Australian Dollar trades broadly higher today, lifted partly by resurgence in risk sentiment, as well as robust PMI data reflecting the cyclical recovery in Australian economy. Improvement in the economic outlook reduces the immediate need of a rate cut by RBA. Judo Bank, who complied the PMI data, warned about the possibility for another rate hike if economic activity continues to pick up while inflation remains elevated.

Additionally, there is growing concern among financial analysts that should Australia begin to see acceleration in inflation similar to recent trends in the US, more monetary tightening might be need. For now, though, the consensus holds that the bar for another RBA rate increase remains high.

Japanese yen is the second strongest currency today, though its momentum is relatively weak. Comments from Japan indicating readiness for currency intervention have so far elicited muted responses from the markets. Nonetheless, increasing concerns are being voiced about the weaker Yen driving up prices, which would eventually leading to further tightening by BoJ. Nonetheless, market focus will be directed to BoJ’s upcoming economic projections this Friday first.

In other currency markets, movements are mixed. Swiss Franc, New Zealand Dollar, and Dollar are weaker for the day at this point. Euro and British Pound are mixed together with Canadian Dollar. The financial community is now turning its attention to PMI data from Eurozone, UK, and US.

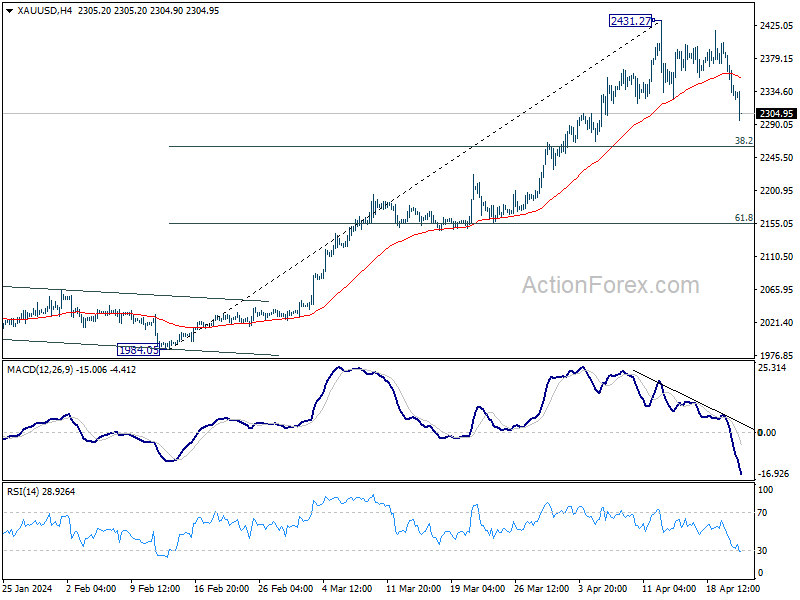

Technically, Gold’s correction from 2431.27 short term top continues lower today. Further fall is expected but strong support should be seen from 38.2% retracement of 1984.05 to 2431.27 at 2260.43 to bring rebound. Another rally through 2431.27 to test 2500 mark is still expected before a major top is formed around there. However, sustained break of 2260.43 will raise that chance that Gold is already in a larger scale correction.

In Asia, at the time of writing, Nikkei is up 0.46%. Hong Kong HSI is up 1.64%. China Shanghai SSE is down -0.41%. Singapore Strait Times is up 1.22%. Japan 10-year JGB yield is up 0.004 at 0.890. Overnight, DOW rose 0.67%. S&P 500 rose 0.87%. NASDAQ rose 1.11%. 10-year yield rose 0.0008 to 4.623.

Australia’s PMI Composite rises to 53.6, RBA might hike again in H2

Australia’s PMI Manufacturing has nearly reached the neutral mark in April, jumping from 47.3 to 49.9. PMI Services edged higher from 54.2 to 54.4, contributing to PMI’s Composite rise from 53.3 to 53.6, marking a 24-month high and indicating the third consecutive month of expansion.

Warren Hogan, Chief Economic Advisor at Judo Bank, said that Composite PMI has averaged 51.5 over Q1, a substantial improvement from 46.9 average in Q4 2023 and correlates with GDP growth of around 0.6% for the March quarter. Hogan suggested that if this trend persists, GDP growth could accelerate to approximately 0.8% in the following quarter.

