Last week’s market action displayed a familiar theme: investors are choosing to focus on growth — even if it’s fragile — and political clarity, however fleeting. US equities roared to record highs as a wave of macro and policy news washed over Wall Street.

Yet the outlook is far from simple. The 90-day tariff truce expires July 9. Markets are now facing a unilateral shift in US policy that threatens to escalate trade tensions. The era of bespoke deals appears to be giving way to a blanket tariff regime. The risk of fragmentation in global trade architecture is also growing by the day.

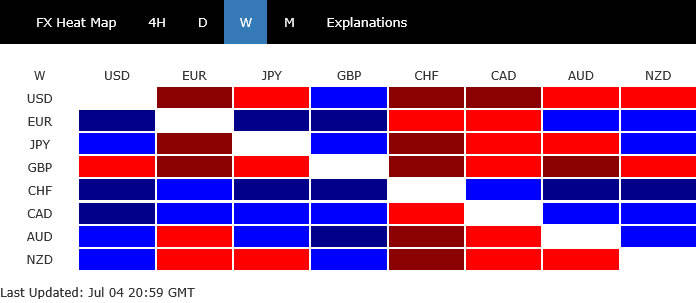

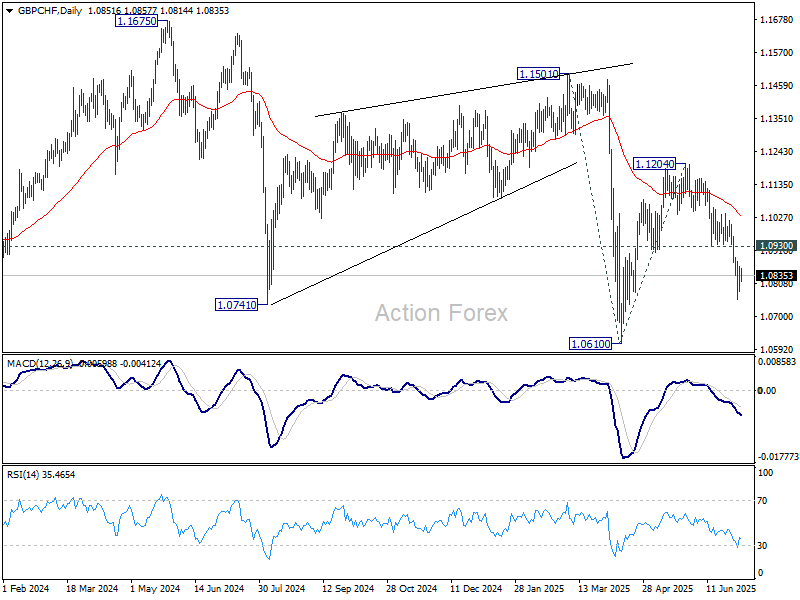

In the currency markets, Swiss Franc stood out as the strongest performer, supported by a better-than-expected inflation report that eased deflation fears. On the flip side, Sterling was hammered by domestic political uncertainty. The contrast is clearly reflected in the downturn of GBP/CHF, logging the largest weekly drop among major currency pairs and crosses.

Overall, Lonnie was the second best, while Euro was third. Dollar was the second worst, trailed by Kiwi. Euro and Yen ended in the middle.

US Equities Hit Record Highs Amid Policy Deluge

US stocks ended the shortened week on a high note,, with S&P 500 and NASDAQ closing at fresh record highs and DOW not far behind. Investors digested a flood of major developments, from economic data to fiscal and trade news, and came away still leaning risk-on. The positive mood suggests that the combination of resilient jobs growth and aggressive fiscal support is outweighing concerns around tighter monetary for longer or geopolitical headwinds.

A stronger-than-expected June non-farm payroll report dented hopes of a July rate cut. But the solid data — coupled with signs of wage deceleration — pointed to cooling, yet healthy labor market, fueling optimism about a soft landing. Meanwhile, the final passage of President Donald Trump’s sweeping tax-and-spending bill added to market momentum, despite raising longer-term deficit risks.

