Tuesday’s Asian and European sessions saw little conviction across even when geopolitical conflicts in the Middle East persisted. The Israel-Iran conflict, now into its fifth day, is generating concern but not yet panic. Oil and gold, typically sensitive to regional instability, remain rangebound, and equities are slightly softer with no meaningful follow-through on the downside.

Currency markets are similarly directionless. Kiwi and Aussie are leading the day, followed by Yen. Sterling is underperforming, alongside Dollar and Euro. Swiss Franc and Loonie sit in the middle of the pack. This mixed profile speaks to an underlying sense of hesitation.

BoJ’s meeting produced little market reaction, but the newly outlined bond tapering plan has drawn some quiet praise. By mapping out a gradual reduction in JGB purchases for fiscal 2026, BoJ has signaled a willingness to act should long-end yields rise sharply again. While the move is more of a gesture at this stage, it has added to the perception that BoJ full ready a more flexible stance.

With the BoJ out of the way, investor focus now shifts firmly to Fed. While rates are expected to remain unchanged, markets will be parsing Chair Powell’s language closely for any signs of movement on timing for next rate cuts. Meanwhile, BoE and SNB will follow on Thursday, rounding out a critical week for central bank actions.

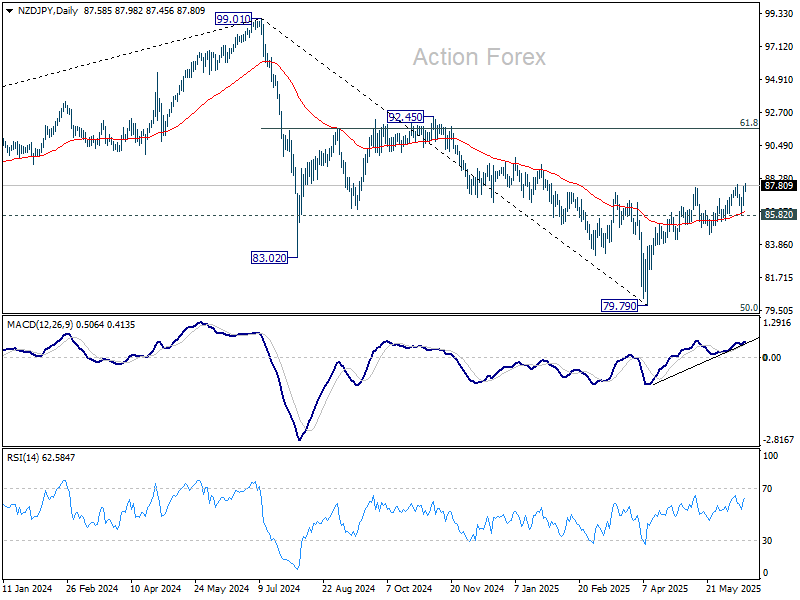

Technically, NZD/JPY is trying to resume the rebound from 79.79. The strong support from 55 D EMA (now at 86.07) keeps near term outlook mildly bullish. The development also affirms the case that whole corrective fall from 99.01 has completed with three waves down to 79.79. Further rally is expected as long as 85.82 support holds, towards 61.8% retracement of 99.01 to 79.79 at 91.66.

In Europe, at the time of writing, FTSE is down -0.33%. DAX is down -0.78%. CAC is down -0.59%. UK 10-year yield is down -0.003 at 4.531. Germany 10-year yield is down -0.002 at 2.523. Earlier in Asia, Nikkei rose 0.59%. Hong Kong HSI fell -0.34%. China Shanghai SSE fell -0.04%. Singapore Strait Times rose 0.57%. Japan 10-year JGB yield rose 0.019 to 1.473.

US retail sales drop sharply by -0.9% mom in May

US retail sales declined more than expected in May, falling -0.9% month-on-month to USD 715.4B, well below the forecasted -0.6% mom drop.

The weakness was broad-based, with ex-auto sales falling -0.3% mom and ex-gasoline sales down -0.8% mom. Even the core control group—excluding autos and gasoline—registered a -0.1% mom decline, suggesting slowing momentum in discretionary consumption.

Despite a solid 4.5% yoy gain for the March–May period, today’s figures raise fresh doubts about the strength of US consumer spending heading into the summer.

