Here are the latest developments in global markets:

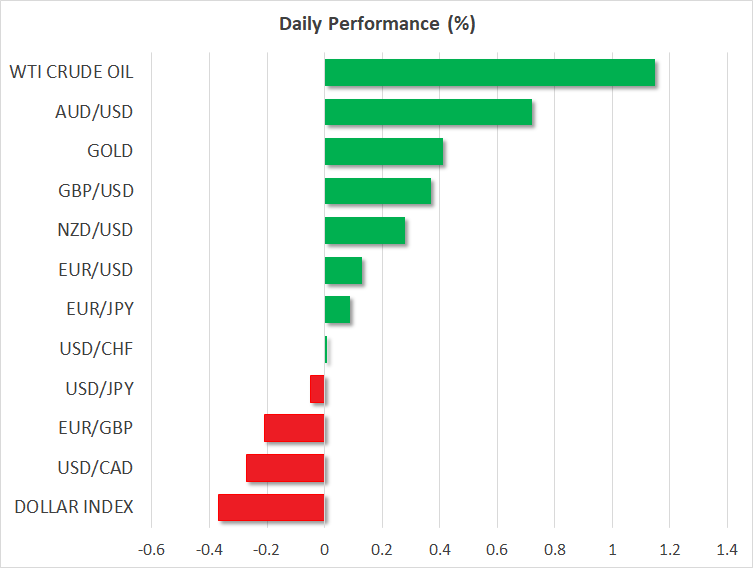

FOREX: Ahead of the Independence Day celebration in the US on Wednesday and the FOMC meeting minutes on Thursday, dollar/yen paused at 110.87 (-0.01%) early in the European session, while the dollar index which gauges the greenback’s strength against a basket of six major currencies was weaker at 94.67 (-0.37%) as the euro and the pound were attracting some interest. Euro/dollar fully recovered yesterday’s losses as the leading coalition parties in Germany managed on Monday to break the migration deadlock, calming concerns over Merkel’s political career and worries about the lifetime of the current coalition government. Eurozone data published early today indicated an unexpected improvement in PPI indicators, though in the retail sector sales came in surprisingly slightly weaker. Following the stats, euro/dollar continued to move upwards. Pound/dollar was also in a bullish mode, coming close to overpassing the 1.32 round level after the BoE member Michael Sanders, who was among the three policymakers who voted in favor of a rate increase at June’s meeting, messaged in an interview today that if the British economy evolves in line with his estimates, the BoE may raise interest rates faster than what financial markets are currently anticipating. Note that markets expect the BoE to hike rates once in the next twelve months. Besides the comments, the UK’s construction PMI for the month of June beat forecasts and reached the highest since December, boosting the pound even further. Speculation that the UK government has a new plan on how to handle customs – a thorny issue in the Brexit negotiations – was also supporting the market. At the Chequers summit on Friday, May will meet her cabinet to shape UK’s preferred economic relationship with the EU. Euro/pound changed hands lower at 0.8830 (-0.26%). In antipodean currencies, aussie/dollar and kiwi/dollar remained on the upside, with the former stretching up to 0.7393 (+0.74%) and the latter moving up to 0.6738 (+0.34%). The rebound in antipodeans early today came after China’s central bank talked up the yuan after it fell below the 6.7 psychological level raising suspicion the central bank could intervene in FX markets to support the currency. The central bank expressed that it will seek to keep the currency stable and at a reasonable level. Dollar/Swedish krona was among the worst performers losing 1.26% after Sweden’s central bank maintained borrowing costs steady but revised upwards its inflation forecasts for this year. Moreover, it reiterated that it would push up rates at the end of the year.

STOCKS: European stocks opened higher on Tuesday, underpinned by the political breakthrough in Germany. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were up by 1.00% and 1.14% respectively at 1150 GMT, with all sectors except energy being in the sea of green. The German DAX 30 gained 1.36%, the French CAC 40 climbed by 1.04%, while the Italian FTSE MIB and the Spanish IBEX 35 surged by 1.81% and 1.32% respectively. UK’s FTSE 100 climbed more modestly by 0.69% as the index was dragged down by a plunge in the shares of Glencore following the US Justice Department issuing a subpoena to the company for a money laundering investigation. In the US, futures tracking major indices such as S&P 500 and NASDAQ 100 were pointing to a positive open.

COMMODITIES: Oil prices continued to head north early in the European afternoon as Canada’s Syncrude oil sand facility which was hit by a power outage last month was said to remain shut during July, while military conflicts in Libya signaled further supply tightening. WTI crude and Brent were last seen higher at $74.78(+1.14%) and at $78.03 (+0.94%) respectively. In precious metals, gold bounced off 7-month lows to touch $1,248 (+0.50%).

Day Ahead: US durable goods, New Zealand Global dairy prices and Australia retail sales eyed

The economic calendar has few economic releases to deliver in the remainder of the day, which in the absence of any trade and political updates could spur positioning in the markets before Thursday’s FOMC meeting minutes and Friday’s non-farm payrolls come into view.

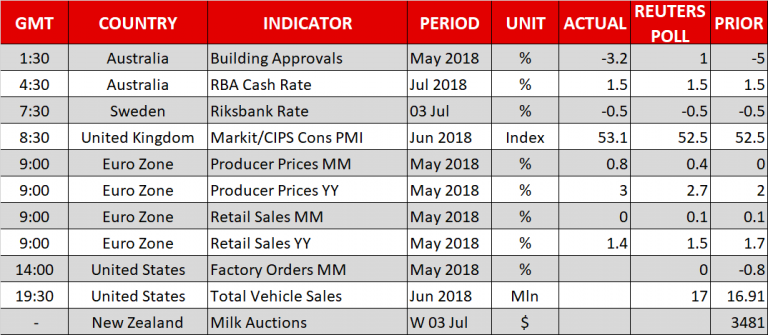

In the US, factory orders and total vehicle sales for May are scheduled for release at 1400 GMT and at 1930 GMT respectively. Factory orders are expected to show no change on a monthly basis in May after retreating by 0.8% in April, while the number of vehicles is projected to improve to 17 million, slightly up from 16.91 million seen earlier. The dollar could come under renewed selling pressure if the data disappoint.

In energy markets, investors will be waiting for the API weekly report to show changes in the US oil inventories at 2030 GMT for the week ending on June 25.

Kiwi pairs could face volatility as the outcome of the bi-weekly milk auction is made public later today; dairy products are New Zealand’s largest goods export earner. The relevant print lacks a specific time of release.

In terms of public appearances, ECB Chief Economist Peter Praet will give a speech at Gala Dinner hosted by the National Bank of Romania in Bucharest, Romania at 1600 GMT.

Trade tensions will be one of the major themes in markets before US tariffs on Chinese imported goods become effective on July 6. Also, the strong movement in the yuan is being monitored by officials in the Chinese central bank (PBOC).

Early tomorrow, Australia will see the release of retail sales numbers at 0130 GMT; aussie pairs will be eyed. Month-on-month, sales are expected to expand by 0.3% in May versus 0.4% the prior month. At the same time, the nation’s trade balance for the same month will be published as well, with analysts predicting the measure to come at 1,200M from 977M before.

A bit later at 0145 GMT, investors will be looking at China’s Caixin services PMI readings.

{kind=link}