Asian markets responded positively to the highly anticipated speech by China President Xi Jinping. At the time of writing, Nikkei is trading up 0.65% and HK HSI is up 1.14%. But it should be noted that Nikkei is already trading way off today’s high at 21933.99. We could see the pattern in the US markets overnight repeat. That, DOW initially surged to 24373.18 but ended up closing at 23979.10, up only 0.19 pts. More importantly, DOW closed below yesterday’s open at 24037.52. We’d like to point out that Xi’s speech didn’t do anything to ease the tension between US and China. Markets were probably just relieved as Xi didn’t say anything over the top to worsen the situation.

In the currency markets, commodity currencies are broadly higher today while Yen and Swiss Franc are generally weak. This is in-line with receding risk aversion. The picture is pretty much the same for the week with Aussie, Kiwi and Loonie being strong and Yen being. But the difference is that Dollar is trading as the second weakest one for the week.

Technically, Dollar and Yen will likely continue to be left behind by others. The main question for today is whether Europeans or commodity currencies will lead the way. For now, favors are on Aussie’s and Canadian’s side.

China Xi delivered calm but uninspiring speech

China President Xi Jinping delivered a calm but uninspiring speech at the highly anticipated Boao Forum for Asia today. The markets nonetheless welcomed it. Xi echoed the line of the government on the commitment to global multilateral framework like G20, APEC. And he urged the world not to return to “Cold War” mentality, and “zero-same game thinking”, as they are outdated. Xi also talked about the plans to further open up the massive Chinese markets to foreign investments. The measures would include “significantly” lowering import tariffs for autos, enforcing intellectual property protection, and improving investment protections for foreign companies.

In our view, the tone and messages of Xi’s speech is expected. And important point to note is that the pledge to open up the markets have been delivered by various Chinese leaders for two decades but actual delivery has been relatively small. And whatever Xi said, they are still words for the moment. And more importantly, “China still have the option of opening the markets to all but those who don’t commit to multilateral frameworks.”

So, the speech itself is targeted to the world in general, rather than the US. There was certainly no escalation in the tensions with US resulted from the speech. But Xi didn’t express his intention to solve the tension neither. What’s next still depends on whether Trump will tripled down version of tariffs on USD 150b of Chinese imports in total. Or he will back down again like on other issues.

More details on Xi here with a video of his speech with English translation voice over.

Dallas Fed Kaplan: Trade rhetoric could have chilling effect

Dallas Fed President Robert Kaplan reiterated his expectation for two for rate hikes this year. And, 2018 is seen a a relatively solid year for growth to him. But Kaplan also noted that it is going to be watching the yield curve “very carefully”. And he won’t “blindly” support rate hikes if yield curve keeps flattening.

In addition, like other Fed officials, Kaplan said it’s “too early to judge” how the trade spat between the US and China is going to affect the economy. But he warned that if the rhetoric goes on for long enough at this level, it is “having somewhat a chilling effect”.

He added that “I’m still hopeful when we look back a year or two from now you’ll see very little actually done in the way of tariffs that were implemented”. And, “that would be my base case, and I think we are in the early innings of this.”

Australia NAB business condition dropped sharply from record high, confidence eased

Australia NAB business confidence dropped another 2 pts to 7 in March, down from 9. Business conditions dropped 6 pts from February’s record high at 20 to 14. That’s 3 points lower than January’s 17. Nonetheless, the condition reading remains well above historical average at 5.5. NAB pointed out that the US announcement of tariffs on USD 50b of Chinese imports could have affected sentiments.

NAB saw that “purchase cost growth has been moving higher since late 2016” and that could be “providing a tentative sign of inflationary pressure.” On the other hand, “labour cost (wage bill) growth moderated after rising the previous month”, which could have offset some of the inflationary pressure.

Canadian Dollar urged on positive BoC Business Outlook Survey

Canadian Dollar surged overnight as the BoC’s Business Outlook Survey painted a positive picture. Business sentiments were supported by “healthy” sales prospects. Capacity and labor pressures are “evident” in most regions due to strong demand. In particular, “intentions to increase investment continue to be widespread.” And, “employment intentions are solidly positive, based on firms’ plans for hiring to support expected sales growth or to expand operations.” However, BoC noted some firms cited “rising protectionism and reduced competitiveness” of the US as factors limiting the impact on their sales.

IMF Furusawa: Global economy continues to strengthen on the back of investment and trade

IMF Deputy Managing Director Mitsuhiro Furusawa delivered an opening remarks to the 9th IMF-Japan High-Level Tax Conference for Asian Countries today. There he noted that the global economy continues to “strengthen on the back of investment and trade”. He firstly pointed to “resilient” capital flows to the emerging market. And, the US tax reform is expected to boost growth “temporarily”. For the world, the current upswing provides an “ideal opportunity” for reforms to boost output potential. However, Furusawa also emphasized that this will require “strategies to ensure fiscal sustainability and financial resilience” at the same time.

