- Oil prices rise, but the dollar posts losses as Middle East tensions persist.

- US earnings, the ECB and UK newsflow dominate next week’s agenda.

- US equity markets face a pivotal test as focus shifts to technology earnings.

- Pound strength could be challenged, while Euro rally relies on a hawkish ECB surprise.

Dollar weakens, Oil jumps and equities underperform

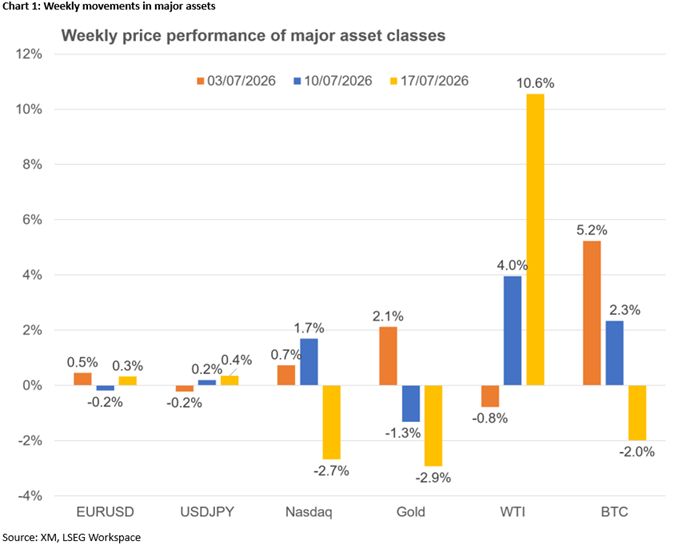

Amidst a mixed trading week, the US dollar, oil and US equities have been in the spotlight. Following a mixed start to July, the softer CPI and PPI reports put the greenback under pressure, overshadowing the persistent hawkish rhetoric from Fed Chair Warsh. However, equity weakness and some degree of safe haven flows linked to renewed Middle East tensions eventually limited dollar losses.

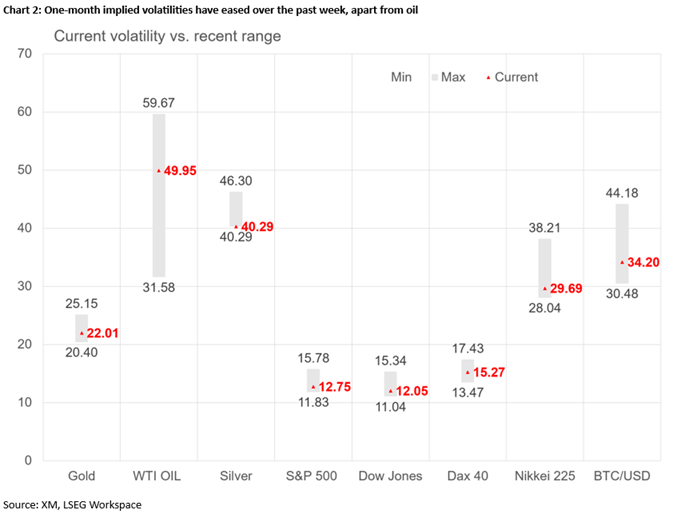

Geopolitical tensions have also woken up oil prices, with both spot WTI and December 2026 WTI oil futures posting solid gains as the risk premium jumped, pushing volatility to fresh highs. A contributing factor to these price increases has been the barrage of Ukrainian attacks on Russian oil installations, especially oil refineries, as the four-year-old conflict has entered a new phase of escalation lately.

