Here are the latest developments in global markets:

FOREX: The dollar continued gaining versus a basket of currencies on Wednesday after rising by a bit less than 0.5% the previous day. Upbeat comments on the US economy by Fed Chief Jerome Powell acted as the catalyst for the greenback’s advance, as well as fueling risk sentiment. In light of the risk-on mood, the yen retreated, with dollar/yen reaching a fresh six-month high of 113.07 earlier on the day.

STOCKS: The Dow, S&P 500 and Nasdaq Composite finished the day higher on Tuesday by 0.2%, 0.4% and 0.6% respectively – the latter posted a fresh all-time high – being helped by Powell’s optimism. Asian equities took their cue from the US, for the most part finishing in the green on Wednesday. Japan’s Nikkei 225 and Topix indices advanced by 0.4% and 0.35% correspondingly, while Hong Kong’s Hang Seng was down by 0.3% at 0629 GMT. Futures tracking major European benchmarks were broadly in the green, pointing to a higher open. Meanwhile, contracts on the Dow, S&P 500 and Nasdaq 100 were also trading higher, albeit only marginally so. In terms of corporate earnings: American Express, Alcoa, eBay, IBM and Morgan Stanley are some of the companies releasing quarterly results as the day unfolds; Morgan Stanley will be reporting before the opening bell on Wall Street, with all others releasing results after the market close.

COMMODITIES: WTI and Brent crude are trading lower by 0.7% and 0.6%, at $67.62 and $71.75 per barrel respectively. The two benchmarks are building on losses after the American Petroleum Institute (API) reported a surprise increase in US crude inventories on Tuesday. In the meantime, weekly EIA data on US crude stocks due at 1430 GMT may offer some short-term direction to oil prices during today’s trading. In precious metals, gold is down by 0.4% at $1,222.45 per ounce, not far above a one-year low hit earlier in the day. The yellow metal, being denominated in dollars, is suffering on the back of the US currency’s strength.

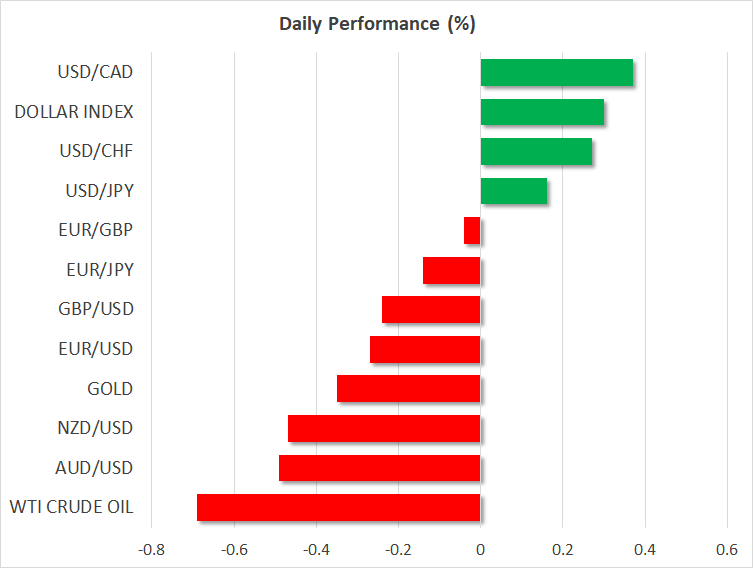

Major movers: Dollar advances helped by Powell, hits six-month high versus the yen

Federal Reserve Chairman Jerome Powell’s upbeat take on the outlook for the US economy fueled a rally in the US currency, while soothing to an extent those wary about the potential negative effects of a trade war. The dollar index is up by 0.25% on Wednesday, with dollar/yen not far below its highest since January 9 of 113.07. Moreover, it is no longer the case that the Japanese currency is trading in the green versus the US currency in 2018.

In the meantime, the euro and sterling are extending yesterday’s decline against the greenback, as Powell lent credence to those expecting the US central bank to remain on a path of rate normalization. The British currency, which also posted notable losses versus the euro on Tuesday, is also coming under pressure on the back of Brexit related uncertainty that is also casting doubts on PM Theresa May’s leadership. Later on Wednesday, the pound is expected to be sensitive to inflation figures which have the capacity to affect Bank of England policymakers’ judgement regarding the delivery of a rate hike during their early August meeting.

The commodity-linked loonie, aussie and the kiwi also fell victims to broad dollar strength. In particular, USDCAD touched a near three-week high of 1.3241 and AUDUSD recorded a two-week low of 0.7344 on Wednesday.