German ZEW surges to 47.5, points to post-stagnation recovery

Investor confidence in the Eurozone surged in June, with ZEW Economic Sentiment readings for both Germany and the wider region easily beating expectations.

Germany’s headline sentiment index jumped from 25.2 to 47.5, well above the expected 34.5, while the current situation gauge improved from -82 to -72. Eurozone-wide, sentiment rose from 11.6 to 35.3, and the current conditions index climbed 11.7 points to -30.7.

ZEW President Achim Wambach attributed the “tangible improvement” to growth in investment and consumer demand, adding that fiscal policy announcements from Germany’s new government appear to be supporting confidence.

The data suggests that the prolonged period of stagnation in Europe’s largest economy may be nearing an end. Combined with the ECB’s recent interest rate cuts, momentum may be building toward a long-awaited recovery.

BoJ maintains policy, expects gradual rebound in inflation after near term weakness

BoJ kept its short-term interest rate unchanged at 0.5% in a unanimous decision today, while sticking with its current bond tapering program through March 2026. Looking further out, the central bank introduced a new bond purchase schedule for fiscal 2026, planning to reduce monthly purchases by JPY 200B each quarter, bringing the total to JPY 2T per month by March 2027.

In its statement, the BoJ downgraded its growth outlook, noting that Japan’s economy is “likely to moderate” in the near term as overseas economies slow and domestic corporate profits weaken. While accommodative financial conditions should provide some support, the central bank only expects a modest recovery later as global growth returns.

On inflation, the impact from food and import price increases is “expected to wane”, while underlying CPI is likely to remain “sluggish” due to a slowing economy. However, the bank anticipates that inflation will gradually pick up over time, supported by rising medium- to long-term inflation expectations and a growing “sense of labor shortage” as the economy recovers.

BoJ also acknowledged “extremely uncertain” outlook around the global trade and policy environment, warning of spillovers to Japan’s financial markets and inflation outlook. The statement emphasized the need to closely monitor foreign exchange developments and their broader implications.

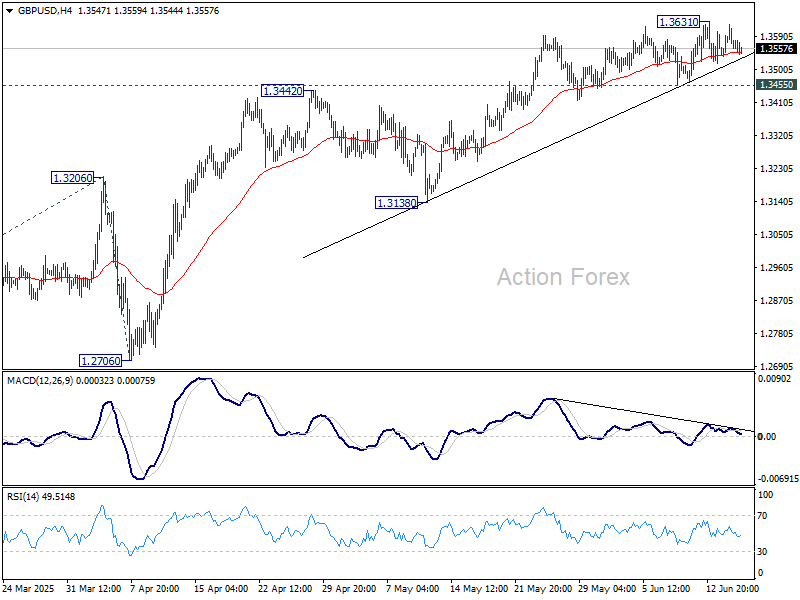

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3534; (P) 1.3578; (R1) 1.3621; More…

Intraday bias in GBP/USD stays neutral as consolidations continue below 1.3631 temporary top. With 1.3455 support intact, further rally is in favor. On the upside, break of 1.3631 will resume the rally from 1.2099 and target 100% projection of 1.2099 to 1.3206 from 1.3138 at 1.3813. On the downside, break of 1.3455 support should confirm short term topping, and bring deeper correction to 55 D EMA (now at 1.3320) instead.

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2937) holds, even in case of deep pullback.

{kind=link}