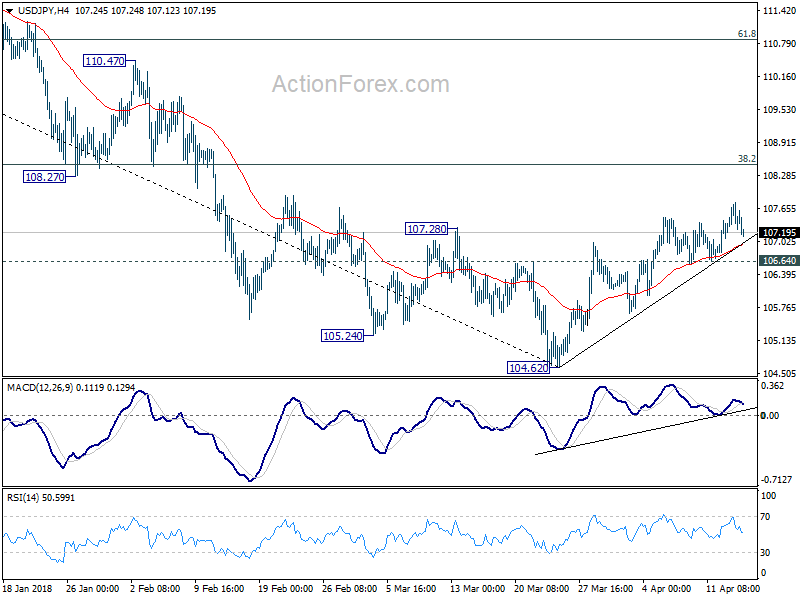

Yen is making a come back in Asian session today. The reaction to the Syria strike was muted. But risk aversion comes back with selloff in Chinese and Hong Kong stocks. Nikkei is maintaining slight gain of 0.25% at the time of writing. But China SSE and Hong Kong HSI are down -1.5% and -1.7% respectively. It’s too early to conclude that the Japanese yen is reversing recent near term decline. But development in major Yen crosses is worth some attention. In particular, 106.64 in USD/JPY is key near term support level to watch.

Elsewhere in the currency markets, commodity currencies including AUD, NZD and CAD are turning a bit softer. But there could be surprises ahead with important events scheduled. Those events include BoC rate decision, Canada CPI and retail sales, Australia employment and RBA minutes, New Zealand CPI and China GDP.

Japan and China agreed to improve tie after first high-level meeting in eight years

The outcome of the first high-level economic talks in eight years between China and Japan appeared to be positive. Japanese Foreign Affairs Minister Taro Kono and Chinese State Councillor Wang Yi met in Tokyo on Sunday. Both agreed to work on strengthening the relationship with more high level visits ahead.

Wang said that “I hope we can begin at a fresh starting point and discuss a new future, while promoting a new cooperative relationship. I want to have in-depth discussions on economic policies, cooperation on the belt and road initiative and further integration of East Asian countries.”

Kono also said that “I hope to hold active discussions about regional and global economic issues. I would also like to take this opportunity to further strengthen economic relations between Japan and China.”

Also more high-level visits were agreed, with Chinese Premier Li Keqiang go to Japan for a Japan-China-South Korea summit. And then Japan Prime Minister Shinzo Abe will visit China while Chinese President Xi Jinping will also visit Japan.

Abe’s support plunged further ahead of meeting with Trump

Separately, Abe will meet with US President Donald Trump at the latter’s Mar-a Lago resort for two days this week starting Tuesday. Ahead of that, polls showed support for Abe continued to plunge. According to a poll by Nippon TV, support for Japan Prime Minister Shinzo Abe dropped to 26.7%, hitting the lowest point after taking office back in December 2012. Another survey by Kydo news agency also showed Abe’s supported from -5.4 points to 37%. Another poll by Asahi also showed Abe’s support at only 31%.

Recent suspected scandals have clearly hurt Abe’s popularity and raised doubts on whether can win a third term as PM as LDP leader in the September vote. Former Prime Minister Junichiro Koizumi questioned whether Abe may “resign around the time parliament’s session ends (on June 20)?”, as quoted in weekly magazine Aera. Koizumi also said that “situation is getting dangerous”.

Nieto, Trudeau and Pence pushing to reach NAFTA agreement within weeks

The push for having a symbolic NAFTA agreement during the the Summit of the Americas failed. But leaders from Mexico, Canada and the US agreed to expedite the efforts. Mexican President Enrique Pena Nieto, US Vice President Mike Pence and Canadian Prime Minister Justin Trudeau met in Lima, Peru, on the sidelines of the Summit of the Americas.

After the meeting, Nieto said there were agreement to “accelerate” the efforts on NAFTA renegotiation. And he added “we hope in the coming weeks we can reach an agreement”.

Trudeau also said “we’d like to see a re-negotiated deal land sooner than later.” And, “we have a certain amount of pressure to try to move forward successfully in the coming weeks.”

Pence also said he left the summit “very hopeful that we are very close to a renegotiated NAFTA”, and “there is a real possibility that we could arrive at an agreement within the next several weeks.”

It’s believed that all parties would like to complete the deal by Mexican elections on July 1.

UK PM May to boost trade with Commonwealth family

The leaders of the 53 Commonwealth member states are meeting in the Commonwealth Heads of Government Meeting this week. UK Prime Minister Theresa May is expected to make use of her speech at the business forum today to boost trade as Brexit looms.

