Trump tweeted early in the morning:

“Received message last night from XI JINPING of China that his meeting with KIM JONG UN went very well and that KIM looks forward to his meeting with me. In the meantime, and unfortunately, maximum sanctions and pressure must be maintained at all cost!”

Recall earlier today, China’s official news agency Xinhua reported North Korean Leader Kim Jong-un saying that “the issue of denuclearization of the Korean Peninsula can be resolved, if South Korea and the United States respond to our efforts with goodwill, create an atmosphere of peace and stability while taking progressive and synchronous measures for the realization of peace.”

Now, does Kim feel that “maximum sanctions and pressure must be maintained at all cost” is something that create peacful and stable atmosphere?

Or, does Trump’s “at all cost” mean maintianing maximum pressure even though it will turn North Korea away? Or he actually believes what he said is responding to North Korea with “good will”?

Probably, both of them need to go back to school to learn what to say what one means exactly.

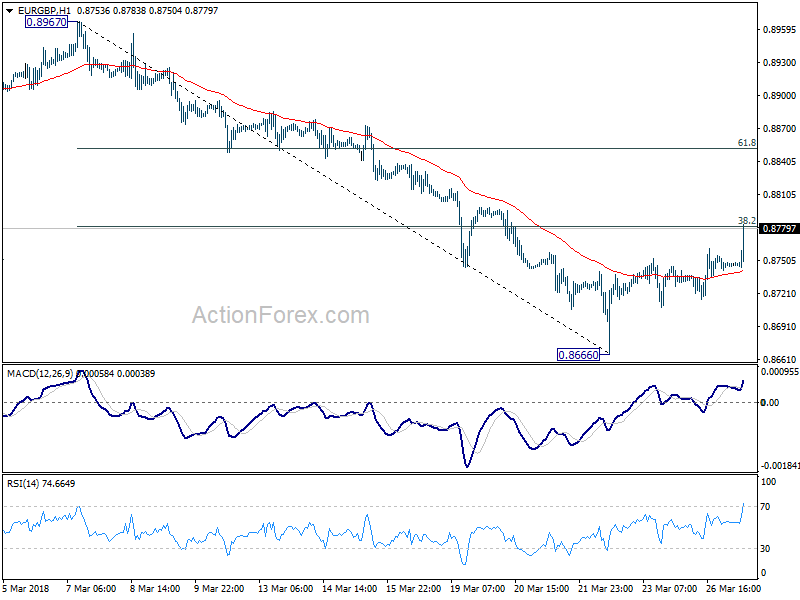

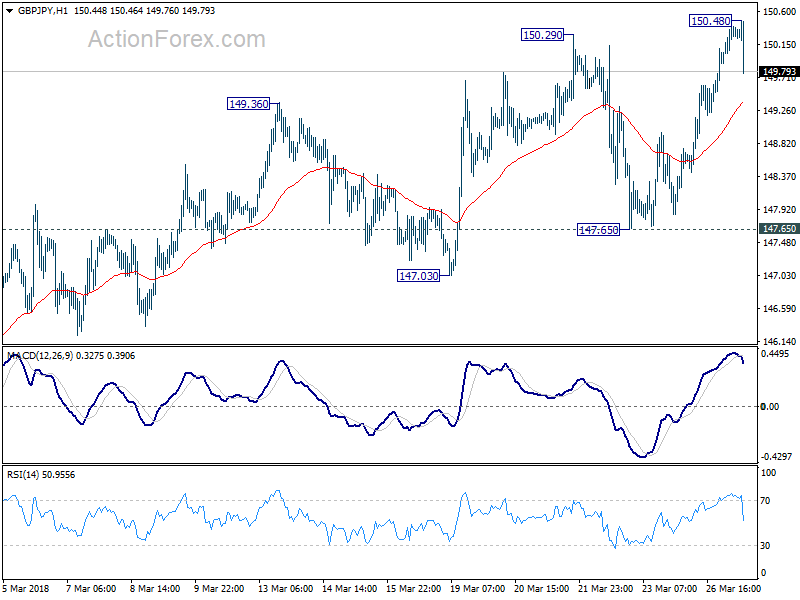

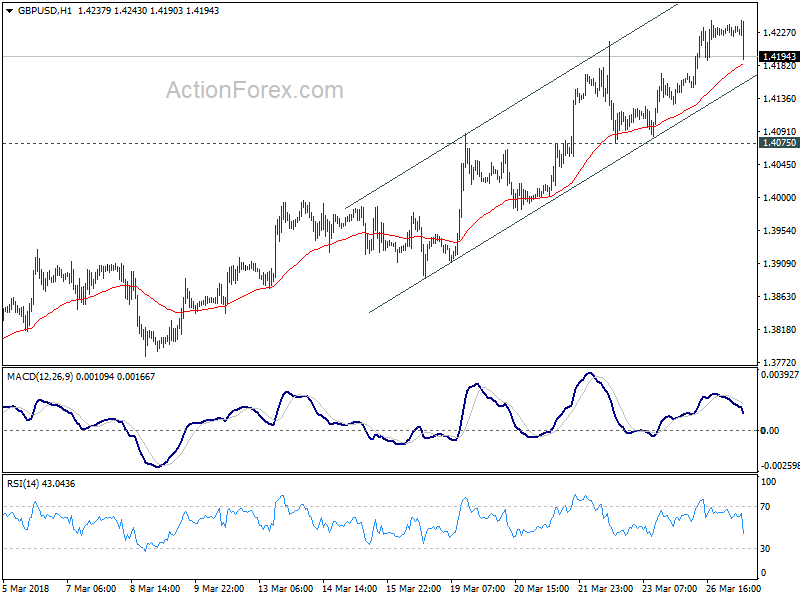

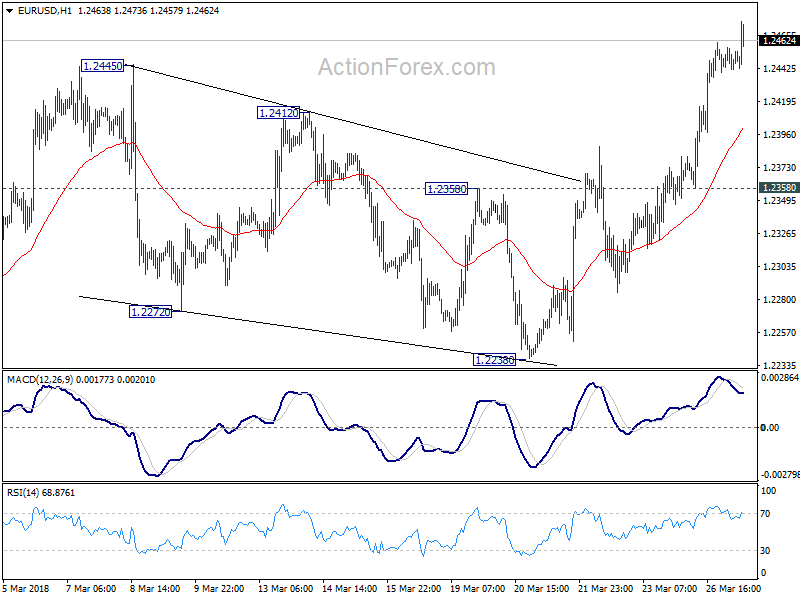

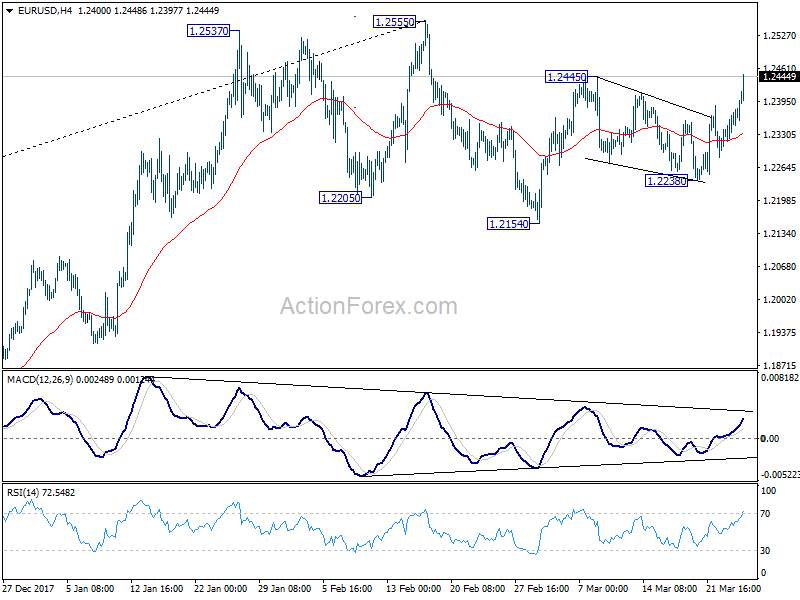

JPY and CHF lower as stocks rebound in premarket, EUR/CHF and GBP/CHF surge

US stocks futures reverse earlier loss and point to a higher open. The move was triggered by news that Facebook is going to streamline privacy settings. Facebook shares trade more than 1% higher in premarket. The development triggers intensified selling in JPY and CHF. Both are in deep red in 4H heatmap.

On the other hand, developments in CHF crosses look more promising. EUR/CHF is on track for a test on 1.1832 resistance.

GBP/CHF is even close to equivalent resistance at 1.3491.