{kind=link}

Market sentiment has tilted mildly risk-off, though there is no sign of aggressive follow-through selling. Price action suggests caution rather than panic, with investors trimming exposure while waiting for clearer signals from both geopolitics and economic data.

Geopolitical developments continue to dominate headlines this week and look unlikely to fade quickly. The key question is whether there will be meaningful follow-up after the Venezuela episode. Attention has increasingly shifted toward Greenland, even if direct US military action there remains highly unlikely. Markets are watching diplomatic signals closely, particularly ahead of next week’s meeting between U.S. Secretary of State Marco Rubio and Denmark’s leadership to discuss Greenland.

For now, geopolitical risk is proving persistent but not disruptive enough to trigger classic safe-haven flows. Precious metals have failed to attract sustained demand, with Gold continuing to drift lower after briefly testing the 4500 level earlier in the week. Instead, defensive positioning has favored Dollar. Funds appear to be rotating back into USD, particularly from risk-sensitive currencies such as Aussie, Kiwi and Loonie.

That positioning, however, remains tentative ahead of Friday’s US non-farm payrolls report. Employment data so far have been solid in the sense that there is no evidence of a labor market breakdown. Weekly jobless claims released today and the rebound in ISM services employment both point to underlying resilience. Hiring momentum may be uneven, but the labor market is clearly not collapsing. The reaction function to NFP, however, is a key uncertainty. An upside surprise may not be uniformly negative for risk assets, especially if markets interpret strength as confirmation of a soft-landing scenario rather than renewed inflation risk.

Another looming catalyst is a forthcoming ruling by the US Supreme Court on President Donald Trump’s use of emergency tariff powers. A decision could come as early as Friday, with betting markets assigning roughly a 30% chance that the tariffs are upheld. Striking them down could dent government revenue expectations, lift Treasury yields and inject fresh volatility into the stock markets.

In FX performance today, Kiwi lags, followed by Aussie and Sterling. Swiss Franc Leads, ahead of Loonie and Yen. Dollar and Euro trade in the middle.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is down -0.20%. CAC is down -0.17%. UK 10-year yield is up 0.005 at 4.422. Germany 10-year yield is up 0.027 at 2.842. Earlier in Asia, Nikkei fell -1.63%. Hong Kong HSI fell -1.17%. China Shanghai SSE fell -0.07%. Singapore Strait Times fell -0.18%. Japan 10-year JGB yield fell -0.041 to 2.080.

US initial jobless claims rise to 208k vs exp 213k

US initial jobless claims rose 8k to 208k in the week ending January 3, below expectation of 213k. Four-week moving average of initial claims fell -7k to 212k, lowest since April 27, 2024. Continuing claims rose 56k to 1914k in the week ending December 27. Four-week moving average of continuing claims rose 21k to 1893k.

Eurozone PPI rises 0.5% mom in November, annual pressures stay weak at -1.7% yoy

Eurozone producer prices rose more than expected in November, with PPI increasing 0.5% mom, above forecasts of 0.2%. Despite the rebound, annual producer price inflation remained firmly negative at -1.7% yoy, versus expectation of -1.9% yoy.

The monthly increase was led by energy prices, which jumped 1.8% mom, while intermediate goods rose 0.3% and capital goods edged up 0.1%. Prices for durable consumer goods also increased 0.3%, partially offset by a -0.2% decline in non-durable consumer goods.

Across the EU, producer prices rose 0.6% mom and fell 1.3% yoy, with sharp divergence among member states. Ireland posted the strongest monthly gain at 4.4%, followed by (+4.4%), Sweden (+1.9%), Bulgaria and Greece (both +1.6%). Slovakia (-0.9%), Cyprus (-0.8%) and Spain (-0.5%).

Swiss CPI stays subdued at 0.1% as imported prices drag

Swiss inflation remained subdued in December, with headline CPI unchanged at 0.1% yoy, in line with expectations. Core inflation edged slightly higher, ticking up from 0.4% to 0.5%, pointing to mild underlying price pressures even as overall inflation stayed close to zero.

The divergence between domestic and imported prices remained a defining feature. Prices of domestic products rose from 0.4% to 0.5% yoy, while imported goods prices fell further into negative territory, slipping from -1.3% to -1.6% yoy.

On a monthly basis, headline and core CPI were flat mom, with domestic prices up 0.2% mom and imported prices down sharply by -0.8% mom. According to the State Secretariat for Economic Affairs, offsetting price movements kept the index stable. Lower prices for international package holidays, medicines and certain vegetables were balanced by higher costs for hotels, supplementary accommodation and private transport hire.

BoJ regional report sees small firms face constraints on wage hikes

Japan’s economy continues to recover gradually across the country, according to the latest Regional Economic Report from the BoJ. The central bank maintained its assessment for all nine regions, noting that activity is either picking up or recovering at a modest pace.

