Dollar fell sharply overnight and extended its slide through Tuesday’s Asian session, as traders responded to dovish Fed commentary and easing geopolitical risks. Vice Chair Michelle Bowman signaled she would support a rate cut as soon as July if inflation pressures remain contained and labor market data weakens further. Her comments followed similar remarks from Governor Christopher Waller last week, suggesting the dovish wing of the FOMC may now be gaining traction.

Market pricing for a July cut jumped notably, rising from just 15% a day ago to around 25%. The timing couldn’t be more important, with Fed Chair Jerome Powell set to deliver his semiannual testimony to Congress starting today. If Powell signals any openness to a near-term rate cut, it would mark a meaningful departure from the Fed’s recent cautious stance, and potentially trigger another leg lower for the greenback this week.

A parallel driver of Dollar’s weakness is the reversal in geopolitical sentiment. Oil prices’ plunged after restrained retaliation by Iran. The sell off then intensified after US President Trump declared a ceasefire between Israel and Iran, triggering a further unwind in long crude positions. Although Iran launched final salvos of missiles after the announcement, Iranian state media framed the response as complete, reinforcing the view that tensions may be easing. That was enough to support a return to risk-on positioning in Asian markets and further erode Dollar’s safe haven appeal.

Trade developments also remain in focus. Japan’s top tariff negotiator Ryosei Akazawa is preparing to visit Washington for a new round of talks beginning June 26. The visit comes as Japanese officials press for relief from US tariffs on auto exports—a key pain point for Tokyo. The upcoming meeting will be the first high-level engagement since the June 16 summit between Prime Minister Shigeru Ishiba and President Trump, which failed to yield a breakthrough.

Meanwhile, Canada and the EU are reinforcing their transatlantic alliance through a new defense partnership. Canadian Prime Minister Carney reaffirmed Ottawa’s commitment to working with Brussels but maintained a cautious stance on US trade talks, reiterating that only the “right deal” would be acceptable.

In the currency markets, Dollar is now the weakest performer this week, followed by Loonie and Yen. Sterling leads the gains, while Kiwi and Swiss Franc follow. Euro and Aussie are positioning in the middle.

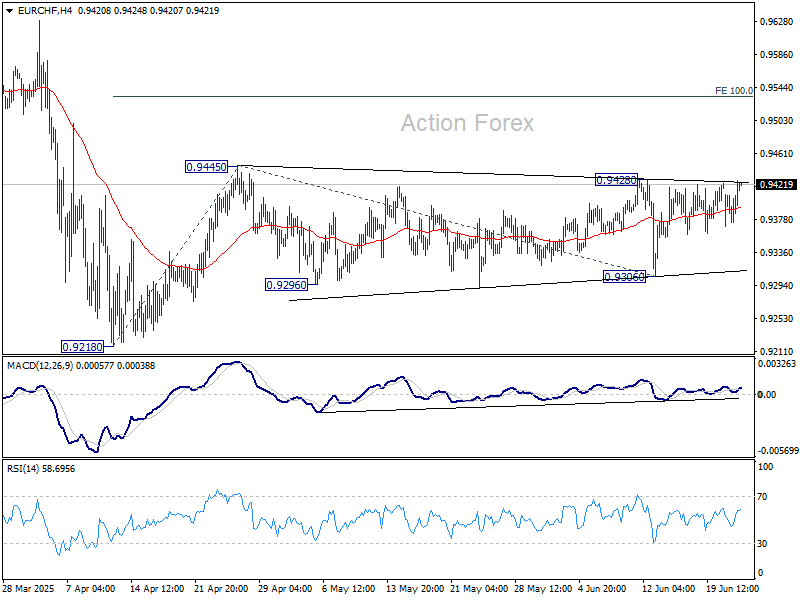

Technically, as geopolitical fears fade, EUR/CHF could be poised for an upside breakout. Firm break of 0.9428/45 resistance zone will resume whole rebound from 0.9218 and target 100% projection of 0.9218 to 0.9445 from 0.9306 at 0.9533. That would likely be accompanied by break of 1.1630 resistance in EUR/USD.

In Asia, at the time of writing, Nikkei is up 1.18%. Hong Kong HSI is up 2.17%. China Shanghai SSE is up 1.07%. Singapore Strait Times is up 0.51%. Japan 10-year JGB yield is up 0.006 at 1.417. Overnight, DOW rose 0.89%. S&P 500 rose 0.96%. NASDAQ rose 0.94%. 10-year yield fell -0.055 to 4.320.

Oil crashes on ceasefire hopes, market unwinds war premium

Oil prices plunged overnight as markets reassessed geopolitical risk following what appears to be a restrained Iranian response to US strikes and a potential ceasefire between Iran and Israel. WTI tumbled sharply after reports that Iranian forces attacked a US base in Qatar—an incident that was intercepted with no reported casualties. The muted retaliation defused immediate fears of further escalation, setting the stage for a pullback in crude. Sentiment turned further when US President Donald Trump declared a 12-hour ceasefire between Israel and Iran, announcing the end of what he called the “12 Day War.”

