Trade figures will dominate next week’s calendar with a number of nations publishing monthly data, though they’re unlikely to attract as many headlines as US protectionism as trade risks appear to be on the rise again. The Australian dollar will be in focus for much of the week as the Reserve Bank of Australia holds a policy meeting and first quarter economic performance is examined. Canadian jobs numbers and GDP revisions in the Eurozone and Japan will also be watched, but it will be a quieter seven days for the UK and the US.

RBA meeting and GDP data pose a downside risk for the aussie

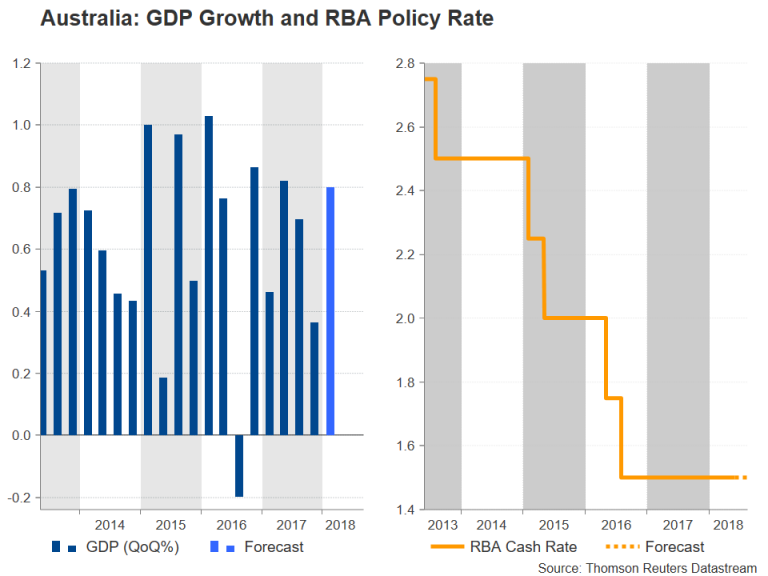

Disappointing quarterly capital expenditure figures out of Australia this week raised the prospect of GDP growth in the March quarter falling short of expectations when the data is released on Wednesday. Growth is forecast to have accelerated from 0.4% to 0.8% quarter-on-quarter in the three months to March. A GDP miss would only reaffirm expectations that the RBA will stay on hold for the foreseeable future. Ahead of the GDP release, there will be plenty of pointers for traders on what to expect as business inventories and net exports contribution for the first quarter are published on Monday and Tuesday, respectively. Other data to watch out of Australia are April retail sales on Monday and trade figures on Thursday.

Meanwhile, the RBA will almost certainly keep rates at a record low of 1.50% on Tuesday and maintain a neutral stance regardless of the data. However, if the growth numbers fail to meet expectations, the RBA could adopt more cautious language on the outlook for the rest of the year and that could trigger a sell off in the Australian dollar. After halting a 3-month downtrend in May, the aussie could head for fresh yearly lows versus the US dollar if the data fails to inspire traders.

There could be more volatility coming in the way of the aussie from Chinese data. China will publish trade numbers on Friday. Investors will be hoping for another healthy jump in annual export growth in May, following April’s 12.7% bounce, to appease concerns of moderating growth in the second quarter. Also out of China are producer and consumer prices on Saturday. China’s producer price index is seen by many as a good barometer for Chinese factory demand so an acceleration in the 12-month PPI rate would be positive for market sentiment.

Canadian jobs report looked at for July rate clues

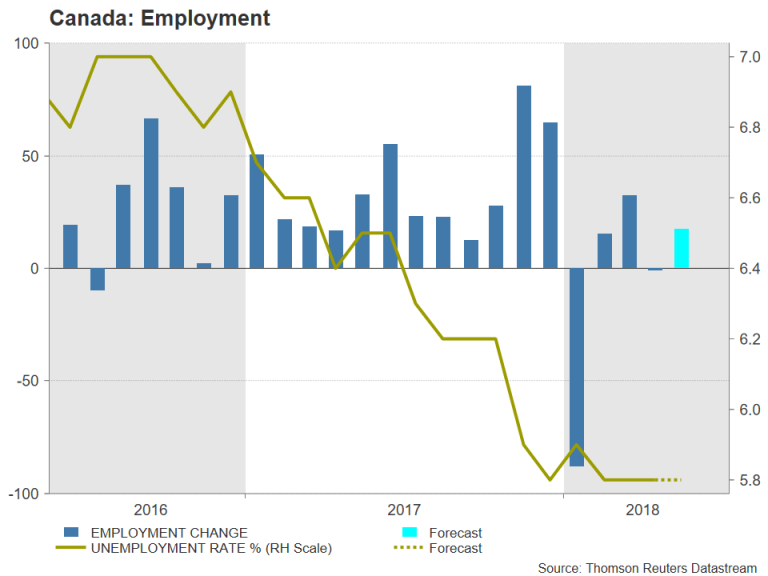

The Canadian dollar got a major boost after the Bank of Canada removed some of the more cautious language from its policy statement at the end of its meeting this week. Expectations of a July rate hike have shot up as a result and could firm further if incoming indicators surprise to the upside. The first batch of data are due on Wednesday, consisting of April building permits and trade figures as well as the Ivey PMI for May. The highlight for the loonie though will be Friday’s employment report. The Canadian economy is forecast to have added 17.4k jobs in May, while the unemployment rate is expected to stay at 5.8%. Solid job numbers on Friday would reinforce expectations of a July rate hike and could lift the loonie to below the C$1.29 level.

