Dollar edged higher today as fresh Iranian strikes on UAE energy infrastructure revived concerns over global oil supply, tempering the cautious optimism seen earlier in the week. While the move has not triggered a full risk-off shift, markets are clearly reassessing the durability of the recent stabilization in energy prices.

Oil benchmarks reversed from Monday’s pullback as the geopolitical risk premium returned. The renewed escalation, including drone and missile attacks on critical infrastructure, has reinforced the view that supply disruptions are not only persistent but potentially worsening. Traders are once again pricing in a more prolonged energy shock.

The broader conflict continues to intensify. Iran launched further missile strikes on Israel overnight, demonstrating its sustained long-range capabilities despite weeks of military pressure. In response, Israel expanded operations targeting infrastructure in Tehran and Hezbollah-linked sites in Beirut, signaling that the conflict is remains in an entrenched phase.

The situation in the Strait of Hormuz remains a central concern. The key shipping corridor is still effectively paralyzed, with roughly 20% of global oil supply hindered. While isolated vessels are attempting transit, most shippers are avoiding the route, forcing Gulf producers to rely on alternative pipeline exports that are insufficient to fully replace lost volumes.

This constraint is increasingly visible in market pricing. The Brent–WTI spread has widened back above its typical $2–$5 range. A sustained break above $10 would signal a shift from general market anxiety to concerns over physical supply shortages, marking a more dangerous phase of the energy shock.

Despite these developments, market reaction remains measured. Equities have not seen broad liquidation, and FX moves suggest caution rather than panic. This reflects lingering hopes that supply disruptions can still be partially managed, as well as expectations that coordinated reserve releases may help stabilize markets in the near term.

In currency markets, Dollar is the strongest performer of the day so far, supported by its safe-haven appeal and the renewed rise in yields tied to energy-driven inflation risks. However, gains have been modest, reinforcing the view that markets are not yet pricing in a worst-case scenario.

Australian Dollar is the second-best performer, benefiting from the RBA’s reaffirmed tightening bias despite the split vote. Canadian Dollar is also firm, supported by higher oil prices, though domestic weakness continue to cap its upside.

On the weaker side, New Zealand Dollar is under pressure, particularly against the Aussie, while Sterling and Euro also lag. The Swiss Franc and Yen are trading in the middle of the pack, suggesting that traditional safe havens are not attracting the same flows as Dollar in the current environment.

Looking ahead, markets remain highly sensitive to further developments in the Middle East. The key question is whether the current disruption remains contained or escalates into a broader supply shock. For now, the return of the oil risk premium is enough to keep Dollar supported, but a decisive break in energy markets—particularly via the Brent–WTI spread—would be needed to trigger a more pronounced global risk-off move.

In Asia, Nikkei fell -0.09%. Hong Kong HSI is up 0.20%. China Shanghai SSE is down -0.66%. Singapore Strait Times is up 1.02%. Japan 10-year JGB yield is down -0.003 at 2.227. Overnight, DOW rose 0.83%. S&P 500 rose 1.01%. NASDAQ rose 1.22%. 10-year yield fell -0.065 to 4.220.

RBA rate hike to 4.10% lacks conviction as board splits 5–4

RBA raised the cash rate to 4.10%, but the narrow 5–4 vote revealed a divided board and limited conviction behind the move. While policymakers cited rising fuel costs and inflation risks, the split highlights growing uncertainty over the outlook as energy shocks threaten both inflation and growth. Read more.

RBA united on further tightening despite split vote, Bullock says

RBA Governor Michele Bullock said the board remains united on further tightening despite the 5–4 split, with disagreement centered on timing rather than direction. She emphasized that inflation remains too high and driven by excess demand, while warning that policy may need to stay restrictive to prevent more persistent price pressures. Read more.

AUD/NZD breaks higher on RBA boost, targets 1.2467 as uptrend accelerates

AUD/NZD surged after breaking above 1.2118 as Bullock’s clarification reinforced RBA’s tightening bias. The breakout suggests upside acceleration, with focus on the 1.2467 target while 1.1867 support holds. Read more.

