Here are the latest developments in global markets:

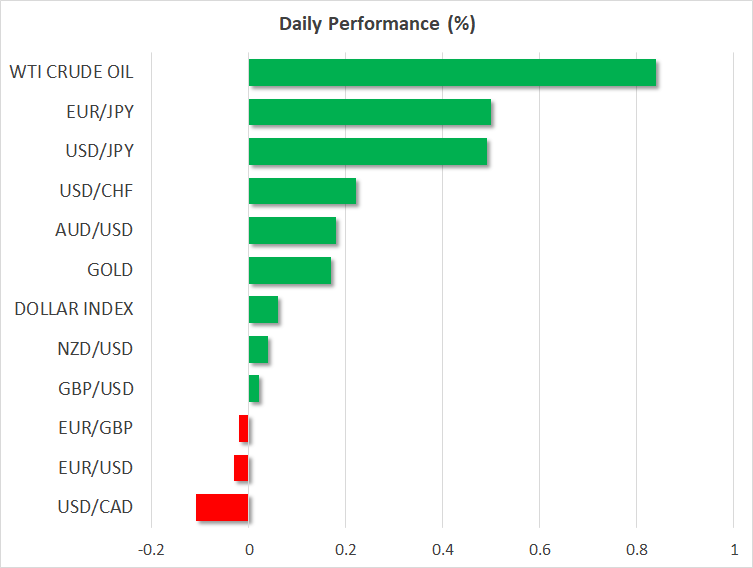

FOREX: Dollar/yen continued to advance during the European trading session on Thursday, rising by 0.49% in the day to touch a fresh seven-month high of 112.55, with the yen failing to draw any support from reports President Trump has threatened to withdraw the US from NATO. Meanwhile, euro/dollar was down marginally (-0.03%), ahead of the release of the ECB minutes from the June meeting at 1130 GMT, where investors will look for clues regarding the potential timing of a rate increase next year. Sterling/dollar is higher by 0.03%, as markets (and EU negotiators) await the release of the full 100-page White Paper on Brexit by the UK government. In the commodity-currencies space, dollar/loonie is down by 0.08%, giving back some of the gains it posted yesterday on the back of declining oil prices. Meanwhile, aussie/dollar and kiwi/dollar are up by 0.18% and 0.04% respectively, amid a general risk-on atmosphere. In EM, the Turkish lira briefly touched a fresh record-low of 4.97 against the dollar earlier, but subsequently rebounded.

STOCKS: European stocks were a sea of green at 1120 GMT, as the risk appetite seen during the Asian session earlier has spilled over into Europe as well. The only exception was the Spanish IBEX 35, which is down by a fractional 0.01%. Meanwhile, the pan-European STOXX 600 was up by 0.36%, while the blue-chip STOXX 50 advanced 0.52%. In the UK, the FTSE 100 climbed 0.65%, the German DAX 30 gained 0.26%, and the French CAC 40 rose 0.31%. US markets look set to follow suit, as futures tracking major indices like the S&P 500 are pointing to a notably higher open today.

COMMODITIES: In energy markets, oil prices were licking their wounds, rising somewhat today following a very sharp downfall yesterday – when WTI dropped by 5.0% and Brent by 6.9%. The losses came amid news that supply outages in Libya have been resolved, and that the nation will soon begin to ramp up its oil production and exports. Today, WTI is up by 0.87% at $70.81, and Brent by 1.53% at $74.20, both recovering partially. In precious metals, gold is higher by 0.18% at $1244 per ounce, while silver is up by 0.48% at $15.82.

Day ahead: US yearly CPI figures to rise further; Brexit White Paper in focus

The focus will switch from trade tariffs to inflation in the next few hours as investors will be interested to see whether CPI figures out of the US have the strength to push the rising dollar even higher.

