{kind=link}

Dollar and Sterling are trading mixed as another week starts, but both remain the two weakest currency for the month. The greenback will try hard to draw something from FOMC statement to halt its decline, but that’s unlikely. Meanwhile, US and UK GDP for Q2 will also catch much attention. Latest economic projections from IMF showed that the world is going to rely less on US and UK for growth this year. And that is, generally speaking, in line with the current market sentiment. In other markets, Gold is staying firm above 1250 handle while WTI crude oil is hovering between 45.5/46.0.

IMF kept global forecast unchanged, downgraded US and UK

In the latest World Economic Outlook released over the weekend, IMF kept global growth forecast unchanged at 3.5% for 2017 and 3.6% for 2018. It saw risks "broadly balanced" for the short term but "skewed to the downside" for the medium term. It pointed out that "protracted policy uncertainty or other shocks could trigger a correction in rich market valuations, especially for equities, and an increase in volatility from current very low levels". And, "in turn, this could dent spending and confidence more generally, especially in countries with high financial vulnerabilities."

Growth forecasts for the US was lowered to 2.1% in 2017 and 2.1% in 2018, down from April projection of 2.3% and 2.5% respectively. IMF noted the "uncertainty" over US President Donald Trump’s policies as the main factor for the downward revision. IMF said that "the major factor behind the growth revision, especially for 2018, is the assumption that fiscal policy will be less expansionary than previously assumed, given the uncertainty about the timing and nature of U.S. fiscal policy changes."

IMF also downgraded UK growth forecast for 2017 to 1.7% , down from prior projection of 2.0%. For 2018, growth forecast was kept unchanged at 1.5%. It noted that the revision was based on "weaker-than-expected activity in the first quarter." Also, IMF warned that "the ultimate impact of Brexit on the United Kingdom remains unclear." The UK treasury responded by noting that "this forecast underscores exactly why our plans to increase productivity and ensure we get the very best deal with the EU, are vitally important."

China’s growth is projected to be at 6.7% in 2017 and 6.4% in 2018, revised up from prior projection of 6.6% and 6.2% respectively. Eurozone growth is forecast to be at 1.9% in 2017, 1.7% in 2018, upgraded from prior projection of 1.7% and 1.6% respectively. Japan growth is forecast to be at 1.3% in 2017, upgraded from prior 1.2%. For 2018, growth projection for Japan is kept unchanged at 0.6%.

UK Liam Fox to seek post Brexit trade deal with US

UK International Trade Secretary Liam Fox will meet with US Trade Representative Robert Lighthizer for two days in Washington this week. A post-Brexit trade deal is the main topic of discussion. The Department for International Trade said that the discussion will focus on "providing certainty, continuity and increasing confidence for UK and US businesses as the UK leaves the EU". Fox said that the "working group is the means to ensure we get to know each other’s issues and identify areas where we can work together to strengthen trade and investment ties."

Meanwhile, the British Chambers of Commerce director general Adam Marshall said that "we’re just getting back into the game of doing this sort of thing after 40 years of doing it via the EU." And he warned that "early on in the process, it would be concerning if the UK were to go up against the US on a complex and difficult negotiation." Meanwhile, Trade Union Congress head Frances O’Grady criticized that "ministers should be focused on getting the best possible deal with the EU, rather than leaping into bed with Donald Trump."

Japan PMI manufacturing dropped slightly

Japan PMI manufacturing dropped slightly by 0.2 points to 52.2 in July, below expectation of 52.3. Markit noted that "the slowdown was driven by stagnation in export orders, amid reports of weaker demand from Southeast Asia markets." Nonetheless, "the sector continues to add jobs, with employment growth remaining among the best since the financial crisis, while optimism hit its highest level in five years of data collection."

Eurozone PMIs will be the main focuses in European session. Later in the day, US will release PMIs, existing home sales. Canada will release wholesale sales.

FOMC as the focus of the week

Looking ahead, the focus of the week is the FOMC meeting due Wednesday. The dilemma facing the Fed is the continuation of moderate growth and labor market improvement on one hand, and the subdued inflation on the other hand. We are interested to see how the Fed would described the inflation weakness of late, especially of it would continue to described the softness as "transitory". Special attention is also paid on any more detail on the timing of an announcement on the beginning of balance sheet normalization.