Day ahead: UK & EU report on inflation; Fed chief testifies before the House Financial Services Committee

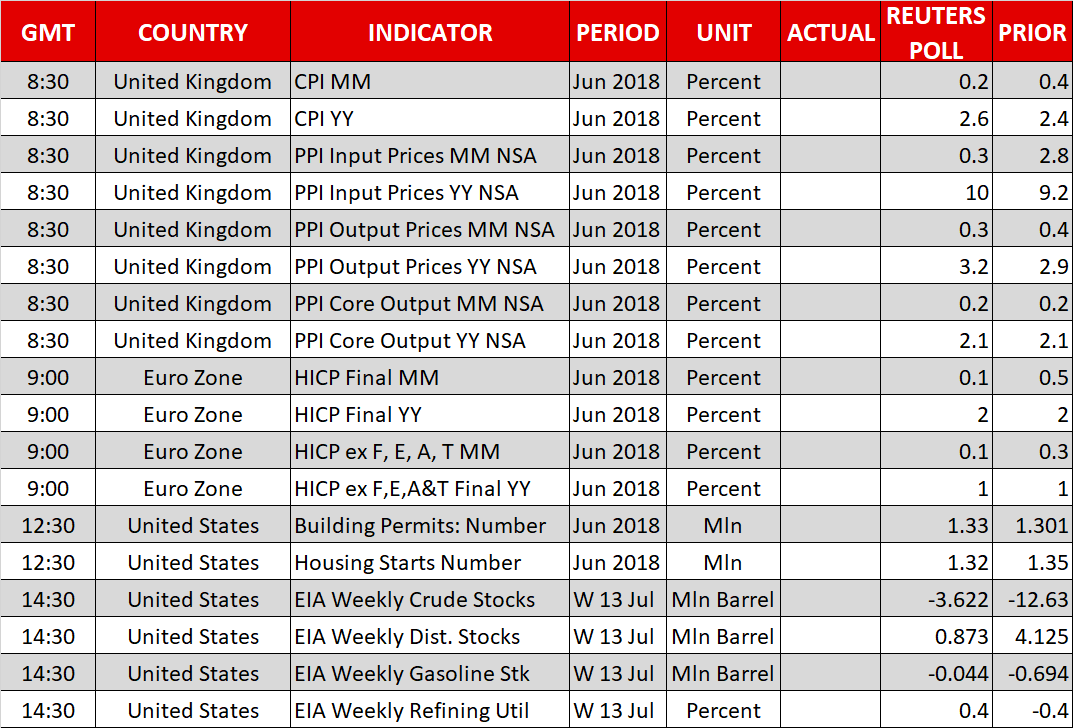

After a bearish trading session on Tuesday, sterling will be eyeing UK’s inflation numbers due today at 0830 GMT to potentially recover losses made on the back of political uncertainty stemming from disagreements within the Tory party over the nation’s Brexit strategy. Analysts expect the headline CPI to have risen faster in June, picking up by 2.6% y/y compared to a growth of 2.4% in May, while on a monthly basis the gauge is anticipated to weaken by 0.2 percentage points, growing by 0.2%. Should the numbers beat expectations, increasing chances for a rate hike by the Bank of England in August, sterling could start erasing Tuesday’s downfall. On the other hand, a miss in the data may see the currency turning more bearish, reaching fresh lows. Producer price and retail price data will also be made public at the same time.

At 0900 GMT, the Eurozone will see the release of June’s CPI figures as well, though these would be final estimates and unless the data deviate significantly from preliminary predictions the euro is not expected to react much. According to forecasts, the headline CPI (HICP, the measure that uses a common methodology across EU countries) is anticipated to come in line with previous estimates on a yearly basis, confirming a growth of 2.0% compared to 1.9% in May. The core measure of inflation which excludes food, energy, alcohol, and tobacco is also projected to match the preliminary release, expanding by 1.0% y/y.

Out of the US, June’s building permits and housing starts are due at 1230 GMT. The number of housing starts is projected to decline by 2.2% m/m after rising by 5.0% in May, to come close to a near 11-year high. Still, the focus will remain on the Fed Chief Jerome Powell and his semi-annual testimony on the economy and monetary policy in front of the House Financial Services Committee at 1400 GMT. Testifying before the Senate Banking Committee on Tuesday, Powell signaled that the US economy is strong enough to withstand further rate hikes this year and that trade uncertainties will probably not keep the Fed from proceeding accordingly. In the meantime, the Fed’s Beige Book gauging economic conditions in the twelve Federal districts in the US is due at 1800 GMT.