Trump signed the bill into law on July 4, securing a political victory. While the bill passed by a razor-thin margin, markets responded positively to the policy clarity. A blend of corporate tax cuts, defense spending hikes, and welfare reductions added fuel to the rally, even as concerns simmer over its inflationary consequences.

Markets also took comfort in the fact that the Fed is now seen as staying on hold in July, avoiding premature policy action. At the same time, cooling wage pressures imply that the door remains open for gradual easing later in the year. The balance between data-dependent Fed patience and fiscal stimulus-driven growth is proving to be equity-friendly.

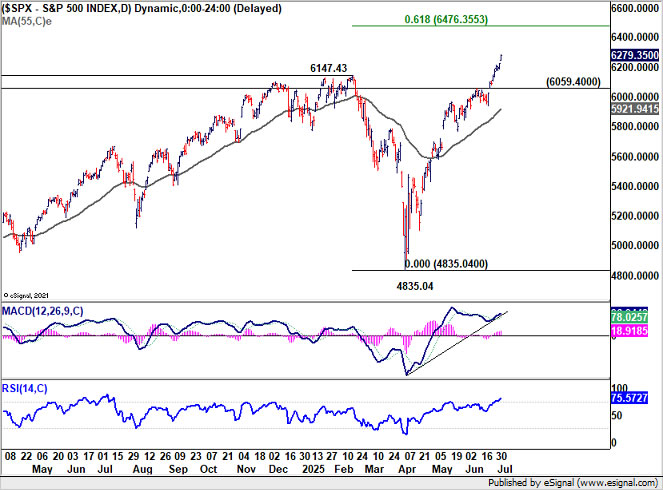

Technically, S&P 500’s upside re-acceleration, as seen in D MACD caught us by surprise. Nevertheless, with the sold break of 6147.43 resistance. long term up trend has resumed. Near term outlook will now stay bullish as long as 6059.30 resistance turned support holds.

The key hurdle for S&P 500 is now between 61.8% projection of 3491.58 to 6147.43 from 4835.04 at 6476.35, and long term channel resistance (now at around 6640). Strong resistance could be seen from this zone to cap upside, at least on first attempt.

Tariff Truce Ends, Global Trade to be Redefined

Trump confirmed on Friday that letters have been signed to 12 countries, detailing specific tariff rates they will face — a clear shift from earlier pledges of bilateral deals. These “take it or leave it” offers will be sent on Monday, just ahead of the July 9 truce deadline. Markets are bracing for fallout as the era of blanket tariffs inches closer to reality.

Back in April, Trump initially floated a 10% base tariff and additional charges up to 50%. Those surcharges were suspended for 90 days to allow for negotiations. But with the grace period ending, the administration may now opt for even higher rates, possibly up to 70%, and most measures are slated to take effect August 1.

So far, only two countries — the UK and Vietnam — have struck deals. The UK retained a 10% rate and won carve-outs for auto and aerospace industries. Vietnam secured lower-than-feared tariffs, with a 20% rate on many goods and a 40% levy on suspected transshipments. US exports to Vietnam will face no tariffs.

Europe’s talks with Washington appear stuck. European Commission President Ursula von der Leyen acknowledged the best hope might be a thin political agreement. She warned that if no deal is reached by July 9, “all instruments are on the table.” The EU could resort to retaliatory tariffs or legal challenges at the WTO.

Beyond official negotiations, global supply chains are shifting. Malaysia announced provisional duties on Chinese, Korean, and Vietnamese steel, effective Monday, signaling broader trade fragmentation. These duties range from 3.86% to nearly 58%, pending a final ruling in November.

Meanwhile, China has retaliated against Europe. Duties up to 34.9% will be imposed on EU brandy, effective Saturday. Large cognac makers can avoid them by agreeing to minimum price floors. The move is widely seen as payback for the EU’s tariffs on Chinese EVs.

Chinese foreign minister Wang Yi recently told the EU that Beijing opposes a Russian defeat in Ukraine — a warning that excessive Western pressure on Moscow may eventually boomerang toward China. Trade is becoming a key theater in this broader contest.