Meanwhile much attention will be on other data, in particular Q2 GDP from US and UK. Others include German Ifo, New Zealand trade balance, Australia CPI and Japan CPI. Here are some highlights of the week:

- Tuesday: German Ifo; US house prices, consumer confidence

- Wednesday: New Zealand trade balance; Australia CPI; Japan corporate service price; Swiss UBS consumption; UK GDP, BBA mortgage approvals; US new home sales; FOMC rate decision

- Thursday: Australia import price; German Gfk consumer confidence; Eurozone M3; US jobless claims, durables, trade balance, wholesale inventories

- Friday; Japan CPI, unemployment rate, household spending, retail sales; Australia PPI; French GDP; Swiss KOF; Eurozone confidence indicators; German CPI; Canada GDP; US GDP

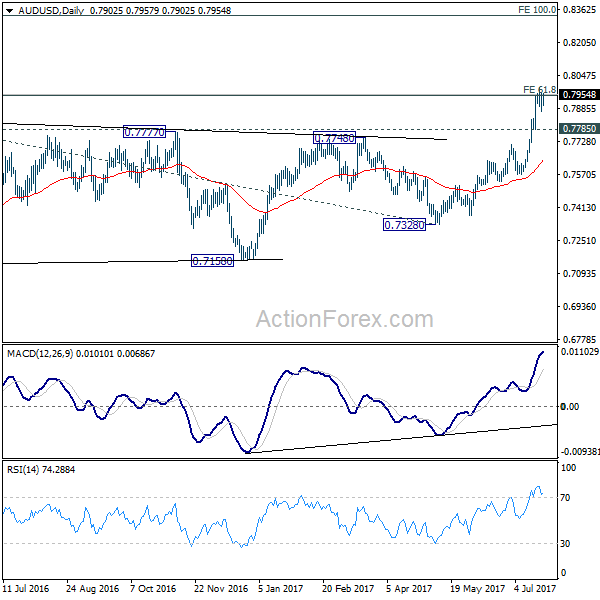

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7872; (P) 0.7915; (R1) 0.7956; More…

AUD/USD recovers mildly today but stays below 0.7988 temporary top. Intraday bias remains neutral as consolidation from there might extend. Another fall cannot be ruled out. But near term outlook will remain bullish as long as 0.7785 support holds and another rise is expected. Break of 0.7988 will target 100% projection of 0.6826 to 0.7833 from 0.7328 at 0.8335 next. However, break of 0.7785 will argue that deeper pull back in under way and could target 55 day EMA (now at 0.7640).

In the bigger picture, current development suggests that rebound from 0.6826 is developing into a medium term rise. There is no confirmation of trend reversal yet and we’ll continue to treat such rebound as a corrective pattern. But in any case, further rise is now expected to 55 month EMA (now at 0.8100) or even further to 38.2% retracement of 1.1079 to 0.6826 at 0.8451. Break of 0.7328 support is needed to confirm completion of the rebound. Otherwise, further rise is now expected.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | JPY | Manufacturing PMI Jul P | 52.2 | 52.3 | 52.4 | |

| 7:00 | EUR | France Manufacturing PMI Jul P | 54.6 | 54.8 | ||

| 7:00 | EUR | France Services PMI Jul P | 56.7 | 56.9 | ||

| 7:30 | EUR | Germany Manufacturing PMI Jul P | 59.2 | 59.6 | ||

| 7:30 | EUR | Germany Services PMI Jul P | 54.3 | 54 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Jul P | 57.2 | 57.4 | ||

| 8:00 | EUR | Eurozone Services PMI Jul P | 55.4 | 55.4 | ||

| 12:30 | CAD | Wholesale Sales M/M May | 0.50% | 1.00% | ||

| 13:00 | CNY | Conference Board Leading Index Jun | ||||

| 13:45 | USD | Manufacturing PMI Jul P | 52.2 | 52 | ||

| 13:45 | USD | Services PMI Jul P | 54 | 54.2 | ||

| 14:00 | USD | Existing Home Sales Jun | 5.59M | 5.62M |