The results also suggest a cyclical recovery, rebounding from the consumer-led slowdown experienced in 2023. This recovery appears to be more robust than anticipated by RBA, suggesting that the economy is beginning to “wander off their ‘narrow path'”. This “narrow path” scenario envisages economic activity remaining subdued to ensure inflation eases back to target by late 2025

“The RBA will likely be concerned that a pick-up in activity, before inflation returns to target, could threaten medium to long-term price stability,” Hogan added. “These results are inconsistent with interest rate reductions at any stage in the foreseeable future and raise the risk that the RBA may have to start hiking again at some stage over the back half of 2024.”

BoJ’s Ueda: No preset idea on rate hikes

Addressing the parliament today, BoJ Governor Kazuo Ueda said while changes in inflation projections could necessitate a shift in monetary policy, the BoJ currently has no “preset idea on the specific timing and pace” of rate hikes.

Governor Ueda also reiterated the necessity of maintaining ultra-loose monetary policy for now. He pointed out that trend inflation — price rises driven by domestic demand and assessed through various indicators — is still “somewhat below 2%.”

Japan’s Suzuki points to US-South Korea trilateral meeting as groundwork for Yen intervention

Japan’s Finance Minister Shunichi Suzuki signaled the readiness to address the weakening yen, a pressing issue that has raised substantial concern due to its impact on import costs.

Speaking to the parliament, Suzuki conveyed the unease discussed during last week’s trilateral meeting with the US and South Korea. He emphasized the economic strain caused by the depreciating currency, stating there was “strong concern” about how a weak yen inflates the cost of imports, stressing the economy and affecting price levels domestically.

Suzuki’s remarks indicated that preparations are underway to counteract Yen’s decline. “I won’t deny that these developments have laid the groundwork for Japan to take appropriate action,” he noted, “though I won’t say what that action could be”.

Japan’s PMI Composite climbs to 52.6, weak Yen contributes to intensifying price pressures

Japan’s PMI Manufacturing rises from 48.2 to 49.9 in April, above expectation of 48.0, signalling a near-stabilization of manufacturing business conditions. PMI Services rises from 54.1 to 54.6, highest since May 2023. PMI Composite also rose from 51.7 to 52.6, matching the joint-fastest pace set in nearly a year.

Jingyi Pan, Economist Associate Director at S&P Global Market Intelligence, noted that while the service sector continues to be the main driver of growth, there are positive developments in manufacturing as well, where the decline in output has lessened.

April’s data, however, also unveiled “additional signs of intensifying price pressures” which were largely attributed to higher input costs inflation affecting both the goods and services sectors.

Notable factors contributing to these rising costs include increased expenses for materials, energy, and wages, with the “weaker Yen having played a significant part as well”. Consequently, businesses have been compelled to pass these increased costs onto their clients, resulting in the “fastest increase in average charges in a year.”