While investors may hope for de-escalation, the trend is clear: Washington is consolidating control over its trade terms, and other nations are scrambling to respond. How this plays out over the next few weeks will shape the second half of 2025.

Dollar Finds No Lift from Fed Caution

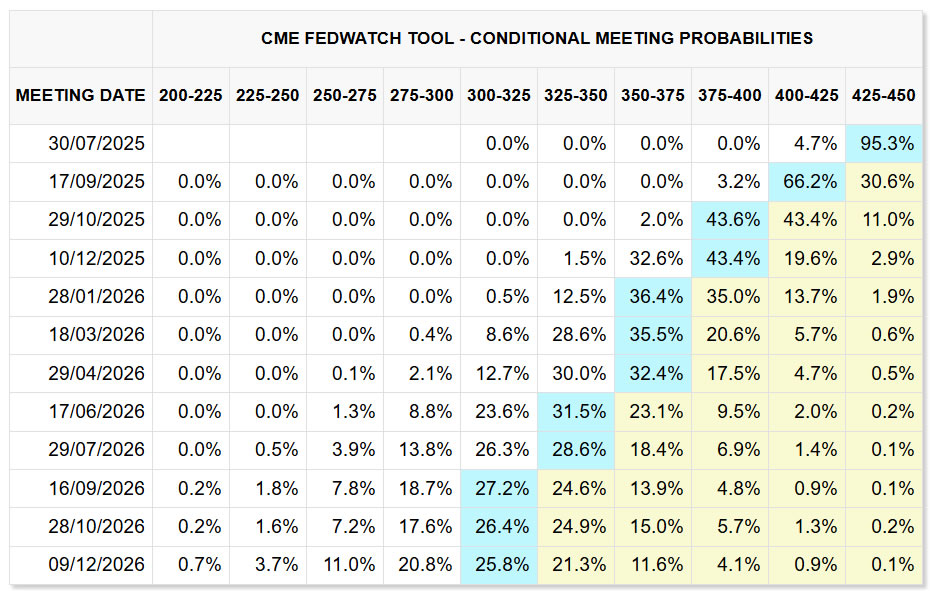

The latest data flow confirmed the Fed’s baseline — the economy is solid, but not overheating, and there’s no urgency to cut rates in July. The solid NFP report gave Fed Chair room to remain patient. While inflation risks from tariffs persist, the resilient labor market buys the Fed time.

Still, while a July cut is off the table, the shift in outlook has been subtle. September cut odds slipped back to 70% from 91% last week. Markets now see less than a 35% chance of three total cuts this year. While the easing cycle is intact, its pace appears slower.

Atlanta Fed President Raphael Bostic offered a longer-term view. He warned that the impact of trade and fiscal changes won’t be immediate, but rather unfold over a year or more. That could keep inflation elevated for longer than textbook models assume.

Bostic’s view supports a cautious Fed. If the inflation path is flatter but stickier, interest rates may need to stay higher for longer. That means even a resilient economy could coexist with slow policy adjustments — a Goldilocks scenario for risk assets, but less helpful for Dollar.

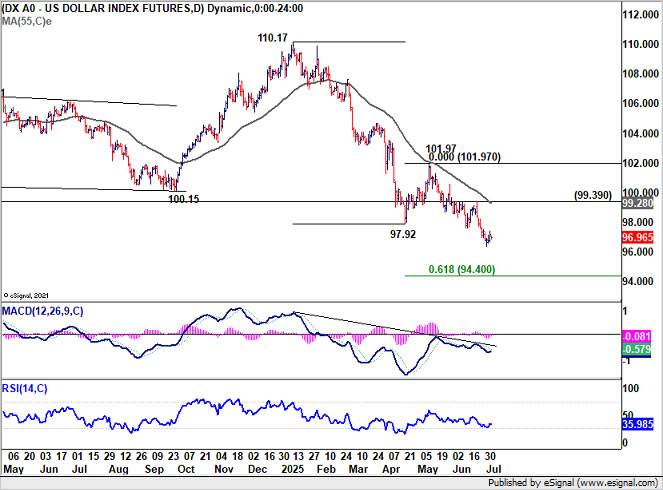

Technically, the most pressing question is whether Dollar Index could draw enough support from long term channel (now at around 96) to complete the decline from 114.77 (2022 high). Strong rebound from current level will keep such decline corrective, and keep the up trend from 70.67 (2008 low) intact. However, sustained break of the channel support will argue that whole up trend has completed, and deeper medium term fall would be seen to 61.8% retracement at 87.52, even still as a corrective move.

