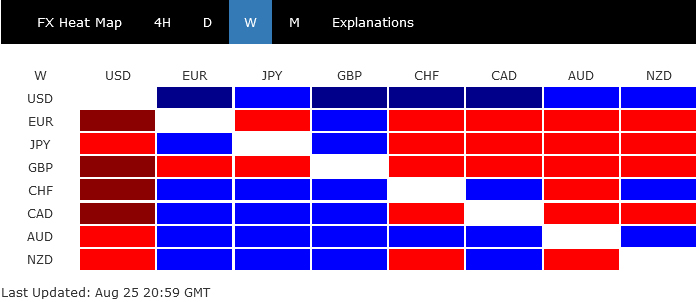

Dollar clinched the title of the week’s best performing currency, even though there was just muted impact from Fed Chair Jerome Powell’s remarks at Jackson Hole. While Powell’s renewed commitment to combating inflation prompted traders to elevate their expectations for another rate hike within the year, broader market reactions, notably in equities and bonds, were rather subdued. Clearly, investors are taking a long view beyond the anticipated pause in September.

On the other side of the pond, Sterling and Euro languished, standing out as the week’s most notable underperformers. The disappointing set of services PMI data confirmed the slowing pace of economic activity in both UK and Eurozone. This data, coupled with the looming threat of a recession, poses a quandary for the BoE and ECB. Both institutions find themselves navigating the challenging task of reining in stubbornly high inflation without inadvertently triggering an economic downturn.

Interestingly, amidst the broader European gloom, Swiss Franc emerged as a beacon of strength, clinching the position of the week’s second strongest currency. Nevertheless, this strength was largely attributable to buying activity against both Euro and Sterling.

Down under, Australia spearheaded the advance among the commodity currencies, though their gains were largely muted, with much of the global attention being fixated on developments in US and Europe. The shadow of uncertainty continues to loom large over China, with concerns about its economic recovery and vulnerabilities in its property and financial sectors potentially setting the stage for future turbulence, which would drag down the commodity currencies again.

Lastly, Japanese Yen offered a mixed performance. While it appeared largely range-bound, there were subtle indications of growing bearish momentum when pitted against the resilient greenback.

Odds of another Fed hike rose after Powell, but not in Sep

Fed Chair Jerome Powell’s highly anticipated speech at the annual Jackson Hole symposium provided the financial markets with some insightful takeaways. While the overall tone was marginally more hawkish than anticipated, it wasn’t as alarming as some had feared. The equity and bond markets responded with steadiness, signaling no drastic shifts in sentiments.

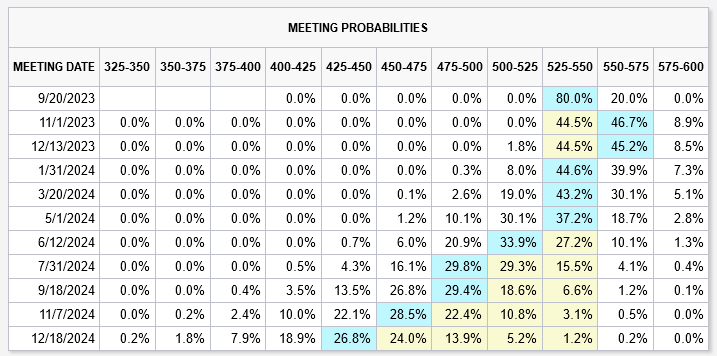

The current market pricing is still firm on a pause at the September FOMC meeting. However, the likelihood of another rate increase within the year has now gained traction. Nevertheless, future actions from Fed will hinge significantly on forthcoming data, particularly the upcoming Non-Farm Payroll and inflation metrics.

Interestingly, Powell’s narrative mirrored the one from his previous Jackson Hole address a year ago, emphasizing the combat against inflation. Although there’s been a recent easing in core inflation, Powell took a conservative stance by emphasizing that “two months of good data are only the beginning of what it will take to build confidence.”

Highlighting Fed’s commitment, Powell maintained that they “are prepared to raise rates further if appropriate” and reiterated the pledge to “hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”

Fed fund futures are currently still pointing to a hold in September, with 80% chance. Yet, in the wake of Powell’s address, the odds favoring a 25bps rate hike either in November or December rose above the 50% mark.

