Here are the latest developments in global markets:

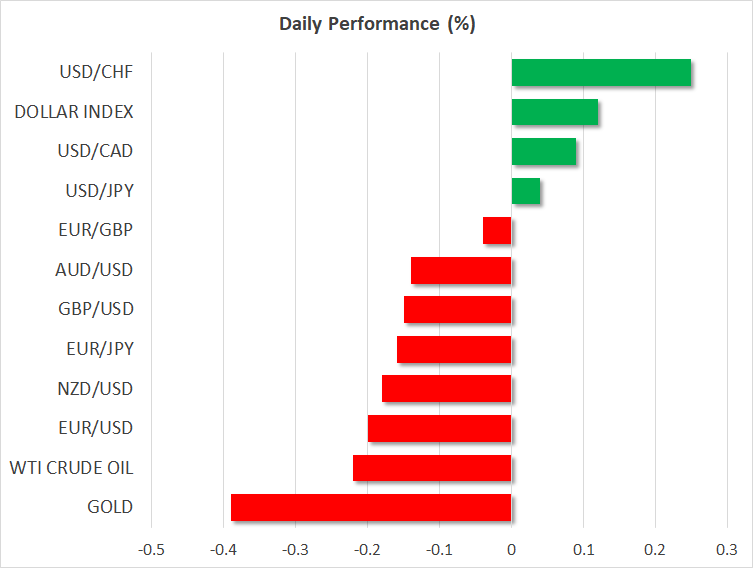

FOREX: The US dollar index advanced higher on Monday, recovering some of its Trump-induced losses as a solid rise in US bond yields increased the currency’s appeal. Heightened expectations for a very strong US GDP print for Q2, due out on Friday, may have supported the move. The yen also grinded higher, as speculation continued to mount that the Bank of Japan may alter its policy in a more hawkish direction as soon as at next week’s policy meeting.

STOCKS: US markets closed mixed on Monday, with the S&P 500 (+0.18%) and Nasdaq Composite (+0.28%) advancing, but the Dow Jones (-0.06%) edging slightly lower. Futures tracking these three indices were pointing to a flat open today. In company-specific news, the stock of Google parent Alphabet soared in after-hours trading, with futures suggesting a new record high today, as the firm reported much stronger earnings than projected. Asia was a sea of green on Tuesday, with Japan’s Nikkei 225 and Topix edging higher by 0.51% and 0.47% respectively. In Hong Kong, the Hang Seng was up by 1.39%. All European benchmarks were expected to open higher today according to futures, with the only exception being the UK FTSE 100.

COMMODITIES: Oil prices fell on Monday, giving back all the gains they posted early in the session on the back of mounting tensions between the US and Iran. The decline appeared to be driven by a combination of a stronger dollar and expectations Saudi Arabia and other major producers will continue to raise their production. WTI was down by 0.21% on Tuesday to touch $67.89 per barrel, though Brent rebounded somewhat, rising by 0.24% to $73.22. In precious metals, gold fell on Monday and is 0.38% lower on Tuesday as well amid a stronger dollar, which renders the dollar-denominated metal less attractive for investors using foreign currencies. The metal is currently trading near $1,220 per troy ounce, not far above its lows for the year at $1,211.

Major movers: Rising yields boost dollar; yen grinds higher on BoJ speculation

The US dollar edged higher against most of its major peers on Monday, with the only exceptions being the Japanese yen and Swiss franc, as a significant rise in Treasury yields boosted the appeal of the world’s reserve currency. The dollar index recovered part of the losses it posted on Friday after the US President criticized the Fed’s tightening plans, calling for fewer rates increases. Still, investors remain fairly convinced the Fed will raise rates twice more this year, with one 25bps rate hike being fully priced in already and markets assigning a 65% probability for a second one, according to the Fed funds futures.

US GDP growth in the second quarter is expected to be close to 4.5% on an annualized basis, models like the Atlanta Fed GDPNow suggest, something likely playing a large role in fueling expectations for quicker Fed hikes and hence supporting the dollar. The first estimate of GDP for Q2 is due out on Friday. Recent media reports indicate the White House is touting a number even higher, around 5%.

