{kind=link}

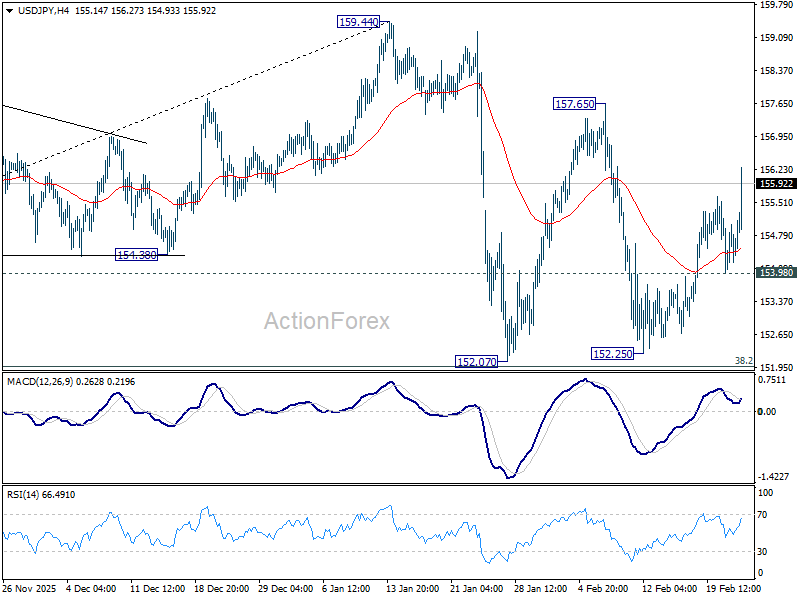

Yen came under marked pressure in otherwise subdued trading, with the move driven less by global risk appetite and more by domestic political developments. The catalyst was a reported shift in tone from Prime Minister Sanae Takaichi, who is said to have voiced direct opposition to further rate hikes in discussions with BoJ Governor Kazuo Ueda.

The signal triggered a repricing in rate expectations. Markets that had leaned toward an April move from the BoJ are now pushing that timeline back toward June at the earliest. The adjustment was enough to send USD/JPY higher and weigh broadly on Yen crosses. The political angle matters. If Tokyo is signaling reluctance to tighten further, the BoJ’s path toward normalization becomes more constrained. That tension between monetary independence and political priorities is now being reflected in FX markets.

At the same time, Aussie is also softer as traders position ahead of January’s Monthly CPI Indicator due tomorrow. Although senior officials at the RBA continue to emphasize quarterly data, the monthly print remains a key guide for near-term rate expectations.

Consensus sees headline CPI easing to 3.7% from 3.8% in December. However, the “danger zone” lies in a repeat or upside surprise. A reading of 3.8% or higher would suggest that the RBA’s recent hike to 3.85% may not have been sufficient to curb underlying pressures. Even more important will be the trimmed mean measure, which stood at 3.3% previously. Any upward move in core inflation would significantly raise the probability of another hike in May, reversing today’s AUD weakness.

Meanwhile, Dollar is mildly firmer as markets look ahead to US President Donald Trump’s State of the Union address. While the speech is expected to be wide-ranging, traders will focus on any references to tariff policy and tensions with Iran.

On a weekly basis, Swiss Franc leads performance, followed by Sterling and Dollar. Aussie sits at the bottom, trailed by Yen and Kiwi, while Euro and Loonie trade in the middle of the pack.

Fed’s Bostic: Lean into structural change, not rate cuts

Outgoing Atlanta Fed President Raphael Bostic told said the rapid adoption of artificial intelligence may push the US into a period of structurally higher unemployment. In an interview with Reuters, he suggested that firms may simply need fewer workers, raising the level of joblessness considered consistent with full employment.

Rather than attempting to artificially suppress unemployment with rate cuts, Bostic argued policymakers should recognize structural shifts and set rates accordingly. “This is a very hard time to be a central banker,” he said, noting that the same economic indicators may now carry different implications as technological change reshapes the labor market.

With inflation still above target, Bostic warned that easing policy to counter structural forces could lead to both higher inflation and misaligned employment signals. “To address short-run issues that are structural in nature could put us at risk of a much more difficult situation, where both of our mandate measures seem to be moving in the wrong direction,” Bostic said.

He steps down as president of the Federal Reserve Bank of Atlanta at the end of his term on February 28.

Takaichi caps rate hopes, USD/JPY jumps; Is intervention at next?

Yen tumbled broadly after reports that Japanese Prime Minister Sanae Takaichi expressed reluctance to raise interest rates further during her February 16 meeting with BoJ Governor Kazuo Ueda. The report, carried by Mainichi Shimbun and citing multiple unnamed sources, suggested a firmer stance against tightening than previously seen.

According to the report, Takaichi emphasized that monetary policy must not “extinguish the fire” of economic recovery supported by her administration’s stimulus measures. Her position was described as stricter than at the prior November 2025 meeting.

The BoJ is widely viewed as recognizing the need for further tightening to normalize the financial system and address persistent Yen weakness. Yet with Takaichi strengthened politically after a landslide lower house victory, the balance between monetary independence and political priorities is under scrutiny.

The timing of the leak is notable. With Japan’s annual Shunto wage negotiations due in March, markets have been pricing a high probability of the next rate hike in Q2, particularly April. The deliberate nature of the Mainichi report suggests an attempt by the administration to cap rate expectations ahead of wage outcomes.

March has already been seen as too early for a move, as policymakers would prefer to assess wage negotiation results first. But if Takaichi’s reluctance proves durable, June may become the more realistic window for any additional tightening.

