Global stock markets rebounded impressively today as traders looked past the first chapter of US-China trade war. Nikkei closed up 1.53% at 21645.42 earlier today. European indices are all trading up at the time of writing, with DAX gaining 2.44% being most impressive. CAC is up 2.07% while FTSE is up 1.68%. After the massive 700ps come back yesterday, DOW futures point to higher open and could have triple digit gain at open.

In the currency markets, Dollar is trading broadly higher for the day, followed by Kiwi. Swiss Franc is also trying to stage a come back after yesterday’s selloff. Worst than expected trade and job data is having no impact on the greenback. EUR/USD has indeed breached 1.2238 support, suggesting that it’s probably ready to head back to 1.22 handle. Sterling is trading as the weakest one today, after PMI services miss. In particular, GBP/USD breaches 1.4008 and is now having 1.3982 key near term support in radar.

What could China do after soybean weapon?

While stocks markets rebounded strongly today, the initial reaction to China’s retaliation tariff announcement was admittedly astonishing. In particular, announcement of soybean tariff came earlier than we, as well as the majority of market participants, had anticipated. What else can China do after this weapon has already been used? Some suggest that China can shift from tariff to financial markets, e,g.: to deliberately depreciate renminibi and reduce purchase of US government bonds. Here is an articular detailing the two options – China Announced Tariff on US Soybean Exports. What Next?

US trade deficit widened to USD -57.6b

US trade deficit widened to USD -57.6b in February, up USD 0.9b from USD -56.7b in January. Exports rose USD 3b to USD 137.2b. Imports also rose USD 3.3b to 213.2b.

The February figures show surpluses, in billions of dollars, with South and Central America ($3.4), Hong Kong ($3.1), Brazil ($0.9), United Kingdom ($0.6), and Singapore ($0.5).

Deficits were recorded, in billions of dollars, with China ($34.7), European Union ($15.3), Germany ($6.7), Mexico ($6.6), Japan ($6.0), Italy ($2.8), OPEC ($2.3), India ($1.9), Taiwan ($1.5), France ($1.4), South Korea ($1.1), Saudi Arabia ($0.4), and Canada ($0.4).

Initial claims rose 24k to 242k

US initial jobless claims rose 24k to 242k in the week ended March 31, well above expectation of 223k. But it’s still at an ultra low level historically. Prior week’s figure was revised up by 3k to 218k. The four week moving average was up 3k to 228.25k. Continuing claims dropped -64k to 1.81m, lowest since December 1973.

Canada trade deficit widened in March, trade surplus with US narrowed

Canada trade deficit widened to CAD -2.7b in February, from CAD -1.9b. Imports rose 1.9% mom, 3.5% yoy to CAD 48.6b, with energy products leading the way. On the other hand, exports rose 0.4% mom, 1.5% yoy to CAD 45.9b, primarily on higher exports of passenger cars and light trucks.

Canadian trade with the US rebounded after two months of decline. Imports from the US rose 3.3% mom to CAD 32.1b, mostly on aircraft. Exports to the US rose 1.9% mom to CAD 34.6b, mainly on passenger cars and light trucks. Canada’s trade surplus with the US narrowed from CAD 2.9b in January to USD 2.6b in February.

UK PMI Services: Economy iced up in March

UK PMI services dropped sharply to 51.7 in March, down from 54.5 and missed expectation of 54.0. That’s the lowest level in 20 months and it’s “partly linked to snow disruption”. Chris Williamson, Chief Business Economist at IHS Markit noted that the services sector suffered the “”weakest increase in business activity since the Brexit vote amid widespread disruptions caused by some of the heaviest snowfall in years. And as a result, Q1 growth will be “adversely affected”. The PMI surveys pointed to Q1 growth as just under 0.3%, slowed from Q4’s 0.4%. Markit also warned that inflationary pressures “picked up again in March”.

Eurozone PMI Composite: Economy growing at 0.6% quarterly rate

Eurozone PMI services was revised down by -0.1 to 54.9 in March. Markit noted in the release that “the final PMI numbers showed the weakest rise in business activity since the start of last year, adding to signs that the growth spurt has peaked”. PMI data indicates a 0.6% quarterly growth, still “impressive”. Meanwhile, some of the factors for loss in momentum was due to temporary factors, such as “bad weather and short-term capacity constraints”. April’s PMI data will be “particularly important” in “ascertaining true underlying growth momentum and in providing a steer on the likely timing of any ECB policy changes.”

Also from Eurozone, German factor orders rose 0.3% mom in February, below expectation of 1.5% mom. Germany PMI services was revised down from 54.2 to 53.9. France PMI services was revised up from 56.8 to 56.9. Italy PMI services dropped notably from 55.0 to 52.6 in March.

