The ongoing US government shutdown has done little to rattle investor sentiment so far. Wall Street shrugged off the impasse, with the S&P 500 closing at a fresh record high overnight while DOW and NASDAQ also advanced. In Asia, risk appetite carried through as Hong Kong surged on its return from holiday and Japan’s Nikkei once again tested the 45,000 handle.

Despite the upbeat mood, political deadlock in Washington shows no sign of resolution. With the Senate out of session today for Yom Kippur, the shutdown will stretch at least three days. The longer the standoff drags on, the greater the risk that Friday’s highly anticipated nonfarm payrolls report will be delayed, leaving ISM Services as the only key US release left this week.

In currency markets, Yen remains the strongest performer, underpinned by rising speculation that the BoJ could deliver a rate hike as early as this month. The resilience of recent business surveys has emboldened hawks on the policy board, keeping traders positioned for a potential move. Commodity currencies are also benefitting from the regional risk-on tone, with Aussie and Kiwi advancing in tandem with equities.

In contrast, Swiss Franc lags at the bottom of the performance table. Today’s CPI print is expected to remain firm enough to support the SNB’s decision to hold rates at 0.00%, reinforcing its reluctance to return to negative policy settings. The Loonie is also soft, with Dollar only slightly stronger, leaving both near the bottom of the pack. Euro and Sterling are mid-range, though the Pound maintains an edge on expectations that UK fiscal policy adjustments could provide support ahead of the November budget.

In Asia at the time of writing, Nikkei is up 1.17%. Hong Kong HSI is up 1.65%. China is still on holiday. Singapore Strait Times is up 1.70%. Japan 10-year JGB yield is up 0.006 at 1.659. Overnight, DOW rose 0.09%. S&P 500 rose 0.34%. NASDAQ rose 0.42%. 10-year yield yield fell -0.042 to 4.106.