This creates an inherent policy tension. Takaichi seeks to avoid choking off recovery through higher rates, yet Japan also faces pressure from a weakening Yen. Balancing lower borrowing costs with currency stability presents a narrowing path.

Some analysts speculate that if rate hikes are delayed, authorities may lean more heavily on FX intervention should USD/JPY approach the 160 level, the line in the sand for Takaichi.

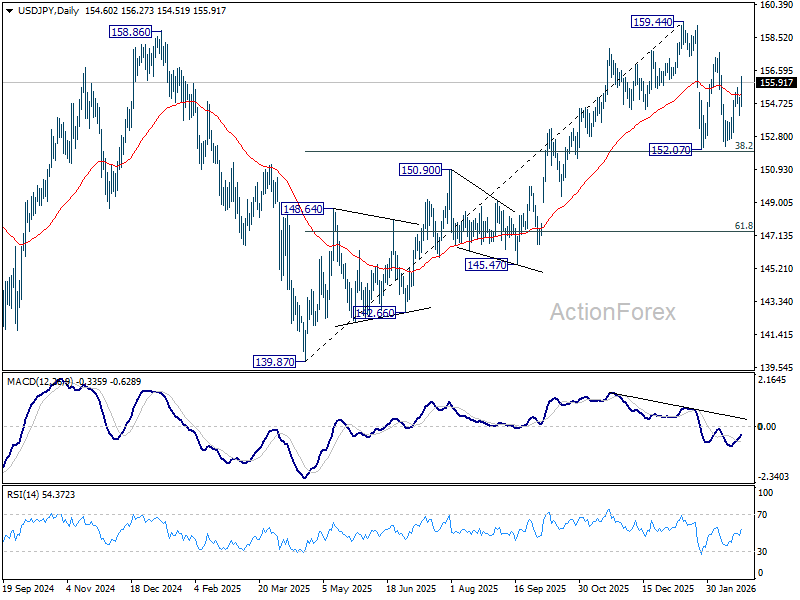

Technically, USD/JPY’s sharp jump reinforces the view that recent price action from 159.44 represents a near term sideway consolidation pattern only. The broader uptrend from the 139.87 low in 2025 remains intact, suggesting eventual resumption toward and potentially beyond 159.44 . But then risk of intervention will surge as USD/JPY marches on.

RBA stays focused on quarterly trimmed mean during CPI transition

In a speech today, Michael Plumb, head of economic analysis at the RBA, said the central bank welcomes the introduction of a complete monthly CPI, noting that more frequent and comprehensive data will materially improve the timeliness of its inflation assessment.

However, Plumb cautioned that it will “take us some” time to understand the properties and seasonal patterns of the new monthly series. During the transition, the RBA will continue to “focus on the quarterly data”, particularly the quarterly trimmed mean measure, for forecasting and evaluating underlying inflationary pressures.

While maintaining its quarterly focus, the RBA has begun analyzing underlying inflation measures constructed from monthly data. Plumb said policymakers will assess potential biases, seasonal differences, responsiveness to economic conditions, and usefulness as a leading indicator.

The central bank intends to engage widely and communicate transparently before any shift in preferred measures in what he described as a gradual move toward a “post-quarterly CPI world.”

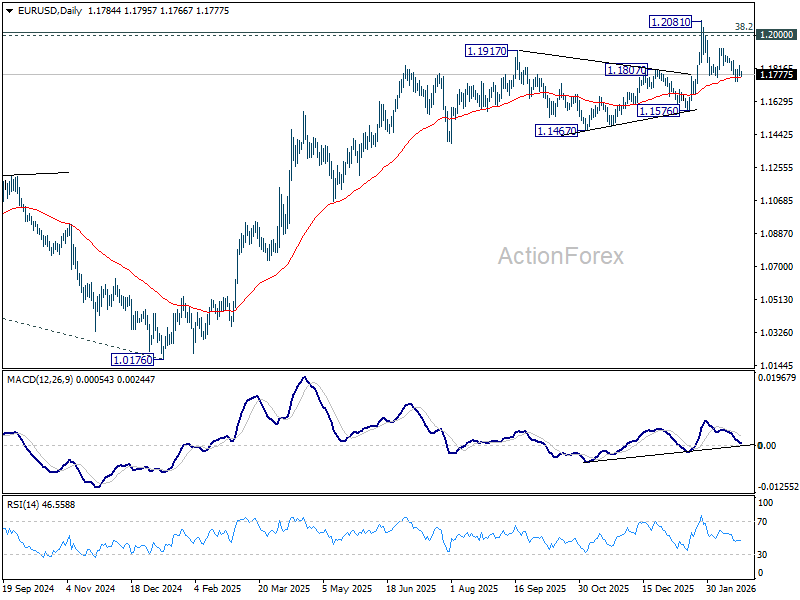

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1762; (P) 1.1798; (R1) 1.1822; More….

EUR/USD is staying in consolidations above 1.1740 and intraday bias remains neutral. Near term risk will remain on the downside as long as 1.1928 resistance holds. Below 1.1740 temporary low will target 1.1576 support next. Firm break there should confirm rejection by 1.2 key psychological level and turn near term outlook bearish. However, break of 1.1928 argue that fall from 1.2081 has completed as a correction, and revive near term bullishness. Retest of 1.2081 should then be seen next.

In the bigger picture, as long as 55 W EMA (now at 1.1494) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will add to the case of long term bullish trend reversal. Next medium term target will be 138.2% projection of 0.9534 to 1.1274 from 1.0176 at 1.2581. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.