Semiconductor selloff has evolved from a regional correction into a broader test of confidence in AI investment cycle. South Korea appears to have delivered first warning earlier this month, when semiconductor-heavy KOSPI broke below its 55 D EMA. Selling then spread through US chipmakers on Thursday before accelerating across Japan and Taiwan on Friday. Nikkei slumped -4%, led by a -16% plunge in Kioxia, -9% fall in Murata and -3.8% decline in TDK, while NASDAQ futures dropped more than -2% during European morning. Focus now shifts back to Wall Street and whether weakness completes a full circuit from Asia to US.

Price action in TSMC offered clearest evidence that investor psychology toward AI trade is changing. Company reported a 77% annual earnings increase and raised its 2026 capital expenditure guidance from USD 52-56B to USD 60-64B. Yet its shares still fell more than -7% in Taiwan today. Strong earnings and greater AI investment would previously have been enough to lift semiconductor valuations. Latest reaction suggests investors are not prepared to reward spending alone and are instead demanding clearer evidence that record capital expenditure will generate corresponding profit and productivity gains.

Alphabet’s delay of flagship Gemini 3.5 Pro model provided an important trigger for renewed anxiety. Delay revived questions over pace of AI commercialization and whether returns from infrastructure spending will arrive quickly enough to justify valuations already embedded across chip sector. Those concerns echoed Thursday’s US session, when SanDisk fell more than -12% and Micron, AMD and Broadcom each dropped around -5%, even as NASDAQ declined a comparatively smaller -1.47%. South Korea was closed for a holiday on Friday, but its earlier decline increasingly looks like beginning of a broader reassessment that has now spread through Japan and Taiwan.

Geopolitical developments are compounding pressure at particularly vulnerable moment. Iran conflict has widened further, with fresh strikes reported across Jordan, Bahrain and Kuwait. An unconfirmed report that Iran targeted King Fahd Causeway linking Bahrain and Saudi Arabia would represent a new category of escalation involving major infrastructure. Oil is on course for its largest weekly gain since April, increasing inflation and discount-rate risks for long-duration growth stocks. Separately, US President Donald Trump’s accusation that China carried out a large-scale voter-data breach pushed Australian and New Zealand Dollars lower, adding another risk-off layer for markets already questioning sustainability of AI boom.

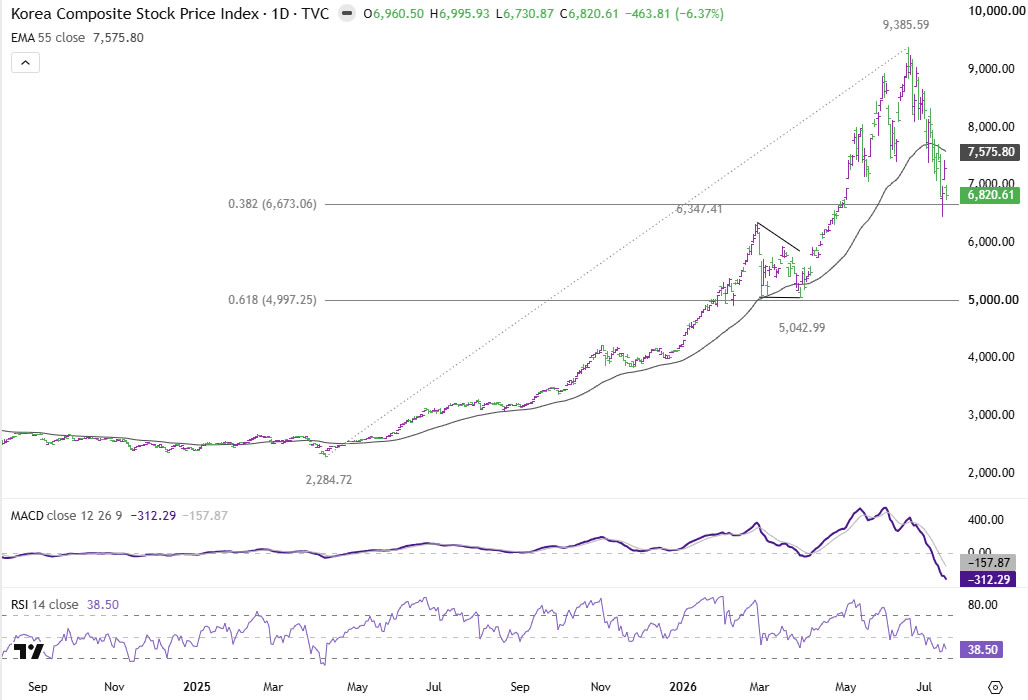

Technically, KOSPI remains most advanced in its correction. Fall from 9,385.59 is correcting entire uptrend from 2,284.72 and has already reached 38.2% retracement at 6,673.06 earlier this week. That level may initially slow downside momentum, but selling could intensify if bearish sentiment spreads further through global semiconductor complex.

Nikkei has now joined breakdown after closing at 64,140.90, well below its 55 D EMA at 65,774.89. Development suggests a medium-term top was formed at 72,831.73. Further decline is expected while 68,798.24 resistance holds, with 60,000 psychological level next target. Firm break there would expose 38.2% retracement of 53,590.24 to 72,831.73 at 56,772.84.

NASDAQ is now critical link. A close below its 55 D EMA, currently at 25628.31 today, would argue that correction from 27,190.21 is extending into another falling leg, bringing 38.2% retracement of 20,690.25 to 27,190.21 at 24,707.22 back into focus.

Further break of 24,707.22 would argue that semiconductor weakness is not confined to individual stocks or Asian markets, but has developed into a global reassessment of AI investment cycle. Korea fired first warning, Japan and Taiwan have followed, and Wall Street must now decide whether investors still trust spending-led AI narrative—or require hard evidence of returns before stepping back in.

{kind=link}