Risk aversions receded much as markets, in the end, responded rather positively to news of trade talks between the US and China. For now, it seems both countries will hold fire first, and come back to the table.

After struggling below 24000 handle for most of the session, DOW finally made up its mind in the last two hours and surged sharply. DOW ended the day up 669.40 pts or 2.84% at 2420.60. S&P 500 gained 70.29 pts or 2.72% to close at 2658.55. NASDAQ also rose 227.87 pts, or 3.26% to 7220.54.

Still, for now, DOW is limited below 24453.14 minor resistance and thus, there is no change in the near term direction yet. It’s still more likely to revisit 23360.29 support then not.

Asian markets follow with Nikkei trading up over 1.6% at the time of writing. Hong Kong HSI is up 0.9%.

Asian markets follow with Nikkei trading up over 1.6% at the time of writing. Hong Kong HSI is up 0.9%.

From D heatmap, JPY is extending this week’s fall in Asian session while Canadian Dollar is picking up some steam.

The W heatmap shows JPY as the weakest one, consistent with the daily developments. But holding above last week’s low against all but GBP only. Euro and GBP are the strongest ones for the week so far.

The W heatmap shows JPY as the weakest one, consistent with the daily developments. But holding above last week’s low against all but GBP only. Euro and GBP are the strongest ones for the week so far.