S&P 500 has indeed closed slightly higher on Friday after initial sell-off. But risk is mildly on the downside for the near term, after Thursday’s single day reversal. That is, corrective fall from 4607.07 is in favor to continue. Break of 4335.31 will extend the decline to 38.2% retracement of 3491.58 to 4607.07 at 4180.85, which is close to medium term channel support.

Outlook is similar for NASDAQ. The post Nvidia bounce on Thursday was rather disappointing as the index ended in a single day reversal too. Risk is mildly on the downside for the near term. Break of 13161.76 will extend the correction from 14446.55 to 38.2% retracement of 10088.82 to 14446.55 at 12781.89.

10-year yield breached 4.333 resistance last week but failed to sustain above there, and closed lower at 4.239. For the near term, outlook will stay bullish as long as 4.094 resistance turned support holds. There question is on whether there in enough selloff in the US bond markets to push 10-year yield firmly above 4.333, to target 61.8% projection of 1.343 to 4.333 from 3.253 at 5.100.

Dollar index ended the rebound from 99.57 last week and hit as high as 104.44. Further rise is expected as long as 102.84 resistance turned support holds, to 38.2% retracement of 114.77 to 99.57 at 105.37. For now, this rebound is more seen as a corrective move. Thus, strong resistance could be seen from 105.37 to limit upside to complete the rebound. Yet, sustained break of 105.37, coupled with intensified risk aversion in the broader markets, would argue that DXY is already reversing the whole down trend form 114.77 (2022 high).

ECB Lagarde’s measured messaged overshadowed by recession risks

ECB President Christine Lagarde stayed out of the debate over whether the ECB should lift interest rates again in September. She reiterated that “It’s critically important that inflation expectations remain anchored at 2 per cent.” Lagarde reinforced that the ECB is “deliberately, decisively data-dependent” and committed to taking decisions one meeting at a time.

But overall, hawks seemed to have a louder voice out of Jackson hole, with Bundesbank President Joachim Nagel saying it’s premature to consider a pause. Latvia’s Martins Kazaks said he would err on the side of raising rates despite risks on both sides. Austrian Robert Holzmann said “a little more should be added.”

But in the background, Euro has been weighed down by dismal economic data over the week. In particular, PMI data indicated that the services sector in Eurozone is losing the steam to offset the manufacturing recession, while Germany has become the “sick man” of the region. Recession risk is generally on the rise.

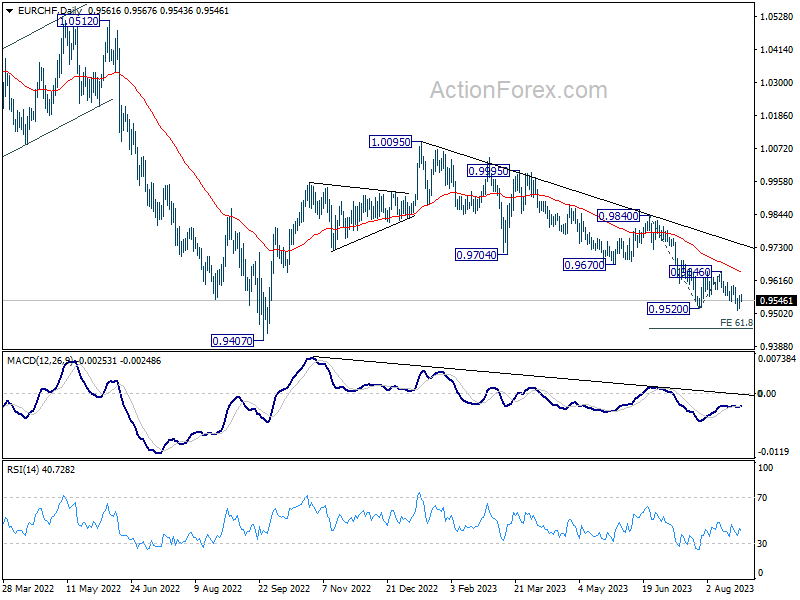

EUR/CHF attempted down trend resumption last week but quickly recovered after breaching 0.9520 to 0.9513. Nevertheless, overall outlook is clearly bearish with the cross capped well below falling 55 D EMA. Break of 0.9513 will pave the way to 61.8% projection of 0.9840 to 0.9520 from 0.9646 at 0.9448. Whether EUR/CHF can dive beyond 2022 low of 0.9407 hinges significantly on how the looming recession unfolds.

