{kind=link}

Commodity currencies, including Canadian, Australian and New Zealand Dollar are suffering steep selling towards the end of the week. New White House economic adviser Larry Kudlow’s strong Dollar comment was seen by some as a factor, as he urged TV interview viewers to “buy King Dollar and sell gold”. But looking from the large picture in the markets, Dollar is just trading marginally better than the above three. Yen remains the strongest one for the week, and for today. The resilient Sterling follows closely as the second strongest one.

Increasing gestures of protectionism of US President Donald Trump and concerns of trade war is seen as the main factor driving the commodity currencies down. Canadian Dollar has its own problems in NAFTA renegotiation and the risk of the return of steel tariffs. Trump’s administration is work on the USD 60b a year unilateral tariffs on China. Australia and New Zealand, with China as largest trade partners, would definitely be affected on contagion. While Australian government might view the US ally, to investors, “America first” Trump wouldn’t care much about casualties elsewhere.

IMF Lagarde: Fix economic imbalances with fiscal means, not trade obstacles

IMF Managing Director Christine Lagarde urged politicians to “resolve trade disagreements without resort to exceptional measures”. She warned that “trade wars not only hurt global growth, but they are also unwinnable”. And, “self-inflicted harm of import tariffs can be substantial even when trade partners do not retaliate with tariffs of their own.” She added that ” protectionism is pernicious, because it puts the biggest strain on the poorest consumers who buy relatively more low-priced imports.” And “harming trade is bad for the economy and bad for people.”

She emphasized “the way to address global economic imbalances is not to raise new obstacles to trade.” That is, by “using fiscal means to address global imbalances is critical”, including “lowering deficits in the US to bring public debt towards a sustainable path, and stronger infrastructure investment and education spending in Germany,” At the same time, ” those who are adversely affected by globalization and technological progress should receive more support to ensure that they can invest in their skills and transition to higher-quality jobs.”

The IMF’s Global Prospects and Policy Challenges report also noted that “the global expansion is gaining strength from the pick-up in international trade, and it should not be put at risk by the adoption of inward-looking policies.” “The modernization of the rules-based multilateral trade system should continue, anchored in the World Trade Organization, with well-enforced rules that promote competition and a level playing field. Co-operation is also needed to tackle excess global imbalances.” The report also warned “the re-emergence of unilateral trade restrictions may escalate tensions and fuel global protectionism, disrupting worldwide supply chains and affecting long-term productivity.”

USD 60b tariffs on Chinese goods is devastating to American families

U.S. Chamber of Commerce President and CEO Thomas Donohue criticized that unilateral tariffs on Chinese goods by Trump’s government would be destructive to the economy. He warned that the USD 30b a year tariffs on Chinese good would “wipe out over a third of the savings American families received from the doubling of the standard deduction in tax reform.” Further, with Trump’s request of USD 60b a year tariff, “the impact would be even more devastating.”In addition, Donohue said “tariffs could lead to a destructive trade war with serious consequences for U.S. economic growth and job creation,”

UK-EU planning intensive talk on Irish border

UK Brexit Secretary David Davis is targeting to complete the legal text of the transition deal at the two-day summit from March 22. Most of the differences would likely be bridged on the following days. But the criteria of avoiding a hard Irish border remains a key showstopper. EU proposed a fall back option in its own draft published earlier this month. That is, should there be no compromisable solution, Norther Ireland would stay in the customs union along side Republic of Ireland. But UK Prime Minister Theresa May has instantly and bluntly rejected that idea. Intensive talk is now planned between March 26 and April 18 on the issue. There is some optimism on completing the transition agreement among UK officials. But businesses in UK would definite request a deal with full clarity. Any conditions in the deal attached to the outcome of Irish border issue would dissatisfy UK businesses and markets.

RBA Debelle: Markets underpriced risks of global tightening

RBA Deputy Governor Guy Debelle warned that markets are under pricing the risks of global monetary stimulus remove. He pointed to “equity prices embody a view of the future that robust growth can continue without generating a material increase in inflation.” And, “there is little priced in for the risk that this may not turn out to be true.” Meanwhile, to him, the market volatility back in February, with sudden selloff in stocks, was just “a small example of what could happen following a larger and more sustained shift upwards in the rate structure.” He admitted before wrong in predicting higher volatility before, but added “I think there is a higher probability of being proven correct this time.”

NZ PMI suggests Q1 manufacturing GDP similar to Q4’s

New Zealand Business NZ manufacturing PMI dropped to 53.4 in February, down from 54.4. Among the sub-indices, production rose 0.4 to 53.9, employment rose 3.3 to 54.8, new orders rose 5.1 to 54.8, deliveries rose 2.9 to 52.7. But finished stocks dropped -1 to 51.1. Bank of New Zealand economist Doug Steel noted in the release that “Q1 manufacturing GDP wouldn’t be much different from Q4’s based on the “generally slower PMI”. Business NZ manufacturing executive director Catherine Beard said pace of expansion had levelled off in recent months and “noted the sluggish start to the year with a dip in new orders being a common message.”

February 25 imagery suggests North Korea testing nuclear reactors at Yongbyon

Defence & security intelligence analysts Jane’s reported that North Korea likely had preliminary testing it’s nuclear reactors at the Yongbyon research facility. That came weeks ahead of the planned meeting between North Korean Leader Kim Jong-un and South Korean President Moon Jae-in next month. There will also be a planned meeting between Kim and US President Donald Trump in May. But it should be noted that the analysis was based on an imagery from February 25. And, the experimental light water reactor (ELWR) was built and optimized for electricity production. Nonetheless, it still has ‘dual-use’ potential and can be modified to produce fissile material for nuclear weapons.