The report highlighted continued wage pressure, with many firms indicating the need to raise wages in fiscal 2026 at roughly the same pace as in 2025. Strong corporate profits and a tight labour market were cited as key drivers. That said, the BoJ flagged emerging divergence beneath the surface. Some regions warned that smaller firms may struggle to match last year’s wage hikes.

Some export-oriented areas reported softness linked to “the impact of U.S. tariffs and intensifying competition from Asian companies”. Others, however, pointed to “increasing global demand mainly for artificial intelligence-related goods.”

Japan real wages fall -2.8% in November, sharpest in nearly a year

Japan’s real wages fell sharply in November, dropping -2.8% yoy, marking the 11th consecutive month of decline and the steepest fall since last January. Inflation-adjusted earnings were hit as a 3.3% rise in consumer prices more than offset a modest increase in nominal pay.

Nominal wages rose just 0.5% yoy, far below expectations of 2.3% and a sharp slowdown from October’s 2.5% pace. While nominal pay has now risen for 47 straight months, the latest reading marks the weakest growth since December 2021.

The softness was driven largely by a -17.0% drop in special earnings, mainly volatile one-off bonuses outside the usual summer and winter payment periods. More concerning for the underlying trend, regular pay growth eased from 2.4% yoy to 2.0%. Overtime pay slowed from 2.1% to 1.2%, pointing to waning momentum in private-sector income growth and continued pressure on household purchasing power.

RBA’s Hauser shrugs off CPI miss, says rate cuts still unlikely

The RBA remains biased against further near-term rate cuts, despite the softer-than-expected inflation data, according to comments from Deputy Governor Andrew Hauser. Speaking in an interview with Australian Broadcasting Corporation, Hauser said the likelihood of additional easing in the near term remains “probably very low”.

Hauser stressed that the November CPI downside surprise has not altered the central bank’s thinking. He described the data as “helpful” but said it was “largely as we expected,” adding that there was “not a lot of news” in the release from a policy perspective. Inflation remains above the RBA’s 2–3% target range, reinforcing the case for caution.

He also noted that part of the moderation in inflation reflected temporary factors such as Black Friday discounting, while cost pressures in housing-related components actually picked up. As a result, policymakers are placing greater emphasis on the upcoming quarterly inflation report due later this month.

Hauser said the RBA will assess that quarterly data in the context of the broader economy rather than reacting mechanically to a single number. While an extreme outcome would prompt deeper scrutiny, he made clear there is no simple rule linking specific inflation prints to policy move.

“We don’t have a rule that says if it’s 0.9 we hold, and if it’s 1 we raise and if it’s 0.7 we cut — we take a view of the whole economy,” Hauser emphasized.

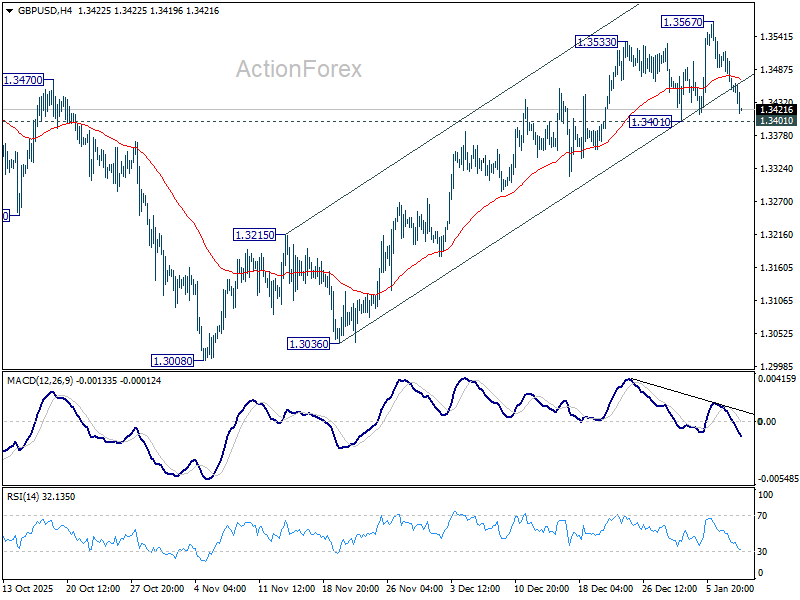

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3436; (P) 1.3477; (R1) 1.3497; More…

Intraday bias in GBP/USD remains neutral for the moment. Further rally is in favor with 1.3401 support intact. On the upside, break of 1.3567 will resume the rise from 1.3008 to retest 1.3787 high. However, firm break of 1.3401 will confirm short term topping, and bring deeper fall back to 55 D EMA (now at 1.3365) and possibly below. Sustained break of 55 D EMA will argue that corrective pattern from 1.3787 is already extending with another falling leg, and target 1.3008.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.