Dollar surges broadly today as boosted by strong rally in treasury yield. 10 year yield reaches as high as 3.049 so far today and breaks key resistance level of 3.036 (2013 high). TNX reaches the highest level since 2011. Released from US, retail sales rose 0.3% mom in April, in line with expectation. Ex-auto sales rose 0.3% mom, below expectation of 0.5% mom. Empire state manufacturing index rose to 20.1, up from 15.8 and beat expectation of 15.0. But these data are shrugged off by traders.

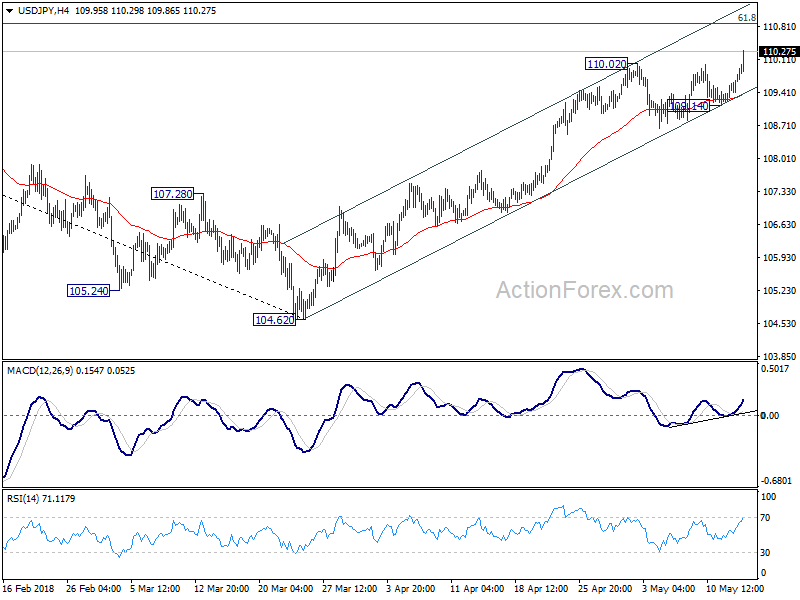

Technically, USD/JPY leads the way with 110.02 short term top broken. Such development is consistent with yield driven Dollar rally. Rise from March low at 104.62 has resumed for 61.8% retracement of 114.73 to 104.62 at 110.86 next. USD/CAD’s breach of 1.2859 minor resistance suggests that pull back from 1.2996 has completed and further rise should be seen to retest this level.

For now, EUR/USD is holding above 1.1822 short term bottom. GBP/USD above 1.3459 short term bottom as the data release from European session provided little inspiration. These two levels will be watched closely today. Also, 1.0036 in USD/CHF will also be eyed.

German ZEW economic expectations deteriorated, UK wage growth met expectation

German ZEW Economic Sentiment was unchanged at -8.2 in May, in line with expectation. German Assessment of Current Situation dropped -0.5 to 87.4, above expectation of 85.2. Eurozone ZEW Economic Sentiment rose 0.5 to 2.4, above expectation of 2.0. Assessment of Current Situation dropped -1.6 to 56.1.

ZEW President Achim Wambach noted in the release that “the US decision to back out of the nuclear treaty with Iran and fears of a further escalation of the international trade conflict with the US, as well as a further rise of crude oil prices, have had an overall negative impact on economic expectations in Germany.”

Also released from during European session, Eurozone GDP grew 0.4% qoq in Q1, unrevised from first estimate. Industrial production rose 0.5% mom in March. German GDP rose 0.3% qoq in Q1, below expectation of 0.4% qoq. Swiss PPI accelerated to 2.7% yoy in April, but miss expectation of 3.0% yoy.

UK unemployment stayed unchanged at 4.2% in March, at the lowest level since 1975. Average weekly earnings rose 2.6% 3moy including bonus, met expectations. Claimant count rose 31.2k in April versus expectation of 13.3k. Sterling’s reaction to the data was muted.

IMF forecasts slower Eurozone growth in 2018, 2019. Urges fiscal reforms

IMF forecasts Eurozone growth to slow to 2.3% this year, from 2017’s 2.4%, and drop further to 2.0% in 2019. IMF noted that “with economic prospects continuing to improve in the short term but medium-term prospects less bright, policymakers should seize the moment to rebuild room for fiscal manoeuvre and push forward with reforms to boost growth potential”

And it pointed out that “policymakers should strive to bring fiscal deficits within range of balance over the next few years.:” With that ” automatic stabilizers and fiscal stimulus can be deployed again, should downside risks materialize.”