For the near term, Dollar Index’s decline slowed a little bit, but there is no clear momentum for a bounce. Near term outlook will continue to stay bearish as long as 99.39 resistance holds. Next target is 61.8% projection of 110.17 to 97.92 from 101.97 at 94.40.

Franc Finds Relief in Inflation Data, Sterling Weakens on UK Political Risks

GBP/CHF was last week’s biggest mover, falling -1.12% as a mix of renewed UK political risk and strengthening Swiss Franc pushed the cross lower. While the Swiss currency’s broad-based gains drove some of the move, domestic issues within the UK also added pressure to Sterling.

On the Swiss side, inflation data surprised slightly to the upside, with CPI rebounding to 0.1% yoy in June. This offered SNB some breathing room in its battle against deflationary pressures and boosted confidence that the May dip into negative territory was transitory. While inflation remains subdued, the data SNB more reason to pause rather than proceed with another cut in September.

With policy rates already at 0%, further easing by the SNB would require stronger justification. Ongoing Franc strength still poses downside risks to inflation, but barring further persistent deterioration in price pressures, the central bank might stay put for now.

In the UK, political drama around Chancellor Rachel Reeves and the Labour government’s policy U-turns have reignited fears of fiscal instability. The government’s retreat from welfare reform plans erased anticipated savings, raising doubts over its fiscal roadmap. Gilt yields spiked and Sterling came under renewed pressure, drawing comparisons to the 2022 Truss-led market meltdown.

Speculation of a cabinet reshuffle—and whether Reeves herself might be replaced—only deepens investor unease. Traders will be watching closely for any concrete developments, especially before the summer recess.

Technically, GBP/CHF’s extended, accelerated decline indicates that rebound from 1.0610 should have completed at 1.1204 already. Deeper fall is expected as long as 1.0930 support turned resistance holds, to retest 1.0610 low first.

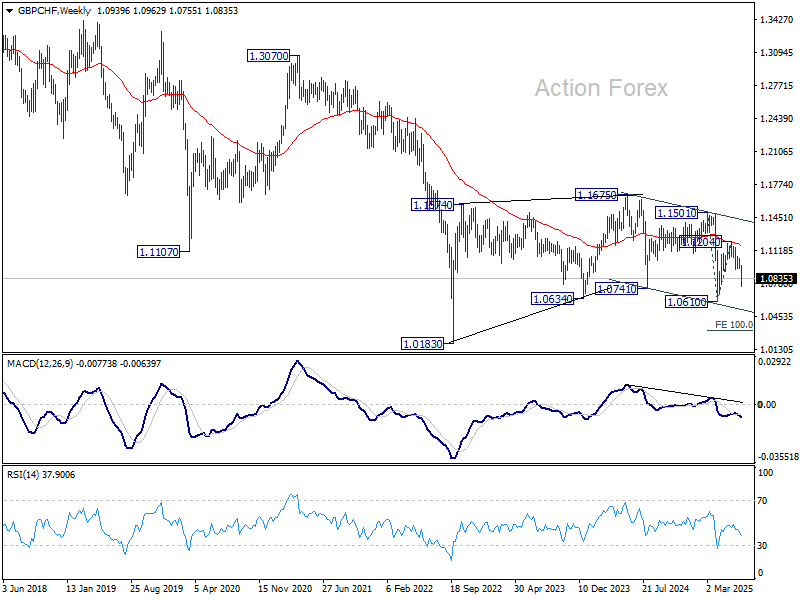

In the bigger picture, prior rejection by 55 W EMA is a medium term bearish sign. Down trend from 1.1675 (2024 high) is likely still in progress. Break of 1.0610 will target 100% projection of 1.1501 to 1.0610 from 1.1204 at 1.0313.