Ahead of the meeting, May said in a statement that “our Commonwealth family already accounts for one-fifth of global trade.” And “we must continue to work together to build further upon this solid foundation by building on our existing trade links and establishing new ones.” May is set to unveil new programs to boost Commonwealth-wide support to women-owned businesses. There will also be new funding for a new Commonwealth Standards Network to establish a common language for goods and services.

Separately, a major push for a “people’s vote” on the final Brexit deal was launched by MPS of different parties, celebrities and business leaders. The MPs included Conservative Anna Soubry, Labour’s Chuka Umunna, the Greens’ Caroline Lucas and Liberal Democrat Layla Moran.

An important week in terms of economic data

It’s an important week ahead in terms of economic data, given the background that three major central banks could raise interest rates in Q2. Fed fund futures are now pricing in 100% chance of a Fed hike in June. Retail sales, housing, regional Fed surveys and Beige Book report are not expected to alter this.

BoE is one that’s widely tipped to hike again in May. And the decision could very much depends on the CPI, employment and retail sales to be released this week.

BoC is generally expected to stand pat this week, given some slowdown in Q1. But still, BoC is expected to hike again the year as the NAFTA uncertainties are cleared, probably two more times. Speculation on the timing of the next move, though, will depends on this week’s BoC statement, as well as Canada CPI and retail sales.

In addition that the above, China GDP, RBA minutes, Australia employment, New Zealand CPI, German ZEW will also be watched.

Here are some highlights for the week ahead:

- Monday: Swiss PPI; US retail sales, Empire state manufacturing index, business inventories, NAHB housing index

- Tuesday: China GDP, industrial production, retail sales, fixed asset investment; RBA minutes; UK employment; German ZEW; Canada manufacturing sales; US housing starts and building permits, industrial product

- Wednesday: Japan trade balance; UK CPI, PPI; Eurozone CPI; BoC rate decision; Fed’s Beige book

- Thursday: New Zealand CPI; Australia employment; Eurozone current account; UK retail sales; US Philly Fed survey, jobless claims, leading indicators

- Friday: Japan CPI, tertiary industry index; Canada CPI, retail sales; Eurozone consumer confidence.

USD/JPY Daily Outlook

Daily Pivots: (S1) 107.10; (P) 107.43; (R1) 107.67; More…

Intraday bias in USD/JPY is turned neutral again with today’s retreat. Further rise could be seen as long as 106.64 minor support intact. But 38.2% retracement of 114.73 to 104.62 at 108.48 9 which is close to 108.12, remains crucial in determining the medium outlook. Break of 106.64, however, will indicate the rebound from 104.62 has completed. And in that case, bias will be turned back to the downside for retesting 104.62.

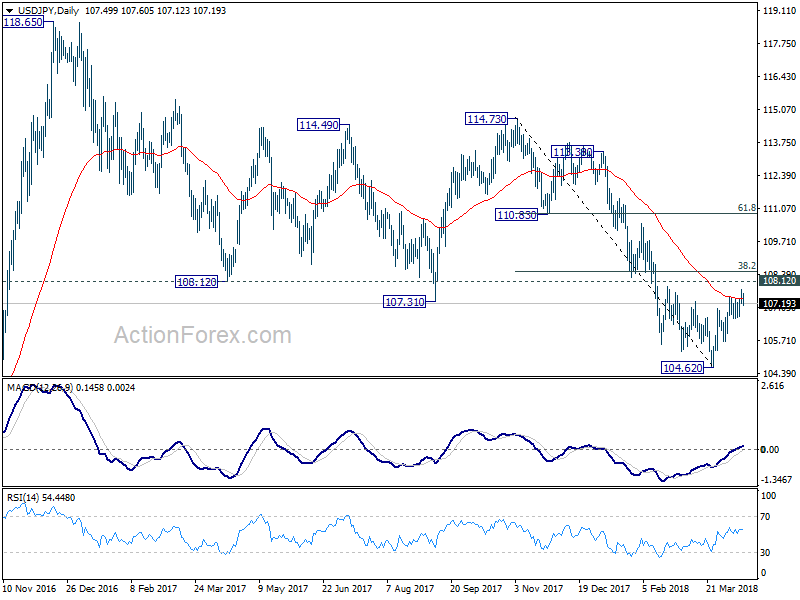

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

In the bigger picture, as long as 108.12 support turned resistance holds, the medium term down trend from 118.65 (2016 high) should still continue lower, at least to retest 98.97 (2016 low). However, sustained break of 108.12 will be an early sign of medium term reversal. In that case, further rise would be seen to 114.73 resistance to confirm completion of the fall from 118.65.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:01 | GBP | Rightmove House Prices M/M Apr | 0.40% | 1.50% | ||

| 6:00 | EUR | German WPI M/M Mar | 0.40% | -0.30% | ||

| 7:15 | CHF | Producer & Import Prices M/M Mar | 0.40% | 0.30% | ||

| 7:15 | CHF | Producer & Import Prices Y/Y Mar | 2.60% | 2.30% | ||

| 12:30 | USD | Empire State Manufacturing Index Apr | 18.6 | 22.5 | ||

| 12:30 | USD | Retail Sales Advance M/M Mar | 0.40% | -0.10% | ||

| 12:30 | USD | Retail Sales Ex Auto M/M Mar | 0.20% | 0.20% | ||

| 14:00 | USD | Business Inventories Feb | 0.60% | 0.60% | ||

| 14:00 | USD | NAHB Housing Market Index Apr | 70 | 70 | ||

| 20:00 | USD | Net Long-term TIC Flows Feb | 62.1B |

{kind=link}