Sterling is under broadly based selling pressure today as UK Prime Minister Theresa May called off tomorrow’s Brexit parliamentary vote. She conceded that her Brexit deal would be defeated by a wide margin and pledged to go back to EU for changes on the Irish border backstop. Kiwi is so far very resilient and seems not even bothered with US stocks selloff. For now, GBP/NZD is the top mover of today.

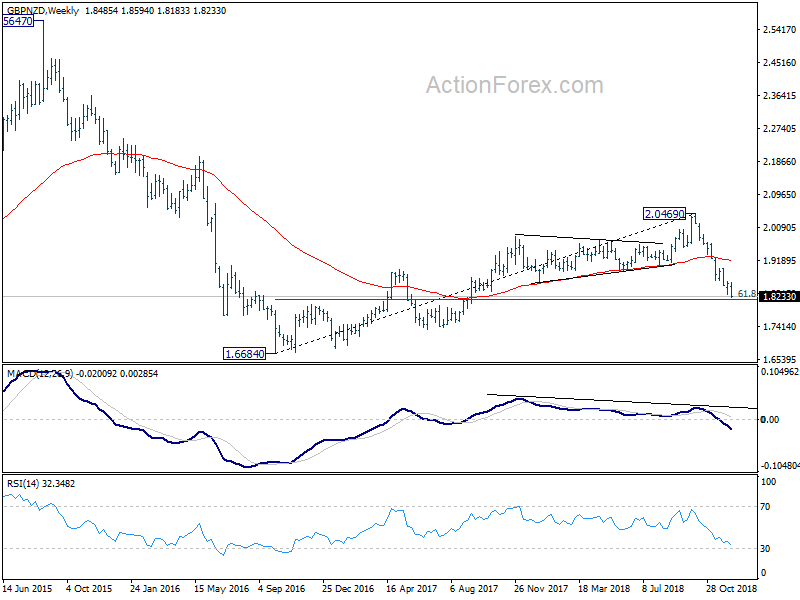

GBP/NZD’s development is inline with our bearish view as discussed here. The decline from 2.0469 resumed today and reached as low as 1.8183. Based on current downside acceleration, 61.8% retracement of 1.6684 to 2.0469 at 1.8130 will likely be taken out. And in any case, break of 1.8634 resistance is needed to confirm short term bottoming. Otherwise, outlook will remain bearish even in case of recovery.

Also, in our view, the medium term corrective rise from 1.6684 (2016 low) should have completed at 2.0469. Based on current downside momentum, fall from 2.0469 is likely resuming the down trend from 2.5647 (2015 high). Reaction to above mentioned 1.8130 fibonacci level will reveal the chance of this bearish case. Decisive, firm break of 1.8130 will at least bring retest of 1.6684 low.

DOW closed up 0.14% after 619pt swing, yield curve flattens further

US stocks staged a strong reversal overnight again. DOW initially dropped to as low as 23881.47 but closed up 0.14% t0 24423.26. The daily range was as large as 619 pts. S&P 500 dropped to 2583.23 but closed up 0.18% at 2637.72. NASDAQ was indeed the star performer, dipping to 6878.98 but closed up 0.74% at 7020.52. Tech stocks are seen as saving markets with Apple gained 0.66%, Qualcomm gained 2.23%, Facebook gained 3.22%.

Treasury yield curve continued to flatten with 5-year yield up 0.13 to 2.709. 10-year yield closed up 0.006 at 2.856. 30-year yield dropped -0.014 to 3.129. Yield curve remains inverted between 3-year (2.738) and 5-year (2.709).

In the currency markets, Sterling remains the weakest one for the week as UK Prime Minister Theresa May conceded and called off Tuesday’s Brexit parliamentary vote. Canadian Dollar is the second weakest. New Zealand Dollar, Australian Dollar and Swiss Franc are the strongest ones.

For today, Dollar turns softer, but Canadian stays weak. Aussie is staying firm for now, while Yen is trying to rally.