{kind=link}

Market sentiment appears to be stabilizing after this week’s sharp tech-led selloff. US equity futures are edging higher and cryptocurrencies are recovering modestly, suggesting the worst of the near-term liquidation pressure may have passed, at least for now. The calmer tone is feeding through into FX markets, where activity has slowed markedly. Most major pairs and crosses remain trapped within yesterday’s ranges, reflecting a lack of fresh catalysts and a market reluctant to re-extend positions after recent volatility.

Canadian Dollar is one of the mild outperformers, lifting slightly after mixed domestic labor data. While headline employment disappointed, the sharp fall in the unemployment rate and a marginal slowdown in wage growth were enough to ease concerns about deep deterioration. From a policy perspective, the data did little to shift expectations for the BoC, which is still widely seen as in a prolonged hold.

Sterling also found modest support following comments from BoE Chief Economist Huw Pill. Pill warned against complacency around the expected dip in inflation, stressing that much of the near-term downside reflects temporary fiscal measures rather than a clean break in underlying price pressures. Those remarks served as a reminder that policy easing is far from guaranteed. Although markets leans toward a rate cut in March after yesterday’s dovish-leaning hold, the deep split within the MPC means incoming data still matter significantly.

For the week so far, Aussie is now the strongest performer, followed by Dollar and then Kiwi. Yen sits at the bottom of the table, followed by Sterling and Swiss Franc, while Euro and Loonie are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.11%. DAX is up 0.38%. CAC is down -0.06%. UK 10-year yield is down -0.04 at 4.523. Germany 10-year yield is down -0.012 at 2.836. Earlier in Asia, Nikkei rose 0.81%. Hong Kong HSI fell -1.21%. China Shanghai SSE fell -0.25%. Singapore Strait Times fell -0.83%. Japan 10-year JGB yield rose 0.006 to 2.234.

Canada employment falls -25k, participation drop drives unemployment rate down to 6.5%

Employment in Canada fell by -25k in January, a sharp miss versus expectations for a modest 7k gain and a clear sign of near-term labor market softness. The decline was driven by a steep drop in part-time jobs (-70k), which more than offset gains in full-time employment (45k).

Meanwhile, Headline unemployment fell sharply from 6.8% to 6.5%, beating expectations of 6.8%, and marking its lowest level since September 2024. However, the improvement was driven by a sizeable drop in labor force participation rather than stronger hiring, with the participation rate falling 0.4ppt to 65.0%. Employment rate slipped from 60.9%. to 60.8%, its first decline since August.

Wage pressures continued to ease at the margin. Average hourly wages rose 3.3% yoy, down slightly from December’s 3.4% yoy.

BoE’s Pill urges to look past April inflation dip

BoE Chief Economist Huw Pill cautioned against drawing “too much comfort” from the near-term dip in inflation expected later this year. Speaking at an event today, Pill said the downside in short-term inflation dynamics was partly created by “fiscal measures” announced last November and risks obscuring the more persistent forces shaping longer-term price pressures.

Drawing a parallel with 2025, Pill said the Bank of England had previously looked through a temporary inflation spike caused by regulatory changes, and should apply the same logic to the projected drop to 2% in April when lower regulated energy prices take effect.

He stressed that monetary policy must remain focused on addressing persistence in inflationary pressures beyond these temporary effects. Pill was among the narrow 5–4 majority on the MPC who voted to keep Bank Rate unchanged at 3.75% this week.

BoE survey sees gradual rate cuts, higher gilt yields ahead

According to the BoE’s latest Market Participants Survey, investors expect a steady easing cycle over the next year. Respondents see Bank Rate gradually reduced from the current 3.75% to around 3.0% by the March 2027 meeting, pointing to confidence that disinflation will allow policy to ease without urgency.

Despite expectations for lower rates, views on quantitative tightening were unchanged. The median forecast for gilt sales over the 12 months from October remained at GBP 50 billion.

At the same time, participants revised up their outlook for long-term yields. The median expectation for 10-year gilt yields at end-2026 rose to 4.25%, from 4.0% previously, indicating that while policy rates are expected to fall, investors see structural or fiscal factors keeping longer-dated yields elevated.

ECB’s Kazaks: Current Euro l baked in, but further sharp appreciation could trigger response

Latvian ECB Governing Council member Martins Kazaks said a “sizeable and pacey” strengthening of Euro could materially lower the inflation outlook, “potentially triggering a policy response”. A stronger currency, he argued in a blog post, would weigh on competitiveness and economic activity, feeding through to weaker price pressures.

Kazaks noted that EUR/USD has traded in a relatively narrow 1.15–1.20 range in recent months. The last meaningful appreciation occurred in the second quarter of 2025, a move he described as appearing largely “permanent”.

Because of policy lags, the full disinflationary impact of that earlier appreciation has yet to be felt and is expected to emerge later this spring. Importantly, Kazaks stressed that these effects are already “baked into” the ECB’s baseline forecast, limiting the need for near-term policy adjustment.

With that backdrop, Kazaks said monetary policy is “in a good place” and not the main lever at present. Instead, he argued that urgent progress on structural reforms is needed to strengthen Europe’s economic fundamentals, resilience, and global standing in an increasingly volatile geopolitical environment.

