A sharp rise in US CPI is all but certain, with March inflation expected to accelerate from 2.4% yoy to 3.4% yoy on the back of a oil-driven energy shock. But markets are already looking beyond the headline number today. The key question is whether the surge spills into core inflation through second-round effects swiftly and pushes inflation expectations higher. That combination—not the CPI spike itself—will determine whether the Fed sticks to a “look-through” stance by delays its easing cycle further, not cancelling.

Headline inflation is expected to jump sharply, with a 1.0% mom increase largely driven by gasoline prices, which some estimates suggest surged nearly 20% during the month. Core CPI is also seen firming from 2.5% yoy to 2.7% yoy, with a 0.3% mom rise. While the headline spike will grab attention, it is widely understood to be energy-driven.

This distinction matters because the Fed has historically treated energy shocks as exogenous. Monetary policy cannot offset supply disruptions such as a closed Strait of Hormuz, and policymakers have often chosen to look through such volatility unless it feeds into broader inflation dynamics.

That is why the focus shifts immediately to second-round effects. The key issue is how quickly higher energy costs transmit into transportation services, including airfares and shipping, and into food prices. A faster and broader pass-through would signal that inflation is becoming more persistent.

Core CPI is therefore the first test. If underlying inflation trends closer to 3%, it would suggest that second-round effects are already taking hold. That would challenge the Fed’s assumption that the current shock is temporary.

The second, and arguably more important, test comes from inflation expectations. The University of Michigan survey will provide a timely read on whether households see the current price surge as temporary or lasting.

In March, one-year inflation expectations already jumped from 3.4% to 3.8%, marking the largest increase in nearly a year. This rise reflected growing sensitivity to gasoline prices and near-term cost pressures. However, five-year inflation expectations edged down slightly to 3.2%, providing reassurance that long-term inflation credibility remained intact.

That balance could now be tested. A move in one-year expectations above 4%, coupled with a rise in five-year expectations toward 3.5%, would signal that inflation psychology is shifting more broadly. Such a development would likely unsettle the Fed.

For now, markets still lean toward the view that this inflation shock is temporary. If the US-Iran ceasefire holds and oil prices fall back toward $80, the Fed would have both the “economic and political cover” to treat March CPI as an outlier. Under that scenario, the broader disinflation trend would resume later in the year, and rate cuts would be delayed rather than cancelled. The policy path would shift in timing, not direction.

However, all of this ultimately hinges on geopolitics. Developments from the Islamabad talks will determine whether the energy shock fades or intensifies. In that sense, CPI may dominate today’s data calendar, but the real driver of inflation—and Fed policy—lies in whether the conflict moves toward resolution or escalation.

In the currency markets, Dollar remains the worst for the week so far, followed by Yen, and then Loonie. Kiwi is sitting on the top, followed by Aussie, and then Sterling. Euro and Swiss Franc are positioning in the middle.

In Asia, at the time of writing, Nikkei is up 1.95%. Hong Kong HSI is up 0.58%. China Shanghai SSE is up 0.63%. Singapore Strait Times is up 0.09%. Japan 10-year JGB yield is up 0.029 at 2.426. Overnight, DOW rose 0.58%. S&P 500 rose 0.62%. NASDAQ rose 0.83%. 10-year yield rose 0.002 to 4.293.

BoJ’s Himino Sees No Stagflation Yet, Warns of Oil-Driven Policy Dilemma

BoJ Deputy Governor Ryozo Himino said Japan is not facing stagflation for now, with inflation near target and growth still holding up. But he warned that a prolonged Middle East conflict could change that dynamic—pushing inflation higher while dragging on growth and creating a difficult policy trade-off. Read More.

Japan PPI Accelerates to 2.6% in March as Import Costs Surge 7.9%

Japan’s producer prices picked up more than expected in March, driven by a sharp rise in import costs and higher energy and industrial input prices. The surge in import prices points to renewed upstream inflation pressure, raising the risk that cost increases could feed through more broadly into the economy. Read More.

China PPI Turns Positive for First Time Since 2022 as CPI Softens

China’s factory prices returned to growth for the first time since 2022, driven by rising energy and commodity costs. But consumer inflation is losing momentum, with CPI and core prices slowing sharply—highlighting a growing gap between upstream cost pressures and weak domestic demand. Read More.

