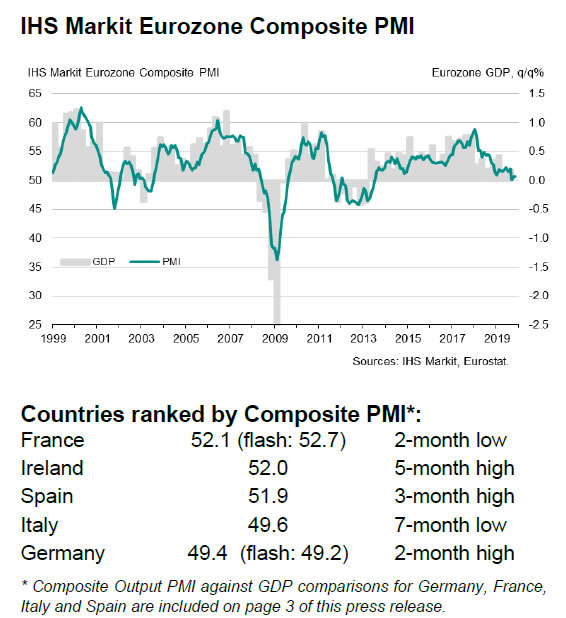

Eurozone PMI Services was finalized at 51.9 in November, down from October’s 52.2. PMI Composite was finalized at 50.6, unchanged from last month’s reading. Looking at some member states, Germany PMI Composite was finalized at 49.4, hitting a 2-month high but stayed below 50. Italy PMI Composite dropped to 49.6, 7-month low. France PMI Composite dipped to 2-month low of 52.1 but stayed comfortably above 50.

Chris Williamson, Chief Business Economist at IHS Markit said:

“The final eurozone PMI for November came in slightly ahead of the earlier flash estimate but still indicates a near-stagnant economy. The survey data are indicating GDP growth of just 0.1% in the fourth quarter, with manufacturing continuing to act as a major drag. Worryingly, the service sector is also on course for its weakest quarterly expansion for five years, hinting strongly that the slowdown continues to spread.

“New orders have not shown any growth since August, underscoring the recent weakness of demand, with sharply declining orders for manufactured goods accompanied by substantially weaker gains of new business into the service sector. Expectations are also among the lowest since the tail end of the sovereign debt crisis in 2013, as firms worry about trade wars, Brexit and slowing economic growth both at home and globally.

“The near-stalling of the economy has been accompanied by some of the weakest price pressures we’ve seen in recent years, which threatens to keep inflation well below the ECB’s target in coming months and adds to the likelihood of further policy stimulus early next year.”

Full release here.

Dollar index’s medium term outlook depends on non-farm payrolls today

US Non-Farm Payrolls report will be the major focus today. Markets are expecting 183k job growth in November. Unemployment rate is expected to be unchanged at 3.6%. Average hourly earnings growth is expected to pick up to 0.3% mom. Dollar dropped sharply this week as poor ISMs pointed to weaker outlook ahead, and revived speculation of Fed cut next year. A strong set of NFP data today is needed to reverse the greenback’s fortune. Otherwise, selloff might accelerate further.

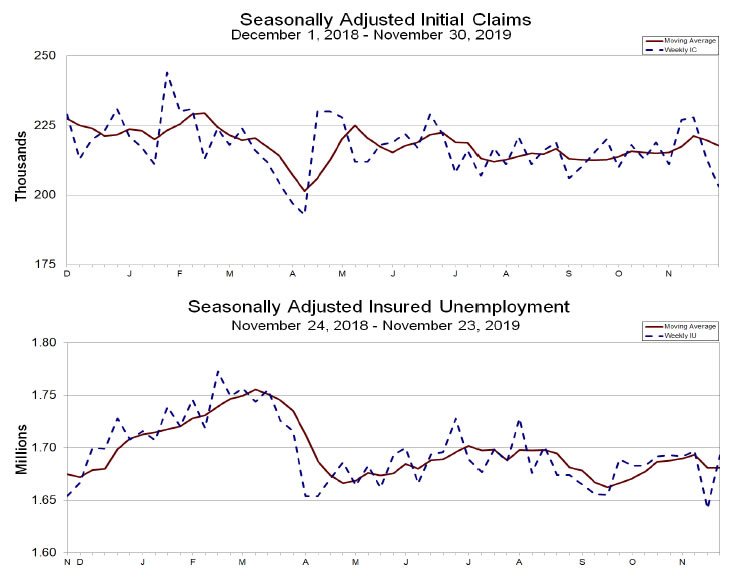

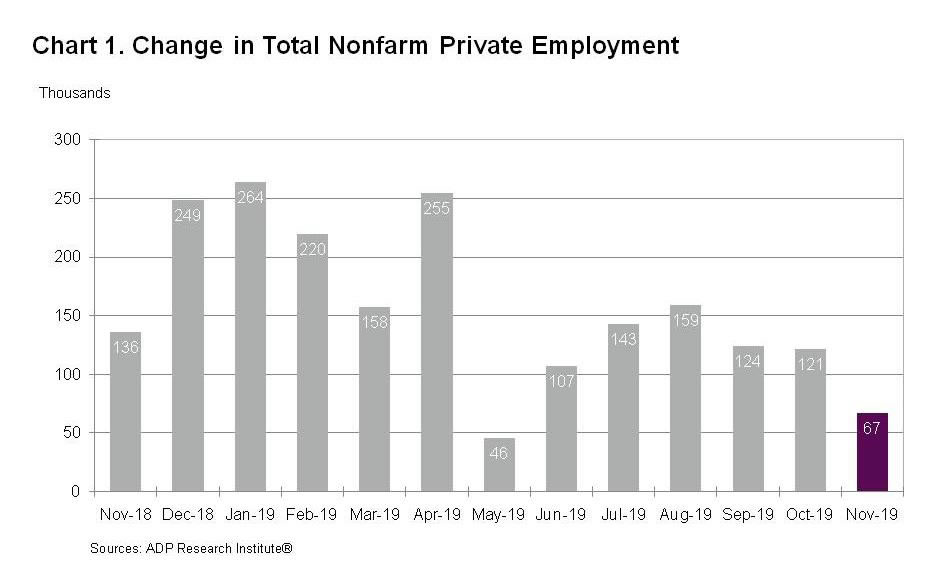

Other job related data released have been mixed to slightly negative. ISM manufacturing employment dropped from 47.7 to 46.6, suggesting deeper contraction in manufacturing jobs. ISM services employment rose to 55.5, up from 53.7. ADP private sector jobs grew just 67k. The details were also in-line with ISMs’, with goods-producing jobs contracted -18k. Service-providing jobs rose 85k. Four-week moving average of initial claims rose 3k to 217.75k.

Current development now raised the chance that Dollar index’s recovery from 97.10 was only a corrective rise, and has completed at 98.39. Next focus will be 97.10 support. Break there will also have 55 week EMA firmly taken out. In that case, a medium term should be confirmed at 99.66. And, a medium term correction should at least be started towards 38.2% retracement of 88.30 to 99.66 at 95.32.