BoJ Kuroda: “Absolutely no plan” to raise yield target

BoJ Governor Kuroda told the parliament today that there is “absolutely no plan” to raise the yield target under the Yield Curve Control for now, as inflation is still distant from 2%. He also explained that removing the time frame to meet the 2% inflation target is not necessarily related to the side effect of monetary policy on bank profits.

Regarding YCC, Kuroda said bond purchases are more sustainable under the framework, as the central bank has more flexibility. And, it’s be able to maintain long term year near 0% with smooth operations in JGB purchases.

RBA minutes reiterated no strong case for near term hike

RBA May meeting minutes reiterated that central bank’s stance that it’s not in rush to lift interest rates. The minuted noted that “stronger growth was expected over the following couple of years, which could reduce spare capacity in the economy and lead to a further gradual decline in the unemployment rate.” But, “the increase in wages growth and inflation was expected to be gradual however because spare capacity in the economy was expected to be reduced only slowly.” And, “as progress in lowering unemployment and having inflation return to the midpoint of the target range was expected to be gradual, members also agreed that there was not a strong case for a near-term adjustment in monetary policy.”

RBA Debelle: 2% is the focal point for wage outcomes now

RBA Deputy Governor Guy Debelle delivered a speech titled “The Outlook for the Australian Economy” at the CFO Forum in Sydney today, where he talked about wages. He noted that “the experience of other countries with labour markets closer to full capacity than Australia’s is that wages growth may remain lower than historical experience would suggest.”

Currently in Australia “2% seems to have become the focal point for wage outcomes, compared with 3–4% in the past.” Even so, “”there is a risk that it may take a lower unemployment rate than we currently expect to generate a sustained move higher than the 2% focal point evident in many wage outcomes today”.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 109.33; (P) 109.50; (R1) 109.82; More…

USD/JPY rises to as high as 110.29 so far and the strong break of 110.02 resistance confirms rally resumption. Intraday bias is back on the upside as rise from 104.62 should now target 61.8% retracement of 114.73 to 104.62 at 110.86 next. Firm break there will target medium term trend line resistance at 112.43. On the downside, below 109.14 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, corrective decline from 118.65 (2016 high) has completed with three waves down to 104.62. Rise from 104.62 is possibly resuming the up trend from 98.97 (2016 low). This will be the preferred case as long as 55 day EMA (now at 108.30) holds. Decisive break of 114.73 resistance will confirm our view and target 118.65 and above.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | RBA May Meeting Minutes | ||||

| 02:00 | CNY | Retail Sales Y/Y Apr | 9.40% | 10.00% | 10.10% | |

| 02:00 | CNY | Industrial Production Y/Y Apr | 7.00% | 6.40% | 6.00% | |

| 04:30 | JPY | Tertiary Industry Index M/M Mar | -0.30% | -0.20% | 0.00% | 0.10% |

| 06:00 | EUR | German GDP Q/Q Q1 P | 0.30% | 0.40% | 0.60% | |

| 07:15 | CHF | Producer & Import Prices M/M Apr | 0.40% | 0.30% | -0.20% | |

| 07:15 | CHF | Producer & Import Prices Y/Y Apr | 2.70% | 3.00% | 2.00% | |

| 08:30 | GBP | Jobless Claims Change Apr | 31.2K | 13.3K | 11.6K | 15.7K |

| 08:30 | GBP | Claimant Count Rate Apr | 2.50% | 2.40% | ||

| 08:30 | GBP | Average Weekly Earnings 3M/Y Mar | 2.60% | 2.60% | 2.80% | |

| 08:30 | GBP | ILO Unemployment Rate 3Mths Mar | 4.20% | 4.20% | 4.20% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Mar | 0.50% | 0.70% | -0.80% | -0.90% |

| 09:00 | EUR | Eurozone GDP Q/Q Q1 P | 0.40% | 0.40% | 0.40% | |

| 09:00 | EUR | German ZEW Economic Sentiment May | -8.2 | -8.2 | -8.2 | |

| 09:00 | EUR | German ZEW Current Situation May | 87.4 | 85.2 | 87.9 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment May | 2.4 | 2 | 1.9 | |

| 12:30 | USD | Empire State Manufacturing May | 20.1 | 15 | 15.8 | |

| 12:30 | USD | Retail Sales Advance M/M Apr | 0.30% | 0.30% | 0.60% | |

| 12:30 | USD | Retail Sales Ex Auto M/M Apr | 0.30% | 0.50% | 0.20% | |

| 14:00 | USD | Business Inventories Mar | 0.10% | 0.60% | ||

| 14:00 | USD | NAHB Housing Market Index May | 70 | 69 | ||

| 20:00 | USD | Net Long-term TIC Flows Mar | 49.0B |

{kind=link}