{kind=link}

US stocks advanced solidly overnight after the Fed’s expected 25bps rate cut was greeted warmly by markets. Even though some economists labeled the decision a “hawkish cut,” the risk-on response in equities and the sell in Dollar suggested investors heard nothing hawkish enough to derail near-term sentiment.

The three-way vote split offered little surprise. Trump-backed Governor Stephen Miran once again pushed for a deeper 50bps reduction, while known hawks Austan Goolsbee and Jeffrey Schmid preferred to hold policy steady. The distribution fit comfortably with prior expectations and did little to shift the market narrative.

The Fed’s economic projections retained their key feature: one rate cut each in 2026 and 2027, reinforcing a shallow and deliberate easing path. Meanwhile, neither Chair Jerome Powell nor the statement signaled that the Committee is ready to commit to a pause. That ambiguity reflects both internal differences and the timing: November CPI and NFP—critical data points—are due next week, making it premature for Powell to any declare direction.

Market pricing barely budged. Fed fund futures now imply about a 48% chance of a 25bps cut in March, versus 52% for a hold—almost identical to pre-FOMC levels. With the market’s base case broadly intact and no hawkish surprise from Powell, the stock-market rally remains on track, keeping hopes for a Santa rally alive for now.

Attention now turns to the Swiss National Bank. SNB is expected to hold at 0.00%. Chair Schlegel has made clear that returning to negative rates would require a very high bar. Officials are expected to repeat their standard line: vigilant, but in no rush to move.

A positive development for Switzerland came with the confirmation on Wednesday that the US–Swiss tariff agreement will apply retroactively to November 14. The deal cuts Trump’s previously imposed 39% tariff down to a ceiling of 15%. The Swiss government noted this would reduce trade-weighted US tariff levels by roughly 10%, materially improving access for Swiss exporters.

In currency markets, Yen remains entrenched at the bottom of the weekly performance table. Aussie slipped to second-worst after today’s poor labor data reminded markets that RBA hike speculation for 2026 is still premature. Dollar sits as the third weakest following its post-FOMC slide.

At the top of the leaderboard, Swiss Franc has rebounded and is now the strongest performer—though recent weak Swiss CPI data raises the risk of a slight dovish tilt today, leaving CHF exposed. Euro follows as the second strongest, benefiting from Dollar weakness. Kiwi ranks third-best, supported by relative strength against the soft Aussie. Sterling and Loonie sit in the middle of the pack.

In Asia, Nikkei fell -0.90%. Hong Kong HSI is down -0.15%. China Shanghai SSE is down -0.92%. Singapore Strait Times is up 0.26%. Japan 10-year JGB yield fell -0.034 to 1.930. Overnight, DOW rose 1.05%. S&P 500 rose 0.67%. NASDAQ rose 0.33%. 10-year yield fell -0.022 to 4.164.

Australia jobs shock as employment drops -21.3k in November

Australia’s November labor data delivered a downside surprise, with employment falling by -21.3k against expectations for a 20k increase. The weakness was driven by a sharp -56.5k drop in full-time positions, partly offset by a 35.2k rise in part-time roles.

Despite the weaker headline, unemployment rate held at 4.3%, better than the expected uptick to 4.4%. The jobless rate has now been steady at 4.3% in five of the past six months, reflecting a labor market that is loosening but not deteriorating sharply. Participation rate dipped -0.2pts to 66.7%, suggesting some softening in labor-force engagement.

Monthly hours worked were unchanged on the month but still up 1.2% yoy, indicating modest resilience in total labor input despite weaker job creation.