Technically, nonetheless, the steep selloff in WTI should have marked the complete of the whole rebound from 55.20 low at 78.87, well ahead of 81.01 key structural resistance. Short covering could come at around 61.8% retracement of 55.20 to 78.87 at 64.24, and bring bounce. That should set the range of sideway trading in the near term between 64/79.

Fed’s Goolsbee: Tariff impact milder than feared, cuts still on the table

Chicago Fed President Austan Goolsbee struck a cautiously optimistic tone Monday, saying that the recent surge in tariffs has not delivered the economic shock many had feared.

Speaking at a mid-year business outlook event in Milwaukee, Goolsbee noted that the fallout so far has been “somewhat surprisingly” modest, particularly in terms of inflation. While uncertainty remains around future price pressures, the current evidence suggests that the economy may still be on a favorable course.

“If we do not see inflation resulting from these tariff increases,” Goolsbee said, “then, in my mind, we never left what I was calling the golden path before April 2.” That path—defined by disinflation without a major slowdown—would support the case for eventual rate cuts.

His remarks echo a growing sentiment within the Fed that policy easing could resume later this year, provided inflation continues to behave and growth risks mount.

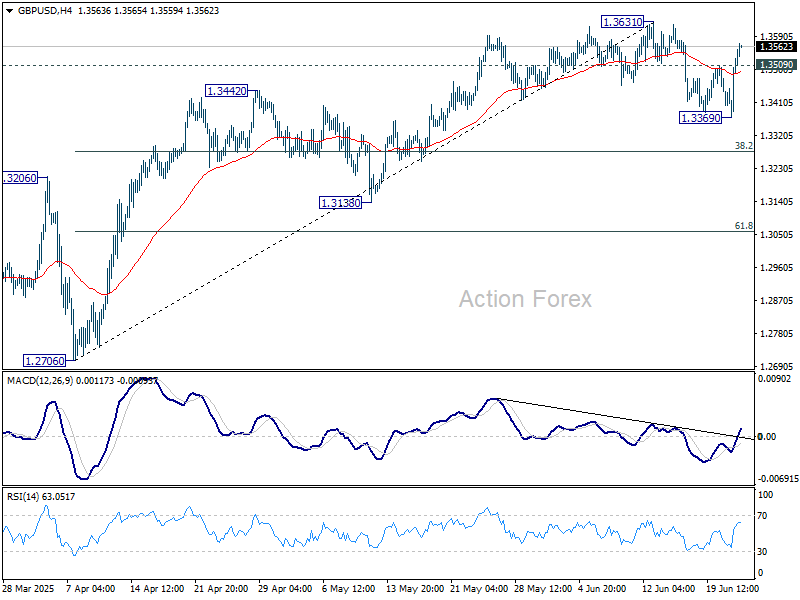

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3420; (P) 1.3475; (R1) 1.3580; More…

GBP/USD’s strong rebound suggest that pullback from 1.3631 has already completed at 1.3369. Intraday bias is back on the upside for retesting 1.3631 first. Firm break there will resume larger rally to 1.4004 projection level next. Nevertheless, break of 1.3369 will extend the correction with another falling leg instead.

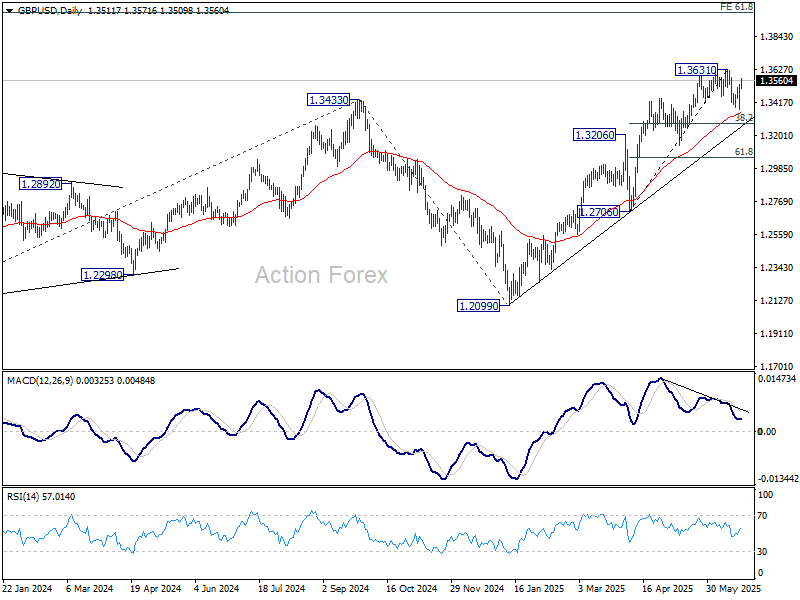

In the bigger picture, up trend from 1.3051 (2022 low) is in progress. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Outlook will now stay bullish as long as 55 W EMA (now at 1.2948) holds, even in case of deep pullback.

{kind=link}