rate red reduction would be considered.

“Given the strength of the economy and progress on inflation so far, we have time to let the incoming data guide our decisions on policy,” he remarked.

Fed’s Kugler expects rate cut this year amid cooling demand

Fed Governor Adriana Kugler said overnight that if the disinflation process and labor market conditions evolve in line with her current expectations, a policy rate reduction within the year could be warranted.

“With demand growth cooling, given the backdrop of solid supply, my baseline expectation is that further disinflation can be accomplished without a significant rise in unemployment,” Kugler stated

“If disinflation and labor market conditions proceed as I am currently expecting, then some lowering of the policy rate this year would be appropriate,” she remarked.

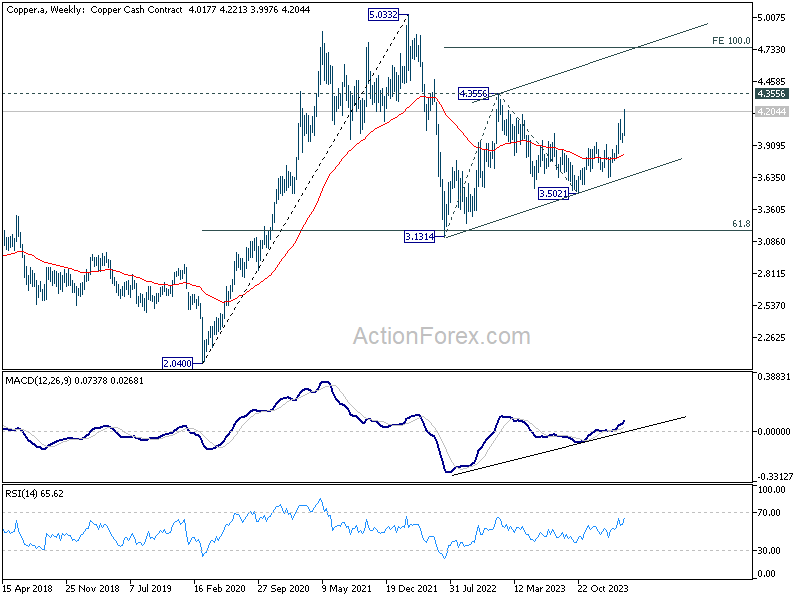

Copper hits yearly high on global growth optimism

Copper soars to the highest levels in over a year this year, driven by renewed optimism regarding global economic growth and expectations of monetary easing from the world’s major central banks. This surge reflects growing confidence among investors that the downturn in manufacturing, including even China, may have past its worst. The prospect of interest rate cuts this year further fuels this positive mood for commodities like copper.

Technically, Copper’s rally from 3.5021 resumed this week and it’s now on track to 161.8% projection of 3.5021 to 3.9346 from 3.6324 at 4.3322, which is close to 4.3556 (2023 high). In any case, outlook will stay bullish as long as 3.9380 support holds. The bigger question is whether Copper is indeed resuming the rise from 3.1314 (2022 low) too. Let’s see.

Looking ahead

Swiss CPI, Eurozone PMI services final and PPI, UK PMI services final will be released in European session. But more focus would likely be on ECB minutes.

Later in the day, US and Canada will release trade balance while US will also publish jobless claims.

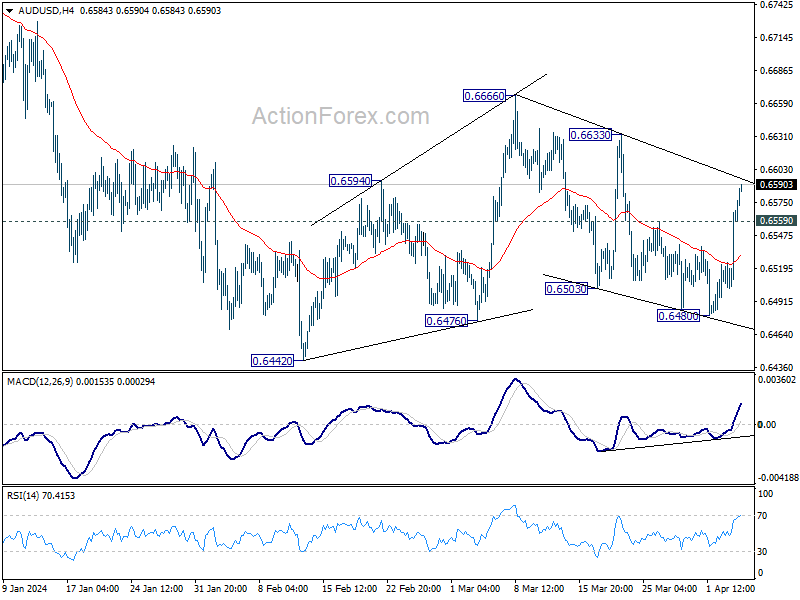

AUD/USD Daily Report

Daily Pivots: (S1) 0.6523; (P) 0.6546; (R1) 0.6590; More….

AUD/USD’s strong break of 55 D EMA suggests that fail from 0.6666 has completed with three waves down to 0.6480. Rise from there is now seen as the third leg of the corrective pattern from 0.6442. Intraday bias is back on the upside for 0.6633 resistance first. Break there will target 0.6666 and above. On the downside, though, below 0.6559 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which might still be in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 14.90% | -8.80% | -8.60% | |

| 00:30 | AUD | Building Permits M/M Feb | -1.90% | 3.20% | -1.00% | -2.50% |

| 06:30 | CHF | CPI M/M Mar | 0.30% | 0.60% | ||

| 06:30 | CHF | CPI Y/Y Mar | 1.40% | 1.20% | ||

| 07:45 | EUR | Italy Services PMI Mar | 53.2 | 52.2 | ||

| 07:50 | EUR | France Services PMI Mar F | 47.8 | 47.8 | ||

| 07:55 | EUR | Germany Services PMI Mar F | 49.8 | 49.8 | ||

| 08:00 | EUR | Eurozone Services PMI Mar F | 51.1 | 51.1 | ||

| 08:30 | GBP | Services PMI Mar | 53.4 | 53.4 | ||

| 09:00 | EUR | Eurozone PPI M/M Feb | -0.70% | -0.90% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Feb | -8.60% | -8.60% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | 8.80% | |||

| 11:30 | EUR | ECB Meeting Accounts | ||||

| 12:30 | CAD | Trade Balance (CAD) Feb | 0.5B | 0.5B | ||

| 12:30 | USD | Trade Balance (USD) Feb | -66.0B | -67.4B | ||

| 12:30 | USD | Initial Jobless Claims (Mar 29) | 212K | 210K | ||

| 14:30 | USD | Natural Gas Storage | -42B | -36B |

{kind=link}