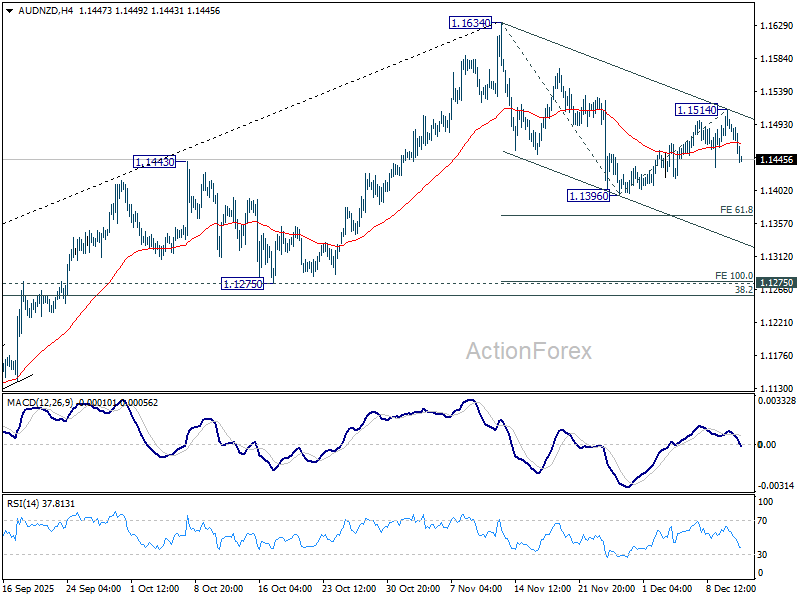

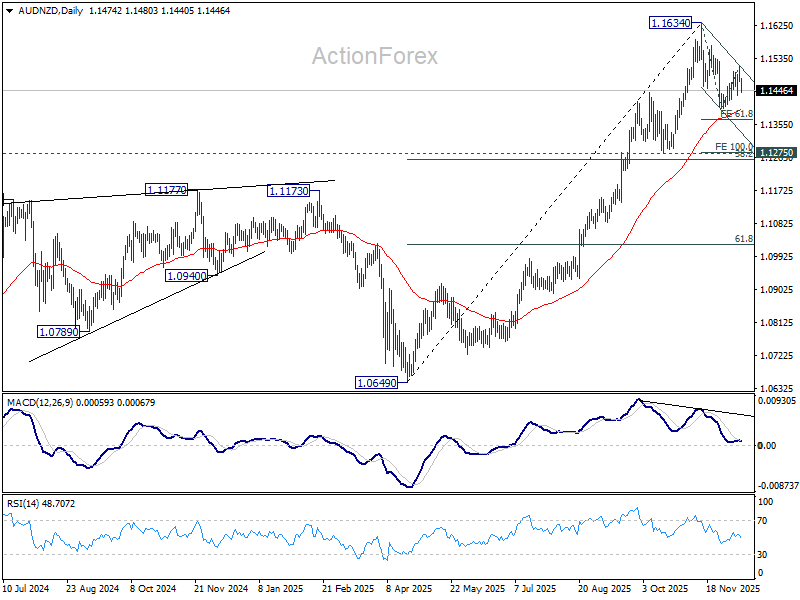

AUD/NZD to extend correction through 1.14 after data blow to RBA hike hopes

Australian Dollar weakened broadly after today’s significantly softer labor-market report, though it continues to show relative resilience against the U.S. Dollar and most majors—with the notable exception of Kiwi. The sharp downside surprise in employment has tilted sentiment in favor of further downside in AUD/NZD as markets reassess the likelihood of near-term RBA tightening.

Speculation of a 2026 RBA rate hike had intensified in recently, particularly after Governor Michele Bullock signaled that cuts were not on the horizon and that the Board had actively discussed scenarios in which rates might need to rise.

However, today’s -21.3k contraction in employment has sharply undercut that momentum. The data suggest that any discussion of a rate hike in the near term is premature. A long pause now appears the more plausible baseline—at least through Q1—while the RBA waits for a fuller run of data to determine whether underlying developments justify movement in either direction.

Technically, AUD/NZD is extending the corrective pattern from 1.1634. Today’s dip suggests the recovery from, as the second leg of the correction form 1.1634, might have completed at 1.1514 already. Deeper fall would be seen to 1.1396 first.

Break there will extend the fall to 61.8% projection of 1.1634 to 1.1396 from 1.1514 at 1.1367, and possibly further to 100% projection at 1.1267. But even in this case, downside should be contained by 1.1275 cluster support, which is slightly below 38.2% retracement of 1.0649 to 1.1634 at 1.1258.