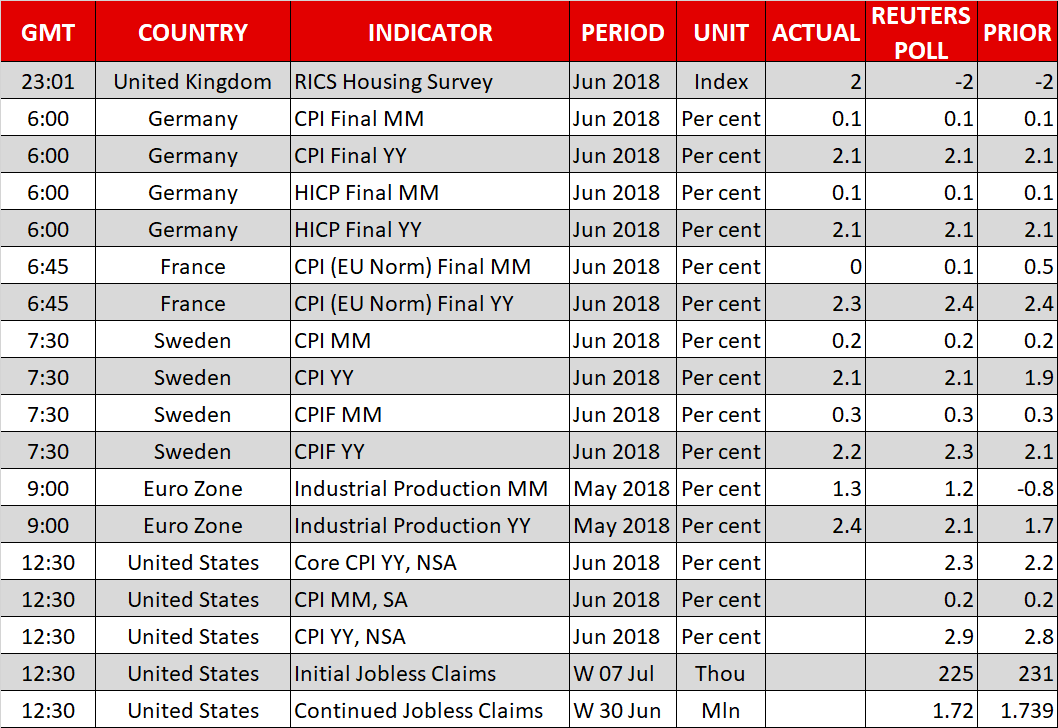

At 1230 GMT, the US Bureau of Labor Statistics is expected to show that US consumer prices have grown by 0.2% m/m in June – the same as in May –, while year-on-year the headline CPI gauge is anticipated to inch up by 0.1 percentage points to 2.9%. The core equivalent, which excludes food and energy, is also projected to edge up on a yearly basis, increasing to 2.3% from 2.2% in the preceding month. While the measure is not the Fed’s favorite – that is the core Personal Consumption Expenditure (PCE) index – CPI figures are used by policymakers to identify trends in inflation as well. Should the numbers beat forecasts, hinting that inflationary pressures in the US are heating up and therefore further rate hikes in the year could be comfortably applied, the greenback could hit fresh highs and even challenge the 113 handle against the yen. On the other hand, a miss in data could see the dollar reversing lower. Separately, any updates on trade tensions have the capacity to trigger moves in the market as well.

Initial jobless claims out of the US for the week ending July 6 will also come in light at the same time, though, the dollar typically shows little response to these data.

Meanwhile in the UK, headlines on the Brexit front will attract the most attention. May’s proposals on the UK’s future relationship with the EU, which were presented to UK ministers on Friday and forced the resignation of David Davis (UK’s Brexit negotiator) and Boris Johnson (UK’s foreign minister), will be explained in detail in a 100-page White Paper today, with scope to bring fresh volatility to the pound. Should the details reveal a “workable” and “realistic” UK plan that makes a “smoother Brexit” more realistic, then the pound could benefit. The opposite holds true as well.

In Brussels, the two-day NATO summit will conclude today but it seems that Trump’s continuing criticism of the group’s defensive spending plan and trade practices have tensed talks, calling unscheduled meetings. The US President will be also fly to the UK today to meet the British Prime Minister.

As for today’s public appearances, at 1100 GMT, a meeting between the US Secretary of State Mike Pompeo and EU Foreign Policy chief Federica Mogherini will attract some attention amid escalating global trade tensions. Later at 1415 GMT, Philadelphia Fed President Patrick Harker, a non-voting FOMC member on 2018, will be making comments at 1415 GMT.

In equities, Delta Air Lines will be releasing its quarterly results before today’s opening bell on Wall Street.

Early on Tuesday at 0445 GMT, Chinese trade stats for the month of June and more importantly China’s trade balance with the US will keep Asian traders busy.

{kind=link}