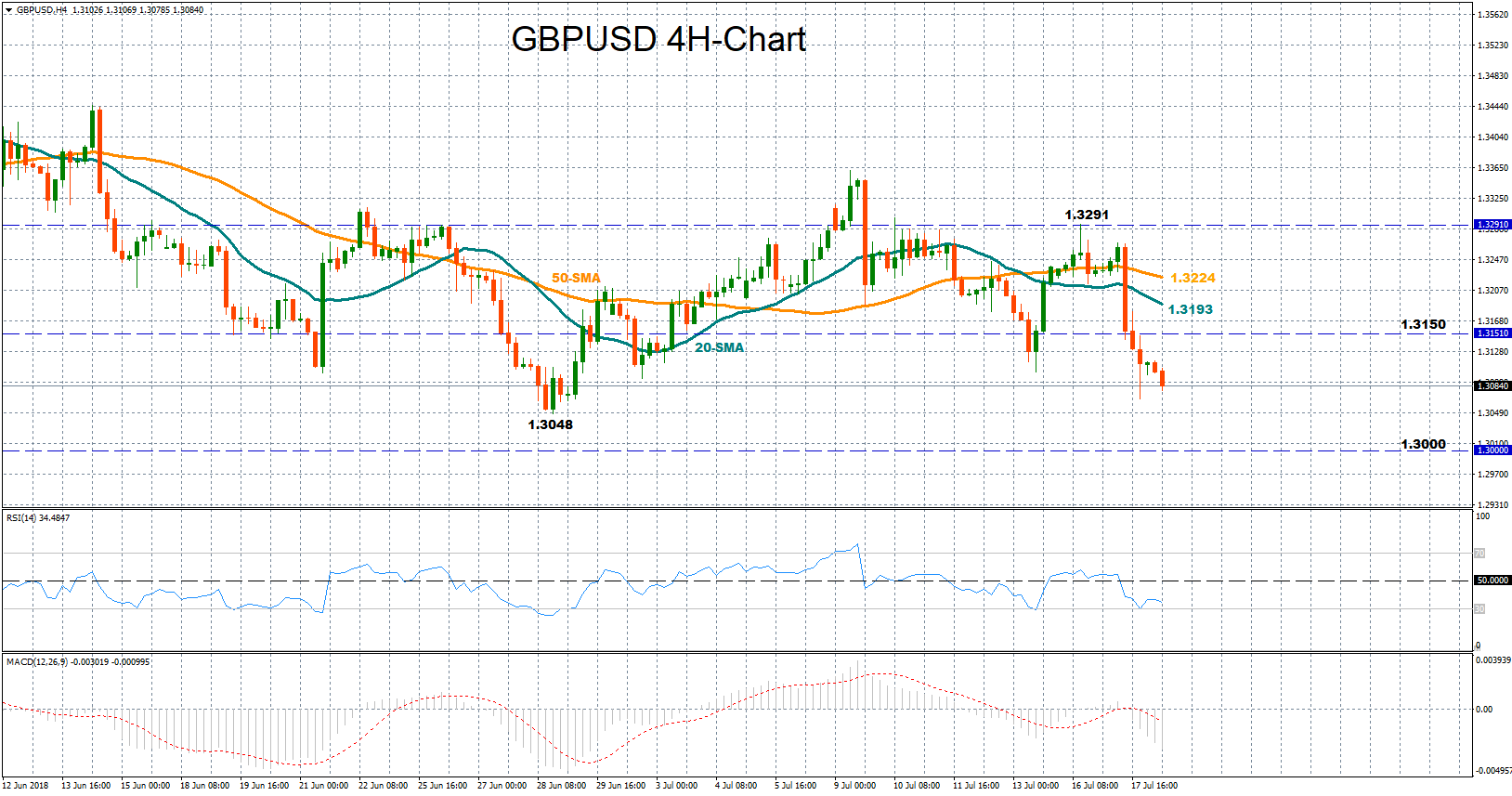

Technical Analysis: GBPUSD dives below 1.3100; bearish bias still in place

GBPUSD turned aggressively to the downside on Tuesday, losing 1.2% to approach three-week lows at 1.3067. Today the bearish sentiment continues to weigh on the pair, with the MACD pointing to further weakness as the indicator increases negative momentum below zero and its red signal line. The RSI also fluctuates in bearish territory, though its heading towards oversold levels, hinting that a rebound could be around the corner.

Should the price bounce above the 1.31 key-level in case CPI numbers come in stronger than expected, immediate resistance could come around 1.3150 where the price paused for a while back in June. A leg higher could then touch the 20-period moving average currently at 1.3193 before bulls meet the 50-period MA at 1.3224. The previous high at 1.3291 (July 16), though, could prove a stronger obstacle to break as the price topped several times around this peak in the past.

Conversely, a fall in GBPUSD on the back of disappointing UK figures that negatively affect the prospects for a BoE hike in August could retest June’s trough of 1.3048, the lowest level reached this year. Further below, the 1.30 round figure would be eyed next.