NZ BNZ Manufacturing Falls to 53.2, Slower Expansion as War Concerns Weigh on Sentiment

New Zealand’s manufacturing sector is still expanding, but momentum is clearly slowing. PMI eased in March as production and new orders softened, while inventories rose—hinting at cooling demand. Read More.

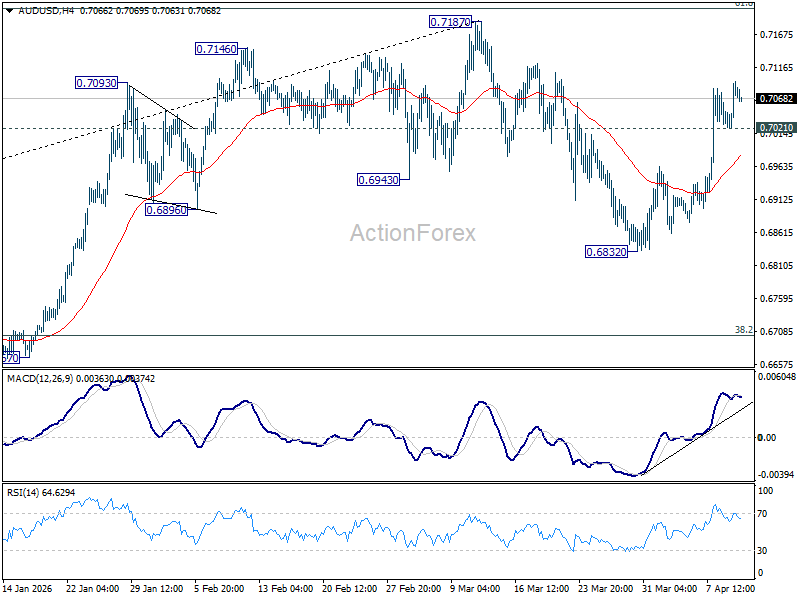

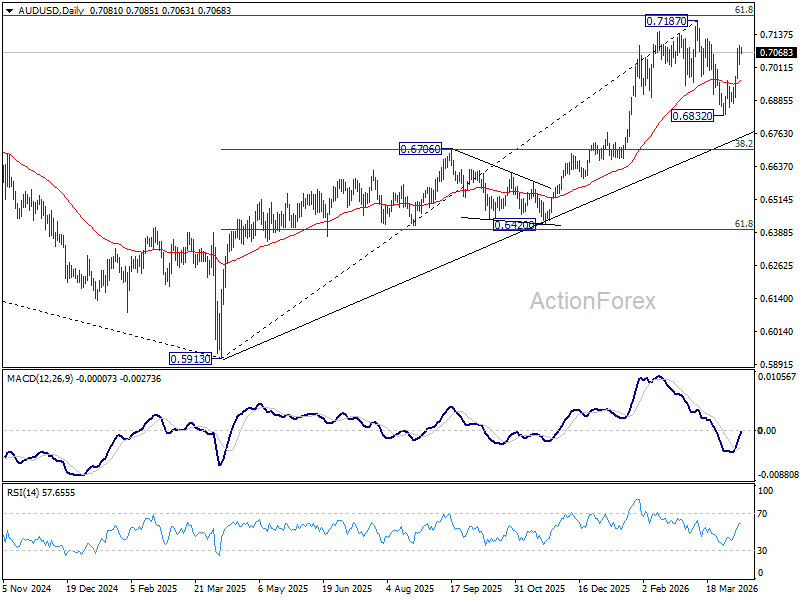

AUD/USD Daily Report

Daily Pivots: (S1) 0.7039; (P) 0.7068; (R1) 0.7113; More…

Intraday bias in AUD/USD remains mildly on the upside as rise from 0.6832 is in progress to retest 0.7187 high. Strong resistance could be seen there to bring another fall to extend the near term corrective pattern. On the downside, below 0.7021 minor support will turn intraday bias neutral again first.

In the bigger picture, as long as 0.6706 cluster support holds, rise from 0.5913 (2024 low) should still be in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it’s already reversing the down trend from 0.8006 (2021 high). However, firm break of 0.6706 will dampen this bullish case, and bring deeper fall back to 0.6420 support, and possibly below.

{kind=link}