Elsewhere

US BRC retail sales monitor rose 1.4% yoy in March. Canada will release building permits later today. US PPI and wholesale inventories will also be released.

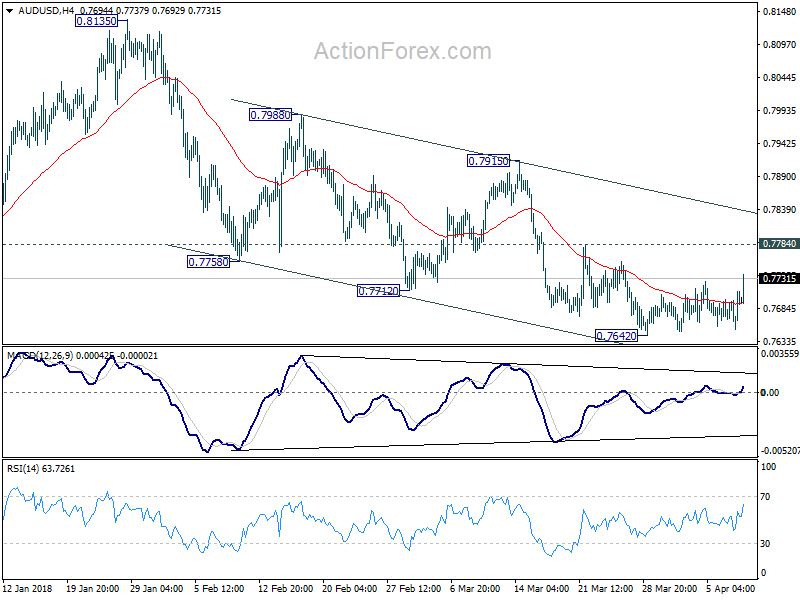

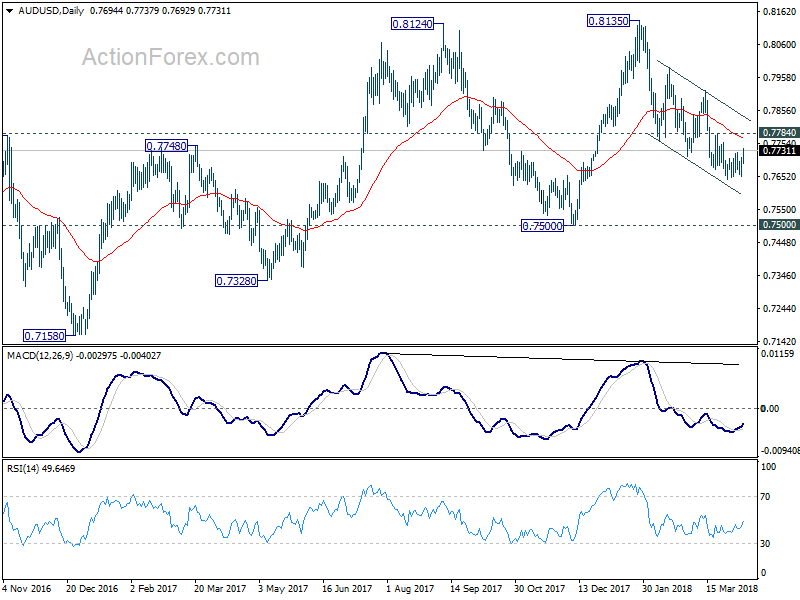

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7665; (P) 0.7687; (R1) 0.7723; More…

AUD/USD recovers strongly today and reaches as high as 0.7737 so far. But still, it’s staying in range between 0.7642 and 0.7784 and intraday bias remains neutral. As long as 0.7784 holds, near term outlook stays bearish for another decline. On the downside, break of 0.7642 will turn bias to the downside to extend recent fall from 0.8135 to retest 0.7500 key support level. On the upside, however, break of 0.7784 will suggest near term reversal and turn bias to the upside for 0.7915 resistance first.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed. In that case, AUD/USD would be heading back to 0.6826 low in medium term.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | BRC Retail Sales Monitor Y/Y Mar | 1.40% | 0.60% | ||

| 1:30 | AUD | NAB Business Conditions Mar | 14 | 17 | 21 | |

| 1:30 | AUD | NAB Business Confidence Mar | 7 | 12 | 9 | |

| 6:00 | JPY | Machine Tool Orders Y/Y Mar P | 39.50% | |||

| 12:30 | CAD | Building Permits M/M Feb | 5.60% | |||

| 12:30 | USD | PPI M/M Mar | 0.10% | 0.20% | ||

| 12:30 | USD | PPI Y/Y Mar | 2.90% | 2.80% | ||

| 12:30 | USD | PPI Core M/M Mar | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y Mar | 2.60% | 2.50% | ||

| 14:00 | USD | Wholesale Inventories M/M Feb F | 0.60% | 1.10% |

{kind=link}