AUD/USD Daily Report

Daily Pivots: (S1) 0.6423; (P) 0.6439; (R1) 0.6465; More…

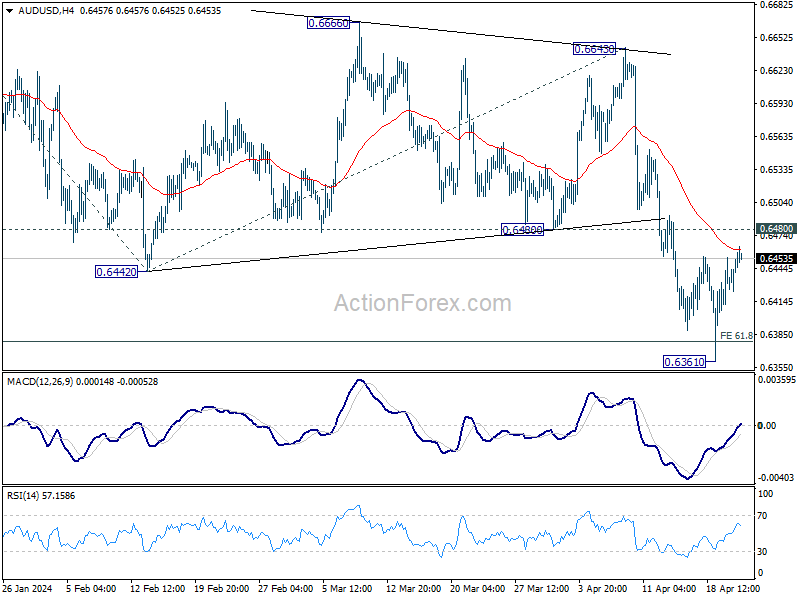

AUD/USD’s recovery from 0.6361 continues today but stays below 0.6480 support turned resistance. Intraday bias remains neutral first. Upside is still expected to be limited by 0.6480 support turned resistance to bring another decline. On the downside, break of 0.6361 will resume the fall from 0.6870 to 100% projection of 0.6870 to 0.6442 from 0.6643 at 0.6215. Nevertheless, sustained break of 0.6480 will bring stronger rebound to 55 D EMA (now at 0.6527).

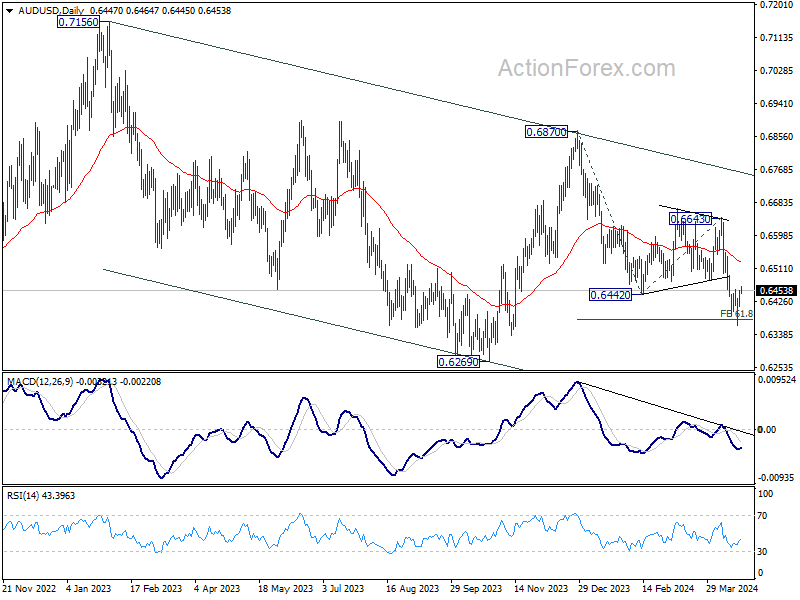

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which is still in progress. Overall, sideway trading could continue in range of 0.6169/7156 for some more time. But as long as 0.7156 holds, an eventual downside breakout would be mildly in favor.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Apr P | 49.9 | 47.3 | ||

| 23:00 | AUD | Services PMI Apr P | 54.2 | 54.4 | ||

| 00:30 | JPY | Manufacturing PMI Apr P | 49.9 | 48 | 48.2 | |

| 00:30 | JPY | Services PMI Apr P | 54.6 | 54.1 | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Mar | 8.9B | 7.5B | ||

| 07:15 | EUR | France Manufacturing PMI Apr P | 46.9 | 46.2 | ||

| 07:15 | EUR | France Services PMI Apr P | 49 | 48.3 | ||

| 07:30 | EUR | Germany Manufacturing PMI Apr P | 42.9 | 41.9 | ||

| 07:30 | EUR | Germany Services PMI Apr P | 50.5 | 50.1 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Apr P | 46.5 | 46.1 | ||

| 08:00 | EUR | Eurozone Services PMI Apr P | 51.8 | 51.5 | ||

| 08:30 | GBP | Manufacturing PMI Apr P | 50.2 | 50.3 | ||

| 08:30 | GBP | Services PMI Apr P | 53 | 53.1 | ||

| 13:45 | USD | Manufacturing PMI Apr P | 52 | 51.9 | ||

| 13:45 | USD | Services PMI Apr P | 52 | 51.7 | ||

| 14:00 | USD | New Home Sales Mar | 668K | 662K |

{kind=link}