The Japanese yen was another notable mover, gaining across the board amid speculation the Bank of Japan (BoJ) may tweak its policy in a more hawkish direction at its policy gathering next week. The BoJ is currently keeping yields on longer-dated Japanese bonds capped at 0.10%, something that renders the yen less attractive from a relative interest rates perspective. Recent reports suggest policymakers may raise that yield target ceiling slightly, perhaps by 2bps to 0.12%, which could spark some repatriation of Japanese funds from abroad, thereby strengthening the yen. That being said, it remains questionable whether the Bank will actually proceed with tweaking its policy so early, particularly considering that the inflation outlook in Japan remains subdued.

Day ahead: Eurozone PMIs due; Markit’s US manufacturing PMI also out

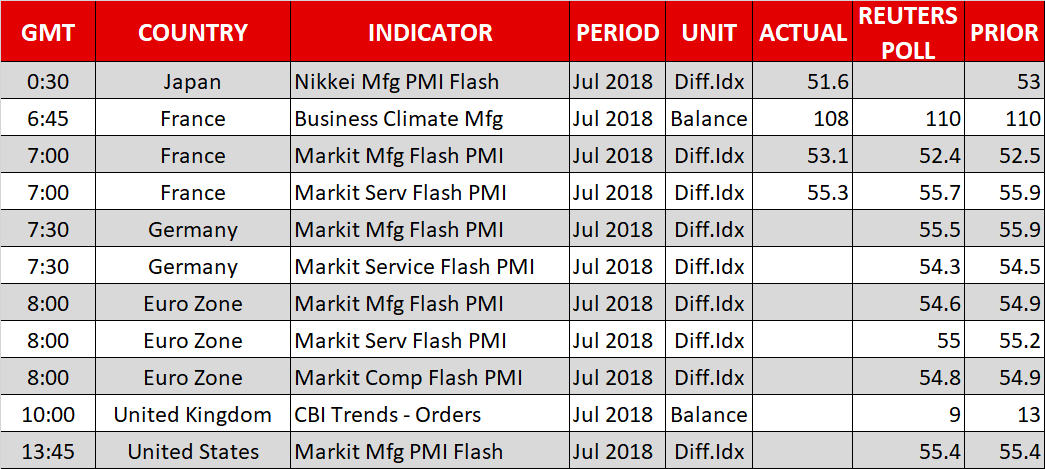

The main releases out of Tuesday’s calendar pertain to the eurozone’s flash PMIs for the month of July.

At 0800 GMT, the eurozone will see the release of flash PMI figures for the manufacturing and services sectors, as well as the composite measure the blends the two. All three prints are anticipated to weaken a bit relative to their respective June readings, though overall they’re expected to paint a mostly steady picture of economic activity. Moreover, they’re all projected to comfortably remain above the 50 threshold that separates sectoral expansion from contraction. It is notable that if the manufacturing PMI indeed declines, this would mark its seventh straight monthly fall. Meanwhile, the numbers might attract additional interest than usual, given they come out two days before the ECB’s meeting on monetary policy.

Germany, the eurozone’s largest economy, will see the release of its corresponding PMI figures at 0730 GMT; its numbers might be viewed as a preamble for what is to follow in terms of the euro area release. France’s respective prints were made public at 0700 GMT. A miss was delivered on the services front and a data beat on the manufacturing front; the euro initially fell a bit before recovering its losses.

Out of the UK, the Confederation of British Industry’s industrial orders data for July is due at 1000 GMT, with the monthly orders balance expected to ease to +9 in July, after jumping to +13 in June.

Markit’s US flash manufacturing PMI for July will be hitting the markets at 1345 GMT. It is forecasted to remain steady at 55.4.

In equities, 3M, AT&T, Verizon, and Harley-Davidson are among companies releasing quarterly results today; AT&T will be reporting after the market close, with all others releasing results before the opening bell on Wall Street.

In energy markets, weekly API data on US crude stocks due at 2030 GMT may give some short-term direction to oil prices.

