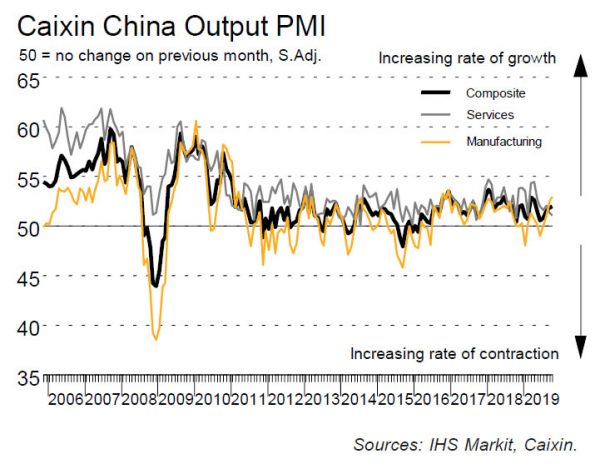

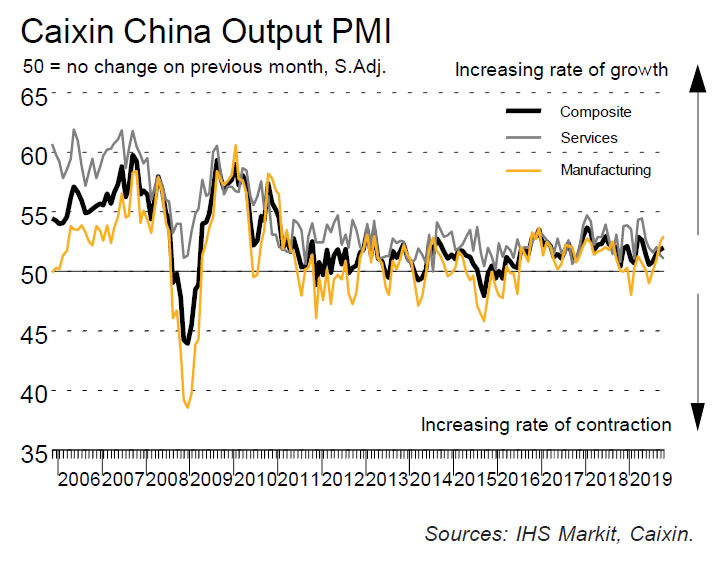

China Caixin PMI Services dropped to 51.1 in October, down from 51.3 and missed expectation of 52.8. PMI Composite Index edged up from 51.9 to 52.0, best reading since April. Markit noted that solid rate of manufacturing output growth contrasts with only marginal rise in services activity. Composite employment falls fro the first time in three months. Outstanding business at was at the fastest expansion since March 2011.

Commenting on the China General Services PMI™ data, Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said:

“The Caixin China General Services Business Activity Index dipped to 51.1 in October from 51.3 in the previous month, marking the slowest expansion in eight months amid subdued market conditions.

1) Demand across the services sector grew at a reduced pace, with the gauge for new business falling to the lowest level since February. The measure for new export business picked up slightly.

2) While the job market expanded at a weaker clip, with the employment gauge falling from the previous month’s recent high, the measure for outstanding business rose further into expansionary territory. This implied a mismatch between labor supply and demand.

3) Both gauges for input costs and prices charged by service providers edged down, but they remained in positive territory, reflecting relatively high pressure on costs, including those of workers, raw materials and fuel.

4) The measure for business expectations dropped to the lowest point in 15 months, indicating depressed business confidence.

“The Caixin China Composite Output Index inched up to 52 in October from 51.9 in the month before, amid an improvement in manufacturing, but a softer service sector performance. The employment gauge dipped into contractionary territory, indicating renewed pressure on the labor market, which was likely due mainly to structural unemployment. The measure for backlogs of work climbed to the highest level since early 2011, highlighting bottlenecks in production capacity and inventories due to weak business confidence.

“China’s economy continued to recover in general in October, thanks chiefly to the performance of the manufacturing sector. Domestic and foreign demand both improved. However, business confidence remained weak, constraining the release of production capacity. Structural unemployment and rising raw material costs remained issues. The foundation for economic growth to stabilize still needs to be consolidated.”

Full release here.

Australia retail sales rose only 0.1% mom in May, dragged by Victoria lockdown

Australia retail sales rose 0.1% mom in May, well below expectation of 0.7% mom. Comparing to a year ago, sales rose 7.4% yoy.

Ben James, Director of Quarterly Economy Wide Surveys, said: “There were mixed results across the industries and states and territories, with COVID-19 restrictions in Victoria impacting the May result. Victoria fell 1.5 per cent as the state entered its fourth lockdown on May 28 with trade restricted for physical stores.”

Full release here.