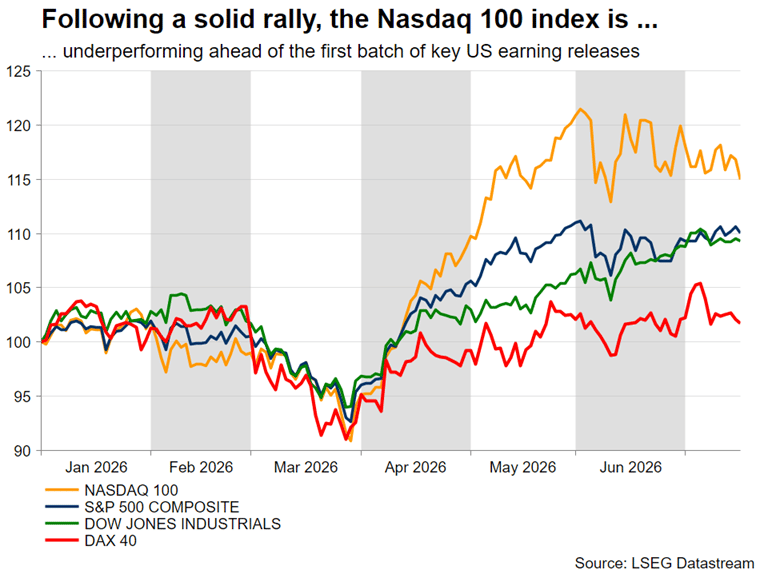

More importantly, despite the reduced chances of a September Fed rate hike, and the fact that the first earnings reports from US banking institutions and technology firms have been optimistic, beefed-up expectations for a stellar earnings season eventually led to a profit-taking correction. The Nasdaq 100 index bore the brunt, with European equities also failing to recover from last week’s weak performance.

Looking ahead, despite the lack of pivotal US data releases, investors are expected to focus on three main events next week: earnings, the ECB meeting and the busy UK calendar, both data-wise and politically.

Strong earnings could help equities recover

The earnings season picks up speed next week, with dozens of companies announcing their Q2 results. However, technology stocks will be in the spotlight, as Alphabet and Tesla report on Wednesday, after US markets close, followed by Intel on Thursday.

Thursday’s equities decline was another reminder of market nervousness and lingering concerns about the actual implementation of the substantial AI investments already announced and their true profitability. That said, a series of robust earnings results, along with further solid AI investment commitments, could prove the decisive factor for a revival of the Nasdaq 100 index, which has been underperforming so far in July. An initial climb to 29,731 would open the door to a retest of the upper boundary of the forming symmetrical triangle at 30,300, pulling other risk assets like bitcoin higher.

Crucially, persistent nervousness due to solid signs of a weaker outlook and/or a slower pace of AI investments would support the current bearish momentum. A drop below 28,180-28,400 could snowball, with Nasdaq 100 bears aiming for a decline towards the 100-day simple moving average (SMA) at 27,550.

Could the ECB pave the way for a September hike?

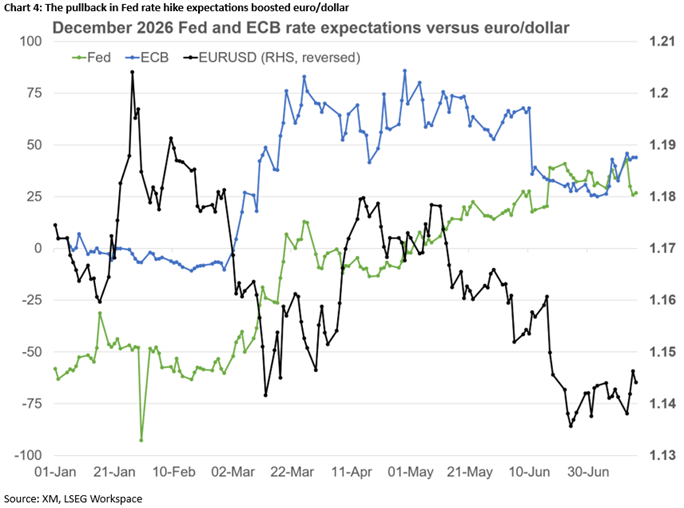

Following a difficult first half of the month, the euro managed to benefit from softer US inflation, advancing versus the dollar this week. This move, though, might prove short-lived if next Friday’s preliminary PMI surveys remain soft and the ECB fails to deliver a hawkish surprise on Thursday.

To be fair, chances of a hawkish surprise almost completely faded after the July 1 euro area inflation report, keeping the euro under bearish pressure, as markets priced out rate hikes during 2026. However, the restart of hostilities in the Middle East and the escalation in the Russia-Ukraine conflict, have reignited inflation concerns, supporting rate hike expectations. Markets are almost fully pricing in a 25bps rate hike in September, but assign only a 15% probability to such a move next week.