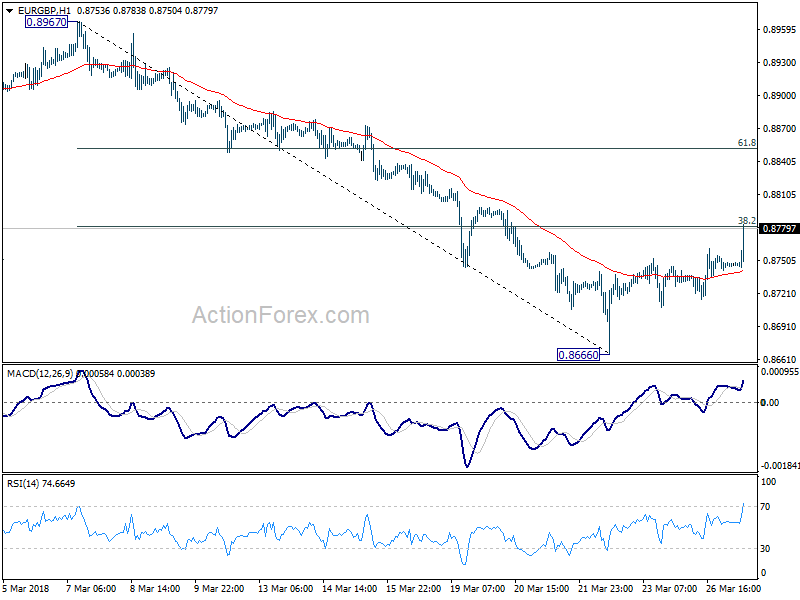

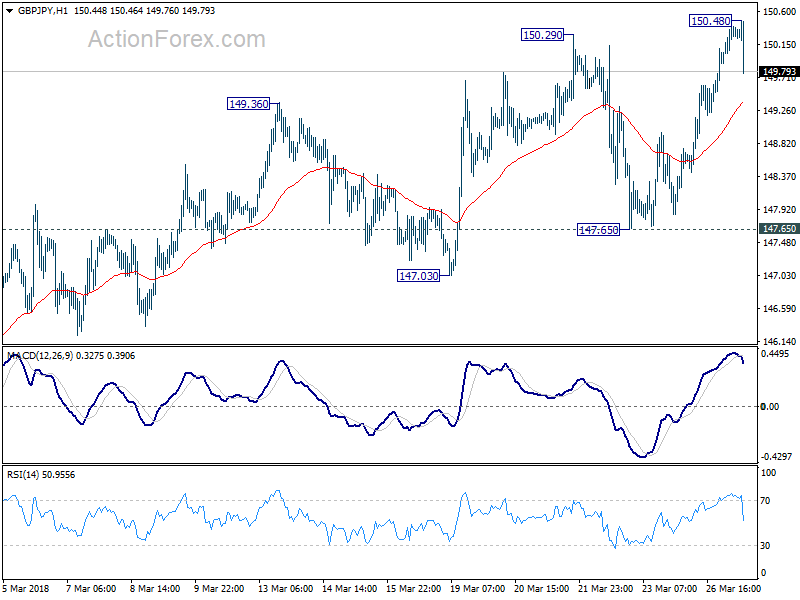

Also, note that EUR/JPY is held well below 132.40 resistance. GBP/JPY also stays below 150.92 resistance. Current rebound in JPY is more seen as a corrective move. The picture suggests that intraday or swings traders could ride on improved sentiments to sell JPY for quick profits. But for position traders, it could be an opportunity to buy JPY once the rebound loses steam.

Also, note that EUR/JPY is held well below 132.40 resistance. GBP/JPY also stays below 150.92 resistance. Current rebound in JPY is more seen as a corrective move. The picture suggests that intraday or swings traders could ride on improved sentiments to sell JPY for quick profits. But for position traders, it could be an opportunity to buy JPY once the rebound loses steam.