Sterling weak as UK’s outlook not better than Eurozone’s

Amid global concerns about economic downturn, UK is not exempt from the rising tide of recession risks. Recent PMI data has put UK on par with Eurozone in terms of gloomy outlook. The speed of decline in services sector has particularly taken analysts by surprise. Even though BoE is largely anticipated to further tighten its monetary stance by raising rates to 5.50% next month, the futures market has grown more skeptical. Presently, there’s just a one-in-three probability being priced in for rates to touch the 6% mark in the foreseeable future.

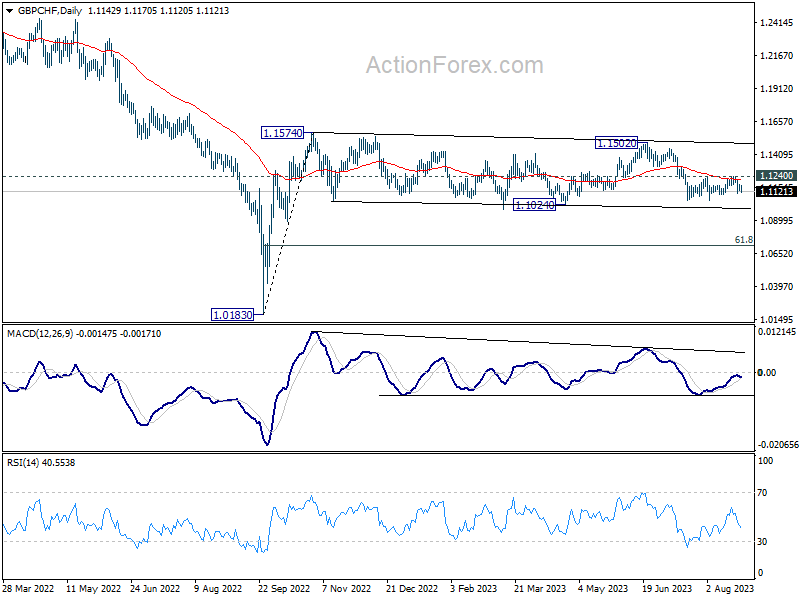

GBP/CHF has turned into sideway trading since mid-July, and it’s still holding above 1.1024 support. However, risks for an intensified selloff is growing after rejection by 55 D EMA . For now, further fall is in favor as long as 1.1240 resistance holds. Sustained break of 1.1024 will confirm breakout from the medium term range from 1.1574, and pave the way to 61.8% retracement of 1.0183 to 1.1574 at 1.0174.