A hawkish press conference, with the usual post-meeting insider article solidifying September rate hike expectations, could help euro/dollar return inside the wide 1.1474-1.1830 range, with euro bulls targeting a rally towards 1.1530. However, a more likely scenario of a balanced meeting with few clues about September could reverse the current upward glide, especially if earnings boost demand for US stocks. A decline towards this week’s trough at 1.1375 could act as a basis for a retest of the one-year low of 1.1324.

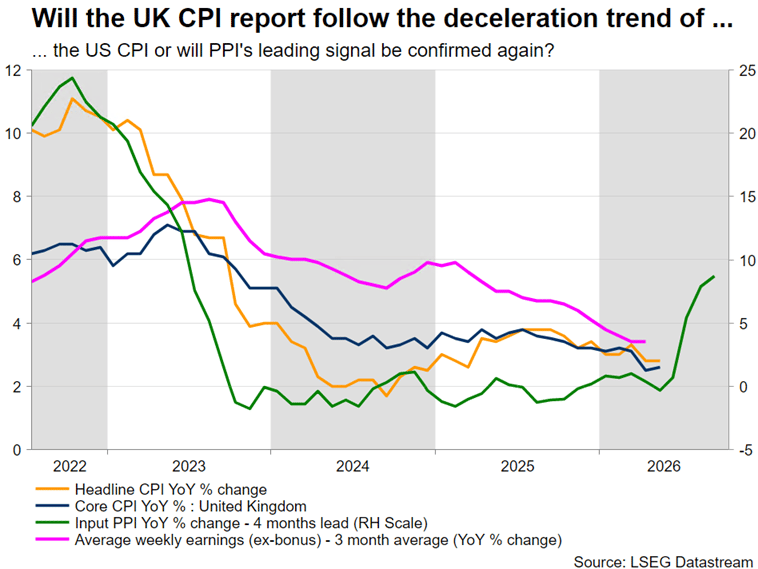

Will data and politics upset the recent Pound strength?

The fourth consecutive weekly pound gains against the euro could be challenged next week. The busy data calendar includes key releases such as Tuesday’s claimant count and Friday’s retail sales figures and the preliminary PMIs, although Wednesday’s CPI report, which may surprise on the downside, could prove more market-moving.

Meanwhile, despite the positive market reaction so far, Andy Burnham’s arrival at Downing Street remains a risk factor. Burnham is scheduled to take office on July 20, deliver his first speech and announce his first cabinet that day. Confirmation of reports that Shabana Mahmood will become the next Chancellor should keep bondholders happy, although there are many gaps to be filled about Burnham’s mix of economic policy, particularly the funding sources of his public investment plans.

Pending a hawkish surprise from the ECB, the current bearish trend in euro/pound might have legs. Specifically, a softer UK CPI report, coupled with a healthy labour market and strong retail sales – partly due to the good performance of the English football team in the FIFA World Cup – could boost the pound’s momentum, assuming that Burnham does not upset markets. In this case, pound bulls may be eager to test the busy 0.8400 area. On the flip side, a tax-heavy fiscal agenda would outweigh any upbeat data prints, putting the pound into a tailspin. A climb above 0.8538 could open the door to a more protracted rally in euro/pound.

Loonie and Aussie eye data, Dollar/Yen stabilizes while Gold craves bullish catalysts

Both the loonie and the Aussie took great advantage of Dollar vulnerability. Looking ahead, with the BoC failing to appear hawkish this week, a soft Canadian CPI report on Monday could put a temporary stop to the loonie’s rally, while strong Australian jobs data, along with more information on the upcoming Chinese Politburo meeting, could extend the Aussie’s advance. The next key support level for dollar/loonie stands at 1.3977, while a rising aussie/dollar could test the 0.7050 region. Alternatively, a break of 1.4100 and 0.6890 respectively could spell trouble for peripheral currencies as dollar bulls would regain the upper hand.

Meanwhile, dollar/yen continues to aimlessly hover above 162. Volatility has crashed to year-to-date lows, potentially reducing the urgency from Japanese authorities to intervene. A persistent dollar weakness might wake up the yen, with 161.20 potentially acting as the first support level.

Finally, gold’s battle for $4,000 persists. A possible continuation of the Middle East hostilities would push gold towards the key support area at $3,886, a move that could snowball if equity weakness gains momentum. Only fresh tariff headlines, since the Section 301 investigations are scheduled to be completed before the Section 122 tariffs expire on July 24, could restore gold demand in the short-term.

{kind=link}