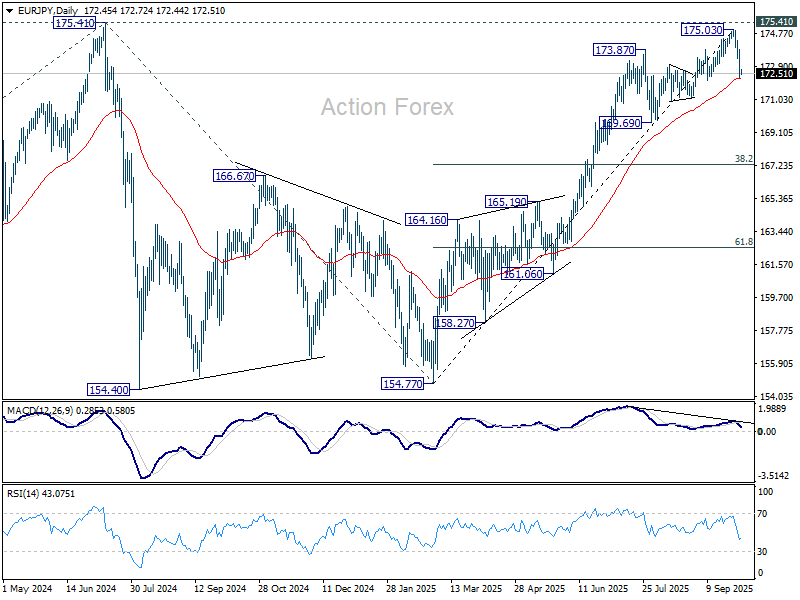

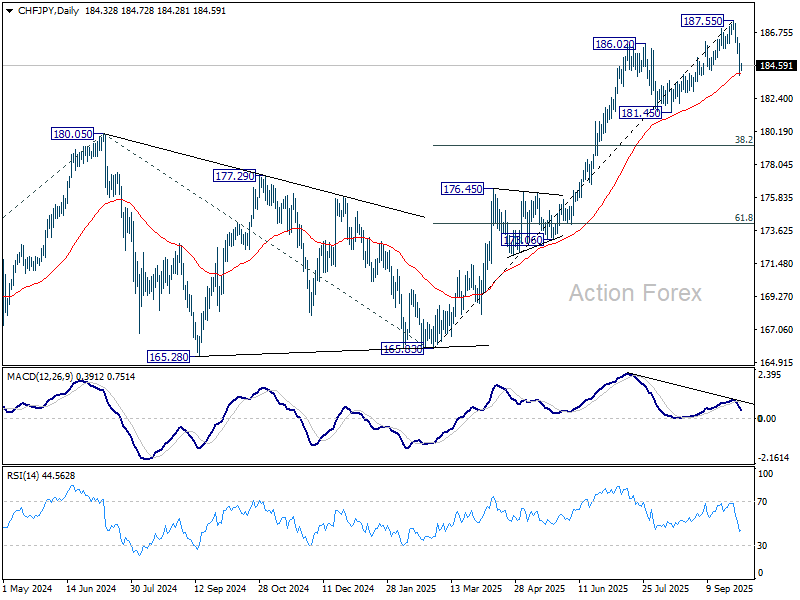

EUR/JPY, CHF/JPY pressing key EMA support, at risk of larger-scale corrections

The selloff in EUR/JPY and CHF/JPY has intensified since Monday, with both pairs now testing key moving averages. Sustained breaks here would strengthen the case that the cross rates have entered a larger-scale correction after months of relentless gains.

The latest push lower came after the pullback in US yields, triggered by disappointing ADP data overnight that showed private payrolls contracting for a second straight month. Markets took this as another sign of labor market weakness and quickly ramped up bets on Fed easing.

Futures now price in close to a 90% probability of two additional Fed cuts this year. US 10-year yield fell through near-term support at 4.110, suggesting the rebound from 3.992 had already peaked at 4.201, shy of 55 D EMA (now at 4.207).

The bigger moves in yield might only come when nonfarm payrolls are released to validate the bleak picture. Still, yields are likely to stay soft until then.

At the same time, expectations for BoJ tightening are gaining ground. Odds of an October 30 rate hike have risen to around 40%, reflecting growing conviction that policymakers may move sooner than previously expected.

That pivot was the recent hawkish rhetoric from policymakers. In particular, board member Asahi Noguchi, long viewed as a dove, said earlier this week that the need for policy tightening is “increasing more than ever.” His remarks were echoed by the Summary of Opinions from September’s meeting. And the resilient quarterly Tankan survey should have cleared some worries of doves regarding tariff impacts too.

Technically, considering bearish divergence condition in D MACD in EUR/JPY, sustained break of 55 D EMA (now at 172.20) should confirm medium term topping at 175.03, just ahead of 175.41 (2024 high). EUR/JPY should then be in corrective to the five-wave rally from 154.77. Deeper fall should be seen to 169.69 support, or even further to 38.2% retracement of 154.77 to 175.03 at 167.29.

Similarly for CHF/JPY, decisive break of 55 D EMA (now at 184.06) should confirm medium term topping at 187.55, on bearish divergence condition in D MACD. CHF/JPY should then be correcting whole five-wave rally from 165.83, and target 181.45 support, or further to 38.2% retracement of 165.83 to 187.55 at 179.25.

BoC sees weaker economy, eased inflation pressures in September cut

The BoC’s September summary showed policymakers debated whether to hold the policy rate at 2.75% or lower it by 25bps. In the end, members judged that the balance of risks had shifted enough to warrant a cut to 2.50%, citing weaker economic conditions and softer inflation pressures.

Council members noted three key developments since July that supported easing. First, the economy had weakened further, with signs of labor market softening. Second, recent inflation readings suggested that core price pressures were easing. Third, the removal of most retaliatory tariffs reduced the risk of renewed upside pressure on prices.

Against this backdrop, the Governing Council concluded that “inflationary pressures appeared more contained” and that a lower policy rate would better balance risks. They emphasized that uncertainty remains high, meaning decisions will continue to be guided by a “risk-management approach”. Policymakers agreed they would keep looking “over a shorter horizon than usual” and remain prepared to respond to new developments.