Japanese GDP could get revised up

The preliminary estimate of first quarter growth released earlier in May showed Japan ended two years of uninterrupted growth as the economy contracted by 0.6% on an annualized basis. The second estimate due on Friday is expected to see growth being revised up to 0.9%, extending the growth stretch to nine quarters. A marginal revision is unlikely to have a significant impact on monetary policy, however, and the Bank of Japan will probably be more interested in seeing a rebound in household spending and wages. Data on household spending in April is due on Tuesday, while the latest wage growth figures will be released on Wednesday. BoJ policymakers in Japan consider a pick-up in real wages to be an essential element in helping lift Japan out of a deflationary mindset.

UK PMIs and German industrial indicators to be the focus in Europe

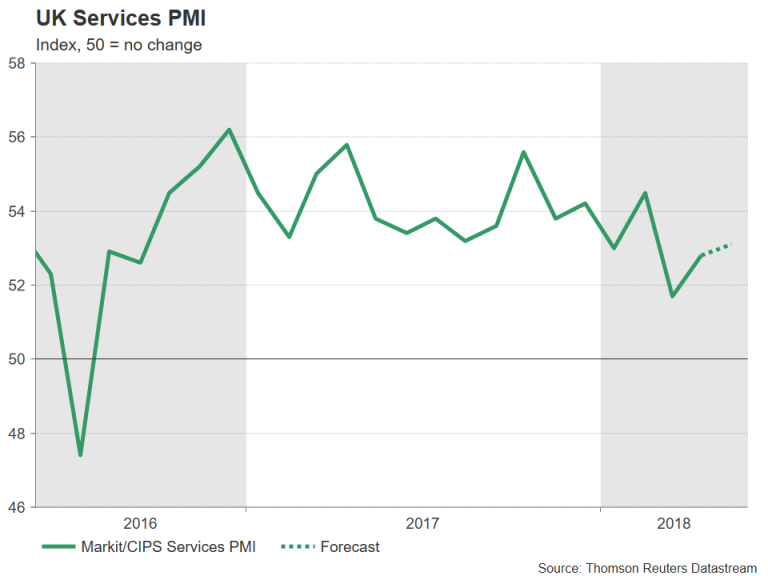

Major data releases will be sparse on the European calendar next week, with UK PMIs and a set of German indicators likely to attract the most attention. In the UK, the Markit/CIPS construction PMI is up first on Monday and the services PMI is due next on Tuesday. A further rebound in services activity in May, following April’s bounce from a 20-month low, could be the catalyst the pound needs to make a more convincing recovery from this week’s 6-months lows against the dollar. The Markit/CIPS services PMI is forecast to rise from 52.8 to 53.1 in May.

The Eurozone will also get PMI data, but having already seen the flash readings, next week’s final releases won’t generate much interest. More important will be the sentix index for June, due on Monday, retail sales for April on Tuesday and the third estimate of first quarter GDP growth on Thursday. No revision is expected to the 0.4% q/q figure of the prior estimate.

Investors will also be watching German figures on industrial orders, production and trade for evidence that the Eurozone’s largest economy is picking up speed in the second quarter. Industrial orders for April are due on Thursday, to be followed by industrial output and trade balance numbers on Friday. Industrial production jumped by 1% month-on-month in March after tumbling 1.7% in February. It is expected to recover further, by 0.2% m/m in April, which if confirmed, would point to a lacklustre start to the second quarter. Trade figures on Friday are unlikely to excite either. German exports are expected to have declined by 0.3% m/m in April. The euro would be at risk of reversing this week’s mini recovery if the data continue to surprise to the downside.

Quiet week for the US

Dollar traders shouldn’t expect to receive much direction from US indicators next week and Trump’s trade policy could once again become a bigger driver for the greenback, especially if the European Union and other countries that failed to get permanent exemption from the steel and aluminium tariffs proceed with announced retaliatory measures. In terms of data, it will be a relatively muted week, starting with April factory orders on Monday. The ISM non-manufacturing PMI on Tuesday will be the most important data to watch. The index measuring services activity is forecast to recover from April’s 4-month low, rising to 57.2 in May. A stronger reading could provide a further boost to the greenback, which managed to regain its positive footing against the Japanese yen after this week’s nonfarm payrolls beat. On Wednesday the trade balance for April will be the highlight. The US trade deficit is expected to widen to $50 billion in April, giving President Trump a stronger argument in his fight to cut the trade shortfall.