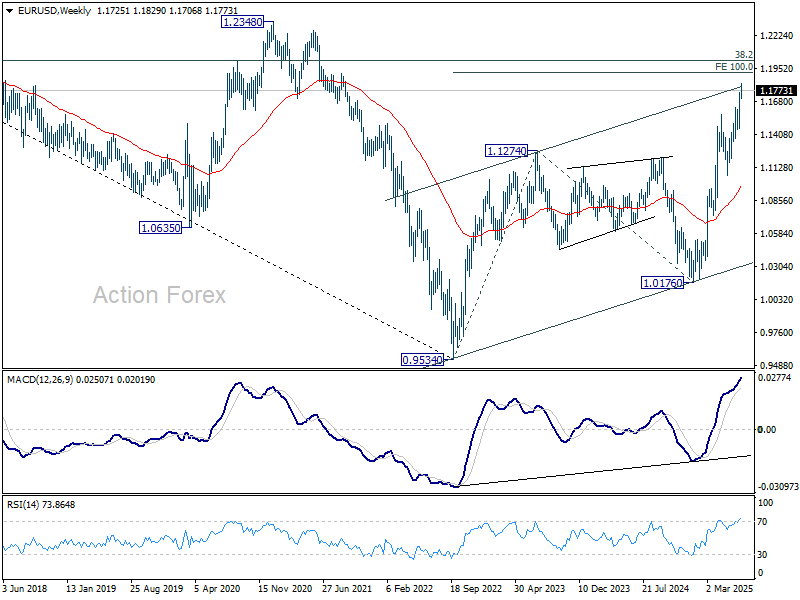

EUR/USD Weekly Outlook

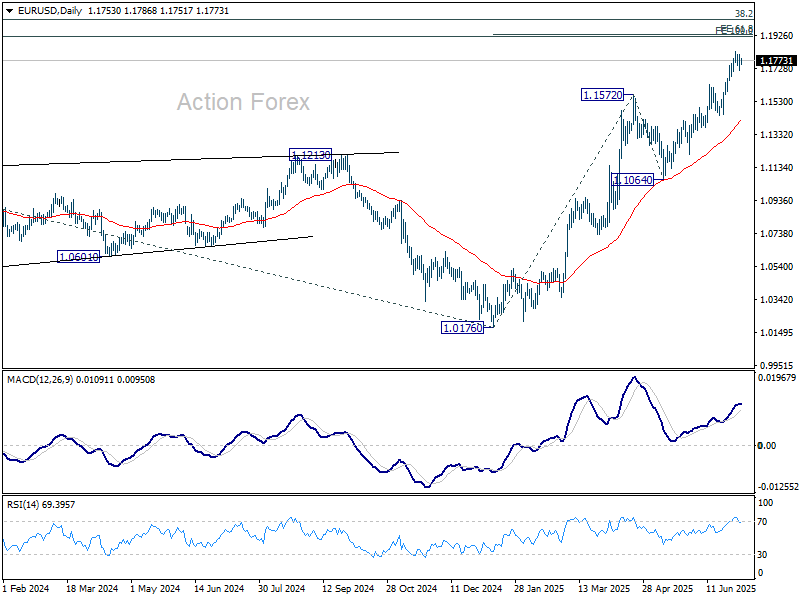

EUR/USD edged higher to 1.1829 last week but turned sideway since then. Initial bias stays neutral this week for more consolidations first. But downside should be contained by 1.1630 resistance turned support to bring rebound. Firm break of 1.1829 will resume the rise from 1.0176 and target 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 1.1604 support holds.

In the long term picture, a long term bottom was in place already at 0.9534, on bullish convergence condition in M MACD. Further rise should be seen to 38.2% retracement of 1.6039 to 0.9534 at 1.2019. Rejection by 1.2019 will keep the price actions from 0.9534 as a corrective pattern. But sustained break of 1.2019 will suggest long term bullish trend reversal, and target 61.8% retracement at 1.3554.

{kind=link}