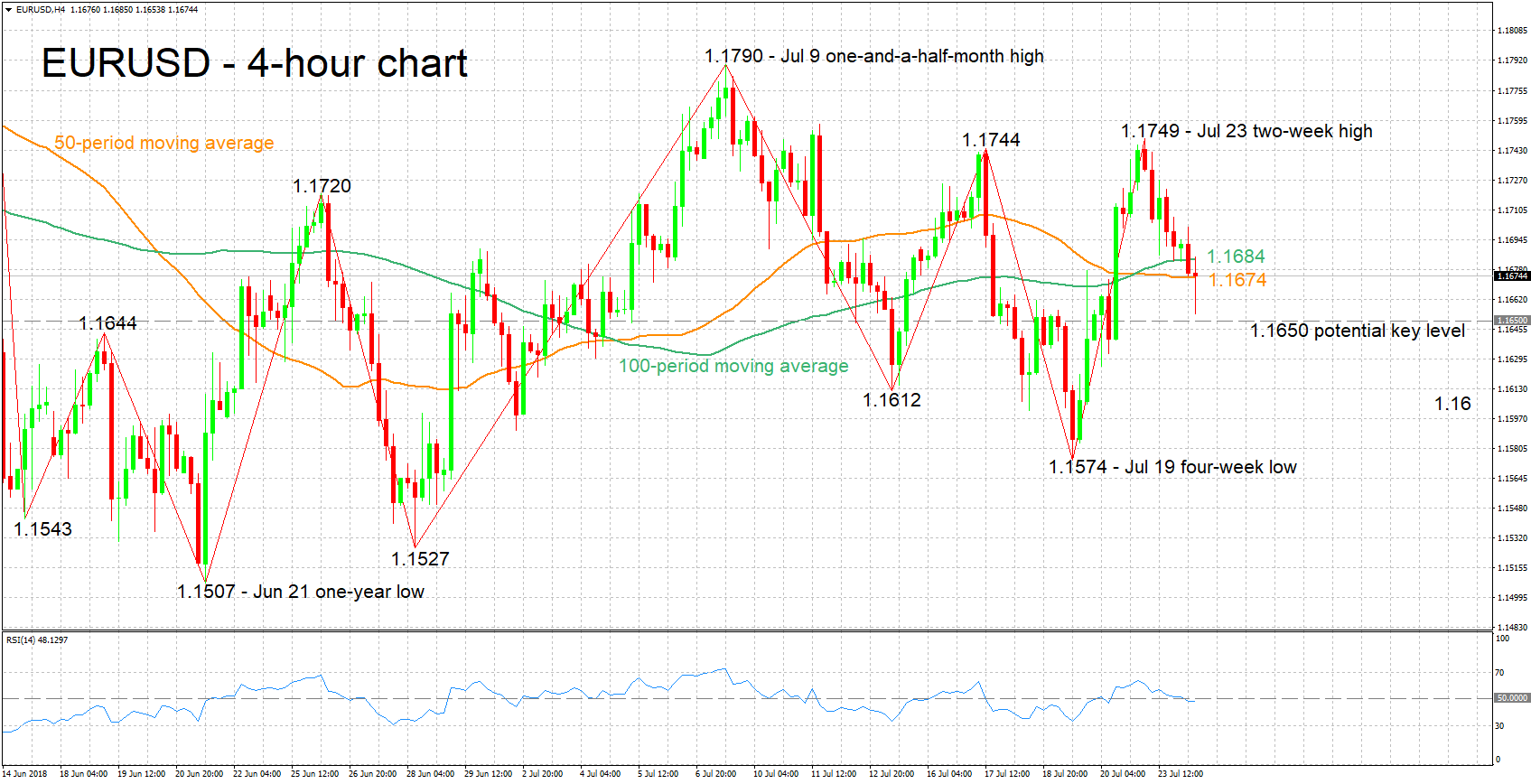

Technical Analysis: EURUSD moderately bearish in the short-term

EURUSD has lost ground after touching a two-week high of 1.1749 on Monday. The declining RSI is projecting a bearish picture in the short-term, though the negative bias does not appear strong – the indicator is only moderately negatively sloped.

Upbeat eurozone PMI readings are anticipated to boost the pair. An initial line of resistance seems to be taking place around the current levels of the 50- and 100-period moving average lines at 1.1674 and 1.1684 correspondingly, with the area around them also encapsulating the 1.17 round figure. Further above, yesterday’s two-week high of 1.1749 would increasingly come into view.

Conversely, weaker-than-expected readings are likely to push the pair lower. The region around 1.1650 was congested in the past and may provide support. Steeper losses would start bringing into scope the 1.16 handle.

Markit’s manufacturing PMI release for the US can also move the pair.