BoJ’s Masu backs further hikes, flags weak Yen risks but urges caution

BoJ board member Kazuyuki Masu said further interest rate hikes will be needed to complete Japan’s monetary policy normalization. He noted that underlying inflation remains below 2% but is “drawing very close” to that level as firms and households gradually shed entrenched deflationary behavior.

He cautioned, however, that the Yen’s recent weakness could amplify price pressures by lifting inflation expectations, with potential spillovers into underlying inflation. Also, He highlighted processed food prices as a key area to watch, noting that surging rice prices may have made consumers more receptive to broader food price increases.

At the same time, Masu stressed the need for caution. “it is critical to ensure excessive rate hikes do not disrupt the virtuous cycle of a moderate rise in prices and wages that has finally begun to gain momentum in Japan,” he said.

RBA’s Bullock defends rate hike, cites excess demand and capacity strain

RBA Governor Michele Bullock told the House of Representatives economics committee today that the decision to raise the cash rate by 25bps to 3.85% was driven by a clear resurgence in inflation pressures during the second half of 2025.

Bullock said the Board concluded that demand in the economy had proven stronger than expected, running ahead of the supply side’s capacity to respond. As a result, inflation outcomes indicated a larger degree of “excess demand” than previously assumed.

She emphasized that this imbalance means demand growth must be dampened unless productivity and supply expand at a faster pace. With the economy now judged to be “more capacity constrained”, leaving policy unchanged would risk inflation remaining elevated for longer. On that basis, the RBA determined that tighter monetary policy was required.

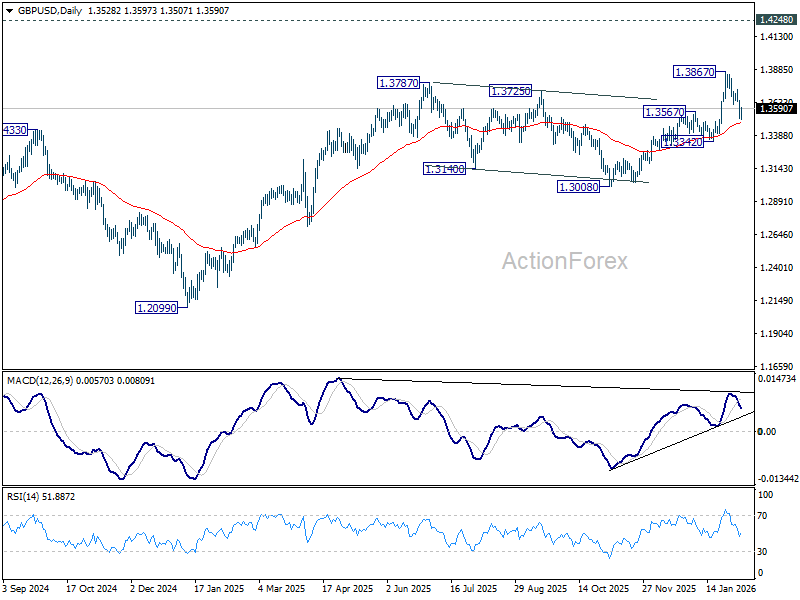

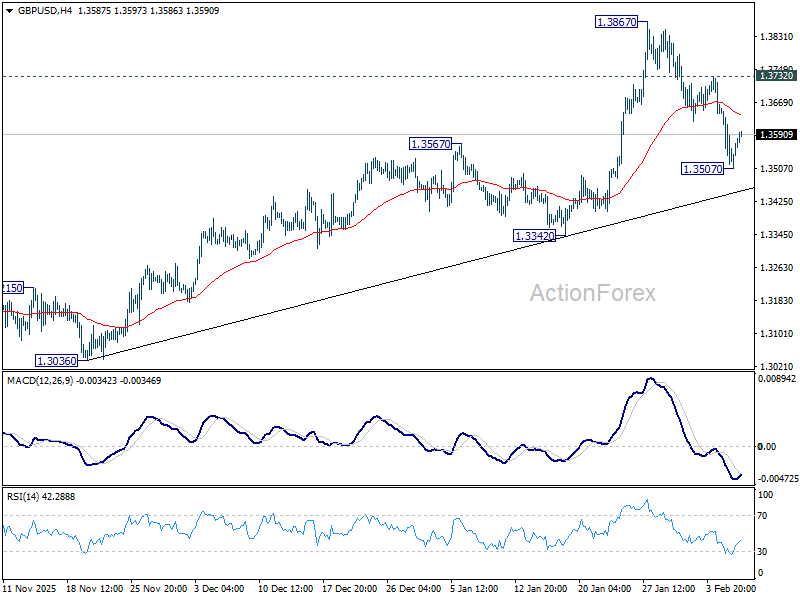

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3472; (P) 1.3575; (R1) 1.3631; More…

GBP/USD recovered after dipping to 1.3507 and intraday bias it turned neutral again. On the downside, below 1.3507 will resume the fall from 1.3867 to 55 D EMA (now at 1.3483). Sustained break there will raise the chance of larger scale correction, and target 1.3342 support for confirmation. On the upside, above 1.3732 minor resistance will bring retest of 1.3867. Firm break there will resume larger up trend towards 1.4284 key resistance.

In the bigger picture, rise from 1.0351 (2022 low) is resuming by breaking through 1.3787 high. Further rally should be seen to 1.4284 key resistance (2021 high). Decisive break there will add to the case of long term bullish trend reversal. For now, outlook will stay bullish as long as 1.3008 support holds, even in case of deep pullback.