The up trend from 1.0649 is expected to resume through 1.1634 at a later stage. But that will require renewed conviction that the RBA is genuinely preparing for a rate hike in 2026.

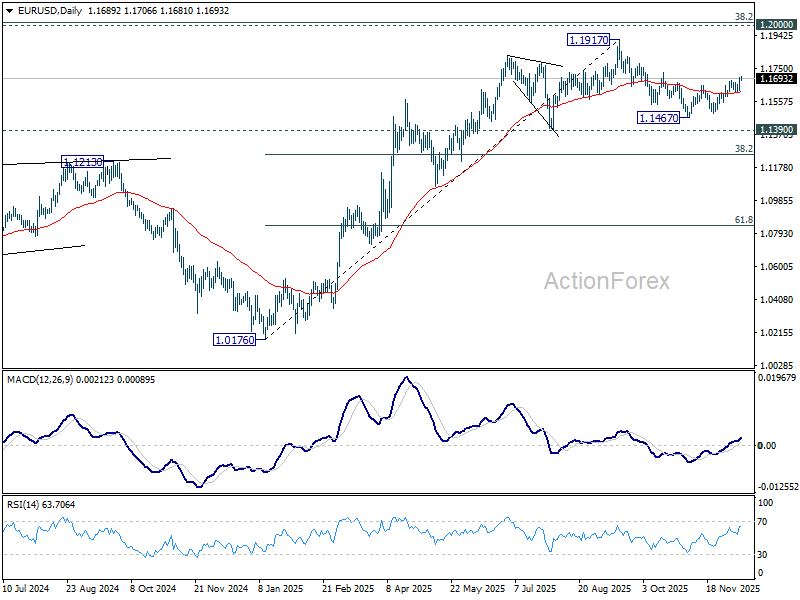

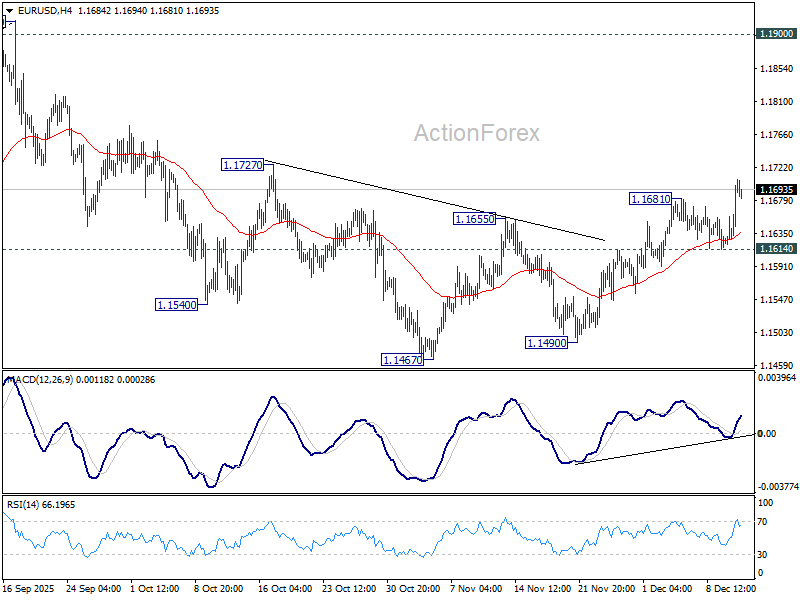

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1646; (P) 1.1673; (R1) 1.1724; More….

EUR/USD’s rise from 1.1467 resumed by breaking through 1.1681 temporary top and intraday bias is back on the upside. As noted before, corrective fall form 1.1917 should have completed at 1.1467. Firm break of 1.1727 resistance will solidify this case and bring retest of 1.1917 high. However, break of 1.1614 support will revive near term bearishness, and bring retest of 1.1467 low.

In the bigger picture, as long as 55 W EMA (now at 1.1346) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.