Bitcoin rebounds above 75k on short squeeze, 80–85k zone to cap upside

Bitcoin climbed back above 75k as a short squeeze drove a sharp rebound after sellers failed to push prices toward 60k earlier this month. Momentum has improved with a break above the 55-day EMA, but gains may be capped in the 80–85k resistance zone. A break below 70k would signal the recovery has run its course. Read more.

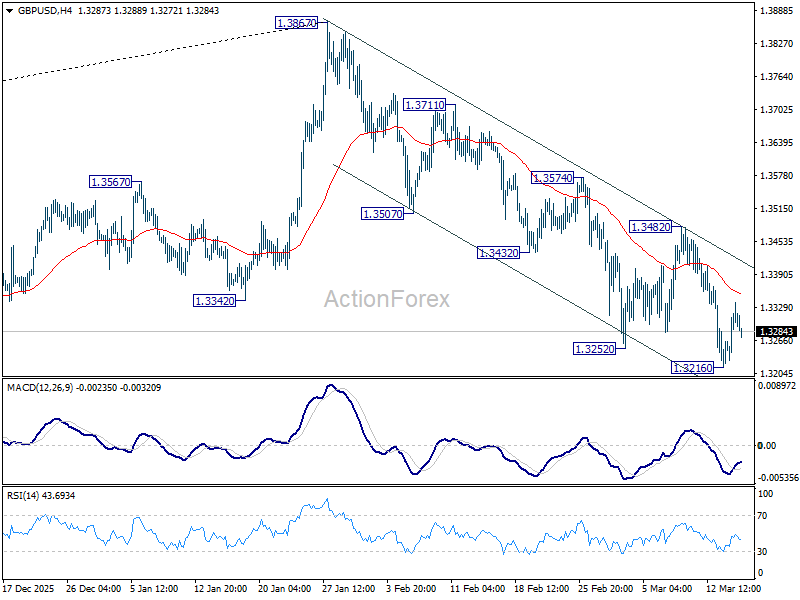

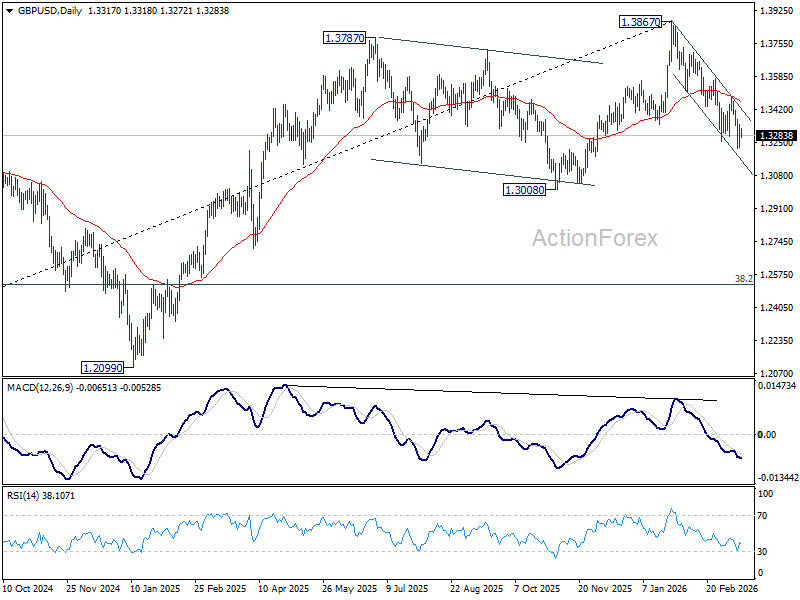

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3249; (P) 1.3295; (R1) 1.3365; More…

GBP/USD dips mildly as recovery from 1.3216 lost momentum, but holds well above this support. Intraday bias stays neutral and more consolidations could be seen. Risk will stay on the downside as long as 1.3482 resistance holds. Below 1.3216 will resume the fall from 1.3867 to 1.3008 structural support. Firm break there will carry larger bearish implication and target 1.2524 fibonacci level.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place from 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or under further development.

{kind=link}