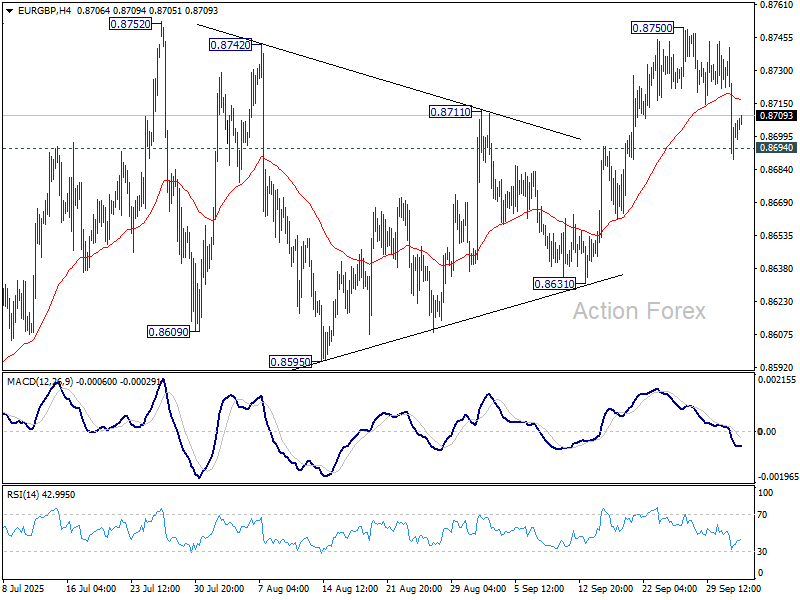

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8682; (P) 0.8712; (R1) 0.8734; More…

EUR/GBP recovered quickly after breaching 0.8694 support and intraday bias stays neutral first. On the upside, firm break of 0.8750 will resume larger rise to 0.8867 fibonacci level. However, decisive break of 0.8694 will turn bias back to the downside for 0.8631 support. Firm break there will indicate near term bearish reversal.

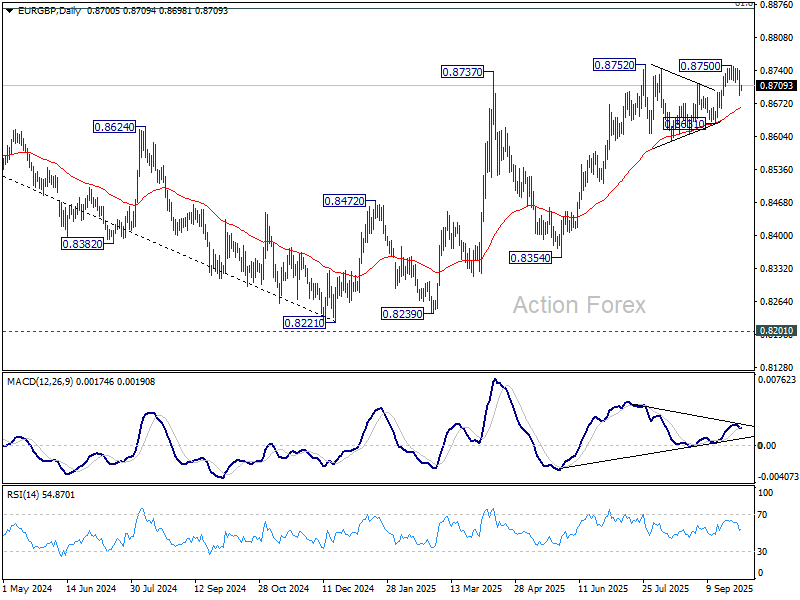

In the bigger picture, the structure from 0.8221 medium term bottom are not impulsive enough to suggest that it’s reversing the down trend from 0.9267 (2022 high). But even if it’s a correction, further rise could still be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867. Nevertheless, sustained trading below 55 W EMA (now at 0.8533) will argue that the pattern has completed and bring retest of 0.8221 low.

{kind=link}