Looking ahead

Eurozone CPI final will be the main feature in European session. Canada will release manufacturing sales and international securities transactions. US will release housing starts, building permits, industrial production and U of Michigan consumer sentiments.

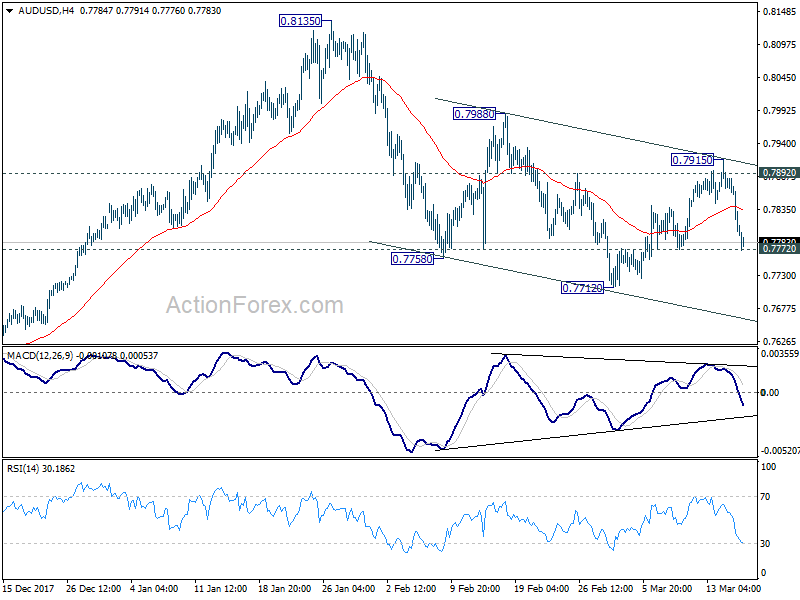

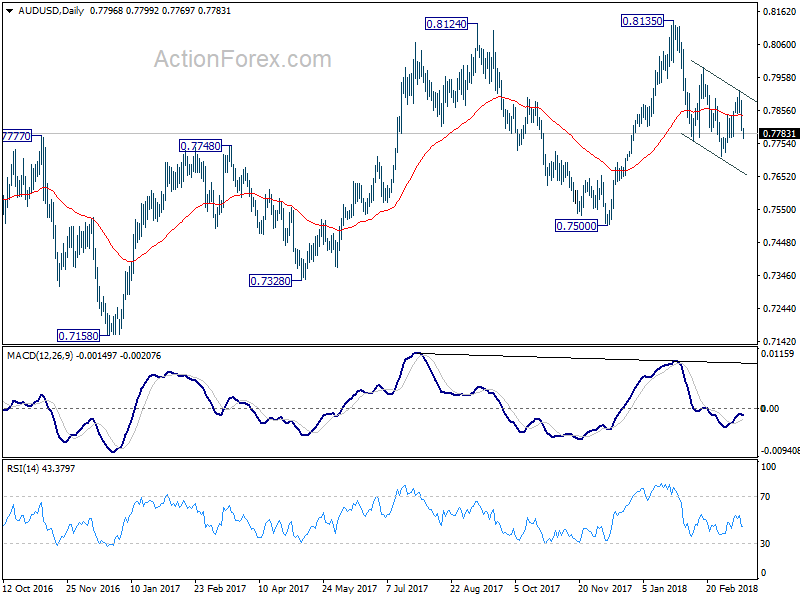

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7766; (P) 0.7825; (R1) 0.7856; More…

AUD/USD failed to sustain above 0.7892 resistance and topped at 0.7915. Subsequent sharp fall now turns focus back to 0.7772 minor support. Break there will likely resume the decline from 0.8135 through 0.7712. In that case, AUD/USD should target 0.7500 key support next. On the upside, break of 0.7915 resistance will revive the case of near term reversal. And, intraday bias will be turned back to the upside for 0.8135 top.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we’d expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Feb | 53.4 | 55.6 | 54.4 | |

| 04:30 | JPY | Industrial Production M/M Jan F | -6.60% | -6.60% | ||

| 10:00 | EUR | Eurozone CPI M/M Feb | 0.20% | -0.90% | ||

| 10:00 | EUR | Eurozone CPI Y/Y Feb F | 1.20% | 1.30% | ||

| 10:00 | EUR | Eurozone CPI Core Y/Y Feb F | 1.00% | 1.00% | ||

| 12:30 | CAD | Manufacturing Sales M/M Jan | -0.90% | -0.30% | ||

| 12:30 | CAD | International Securities Transactions (CAD) Jan | -1.97B | |||

| 12:30 | USD | Housing Starts Feb | 1.30M | 1.33M | ||

| 12:30 | USD | Building Permits Feb | 1.33M | 1.38M | ||

| 13:15 | USD | Industrial Production M/M Feb | 0.30% | -0.10% | ||

| 13:15 | USD | Capacity Utilization Feb | 77.70% | 77.50% | ||

| 14:00 | USD | U. of Mich. Sentiment (Mar P) | 99.3 | 99.7 |