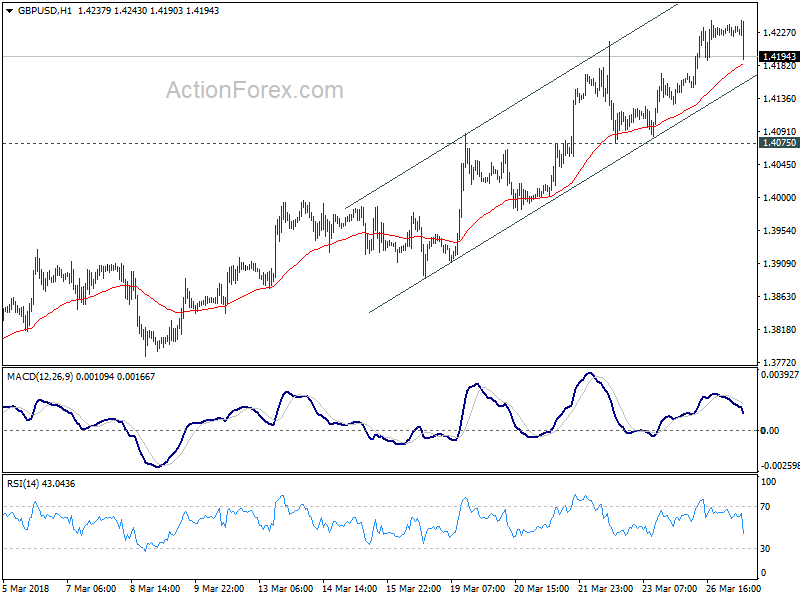

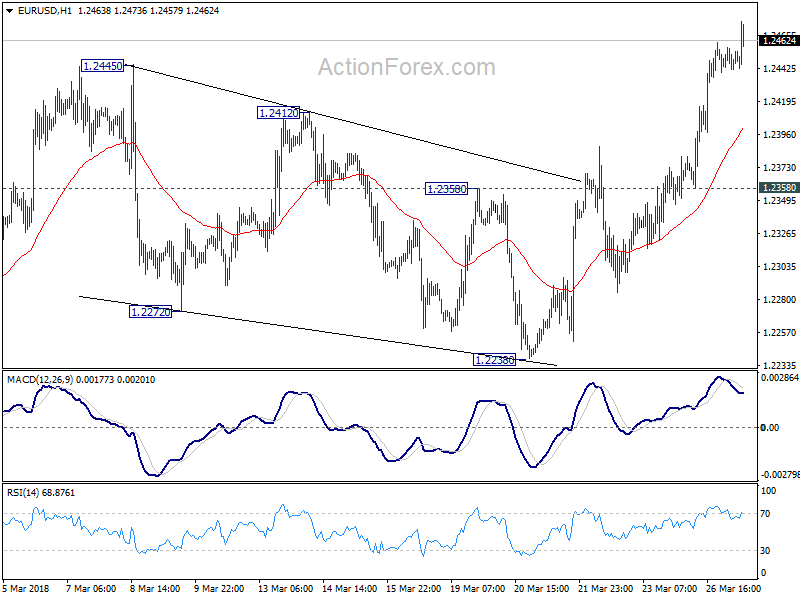

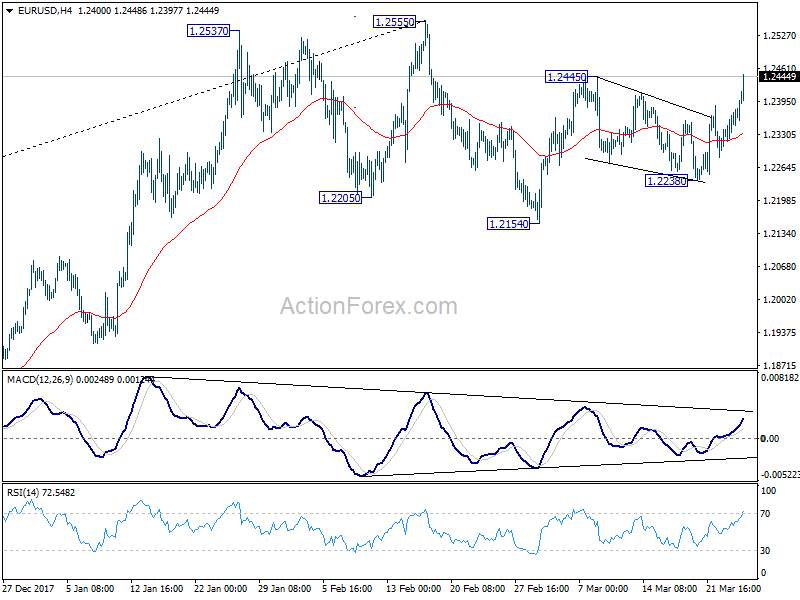

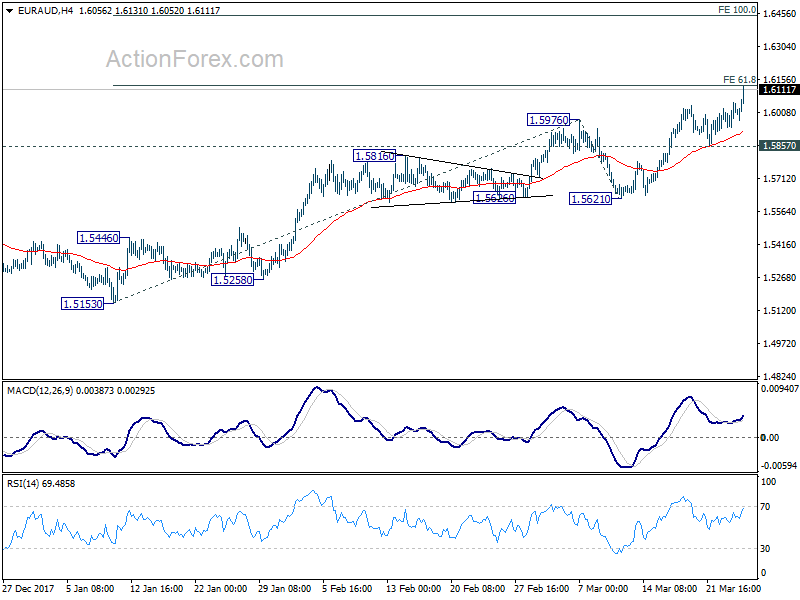

Euro stays strongest after jitters, EURAUD with solid upside bias

After some jitters yesterday, EUR remains the strongest major currency for the week as seen in W heatmap. Strength is apparent against USD, GBP and AUD. Meanwhile, JPY is trading as the weakest, followed closely by USD, CHF and AUD.

An intraday strategy could be buying at PP at 1.6120 with a stop below S1 at 1.6081.