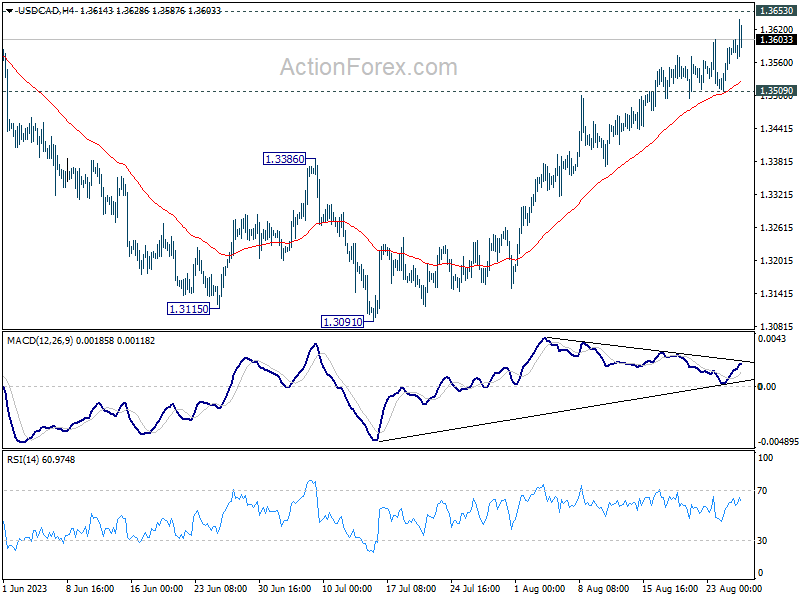

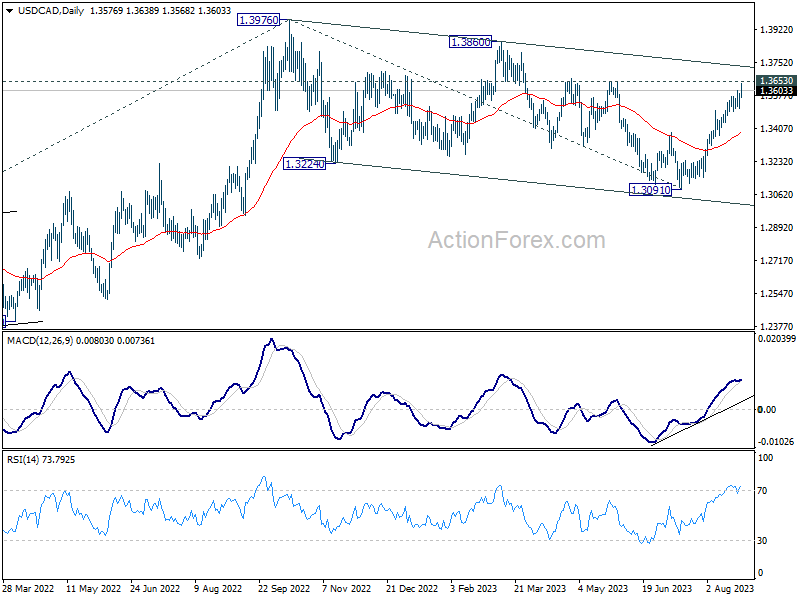

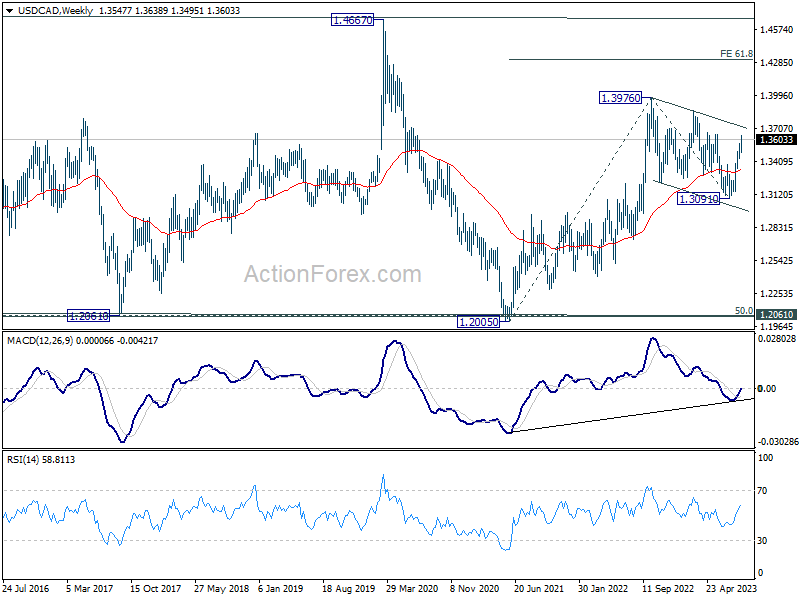

USD/CAD Weekly Outlook

USD/CAD’s rally from 1.3091 continued last week despite some interim retreat. Initial bias is now on the upside this week for 1.3653 resistance. Decisive break there will confirm that correction from 1.3976 has completed, a target a test on this high. On the downside, however, break of 1.3509 support will indicate short term topping, and turn bias to the downside for some correction first.

In the bigger picture, price actions from 1.3976 are viewed as a corrective pattern only. Upon completion, rise from 1.2005 (2021 low) would resume through 1.3976. Next target is 61.8% projection of 1.2005 to 1.3976 from 1.3091 at 1.4309. For now, this will remain the favored case as long as 55 D EMA (now at 1.3387) holds.

In the longer term picture, price actions from 1.4689 (2016 high) are seen as a consolidation pattern only, which might have completed at 1.2005. That is, up trend from 0.9506 (2007 low) is expected to resume at a later stage. This will remain the favored case as 55 M EMA (now at 1.3044) holds.

{kind=link}