Swiss CPI rose 0.4% mom, 0.8% yoy in March

Swiss CPI rose 0.4% mom, 0.8% yoy in March, above expectation of 0.3% mom, 0.7% yoy. Annual rate also accelerated from February’s 0.6% yoy. But it’s way off the level that will trigger a change in SNB policy. Swiss Federal Statistical Office (FSO) noted that “various factors contributed to the 0.4% rise compared with the previous month, such as an increase in the price of international package holidays, air transport and hotel accommodation. However, prices fell for medicines and fuel.”

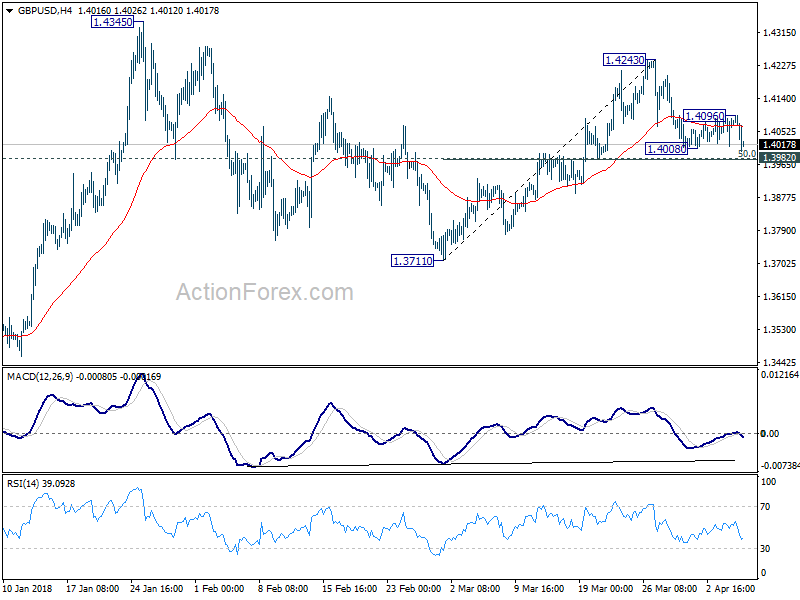

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4029; (P) 1.4062; (R1) 1.4112; More….

GBP/USD drops to as low as 1.3999 today and breaches 1.4008 temporary low. Focus is now on 1.3982 support. Decisive break there will indicate completion of the rise from 1.3711. In that case, intraday bias will be turned back to the downside for retesting 1.3711. Nonetheless, strong rebound from 1.3982, followed by break of 1.4096 minor resistance will turn bias to the upside for 1.4243. Break will resume the rally from 1.3711 for 1.4345 high first.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4259) so far. Break of 1.3038 support, will suggest that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Feb | 0.83B | 0.72B | 1.06B | 0.95B |

| 06:00 | EUR | German Factory Orders M/M Feb | 0.30% | 1.50% | -3.90% | -3.50% |

| 07:15 | CHF | CPI M/M Mar | 0.40% | 0.30% | 0.40% | |

| 07:15 | CHF | CPI Y/Y Mar | 0.80% | 0.70% | 0.60% | |

| 07:45 | EUR | Italy Services PMI Mar | 52.6 | 53.9 | 55 | |

| 07:50 | EUR | France Services PMI Mar F | 56.9 | 56.8 | 56.8 | |

| 07:55 | EUR | Germany Services PMI Mar F | 53.9 | 54.2 | 54.2 | |

| 08:00 | EUR | Eurozone Services PMI Mar F | 54.9 | 55 | 55 | |

| 08:30 | GBP | Services PMI Mar | 51.7 | 54 | 54.5 | |

| 09:00 | EUR | Eurozone PPI M/M Feb | 0.10% | 0.00% | 0.40% | |

| 09:00 | EUR | Eurozone PPI Y/Y Feb | 1.60% | 1.50% | 1.50% | |

| 09:00 | EUR | Eurozone Retail Sales M/M Feb | 0.10% | 0.60% | -0.10% | -0.30% |

| 11:30 | USD | Challenger Job Cuts Y/Y Mar | 39.40% | -4.30% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Feb | -2.7B | -2.1B | -1.9B | |

| 12:30 | USD | Initial Jobless Claims (MAR 31) | 242K | 223K | 215K | 218K |

| 12:30 | USD | Trade Balance Feb | -57.6B | -56.5B | -56.6B | -56.7B |

| 14:30 | USD | Natural Gas Storage | -29B | -63B |

{kind=link}