Here are the latest developments in global markets:

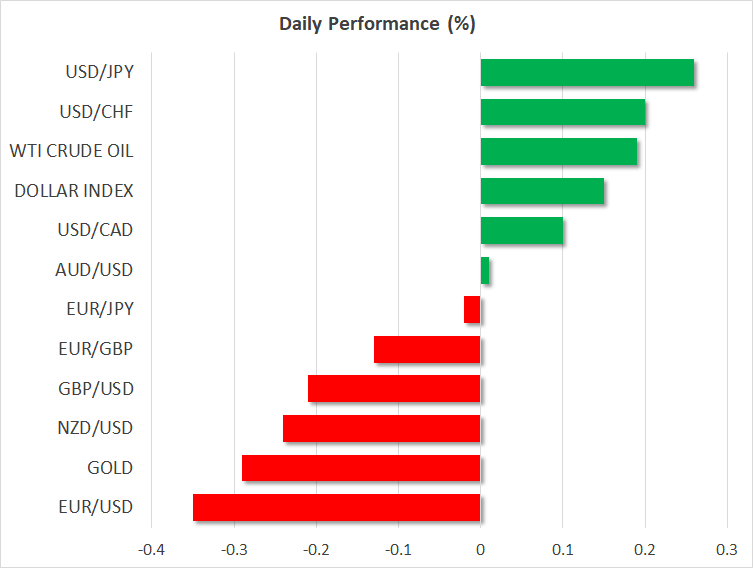

FOREX: The greenback is higher across the board on Tuesday, with the dollar index advancing by 0.15% in the absence of any major new developments. The aussie jumped overnight after the RBA struck a less-cautious tone than many expected, erasing losses it posted earlier in the session after Australia’s current account data for Q2 disappointed. Earlier on Monday, the British pound came under renewed selling interest, following a miss in the UK manufacturing PMI.

STOCKS: Wall Street remained closed on Monday for the Labor Day public holiday. As for today, futures suggest that the S&P 500, Dow Jones, and Nasdaq 100 are all set to open higher, which would bring the S&P and the Nasdaq back within breathing distance of their recent all-time highs. It was a mixed session in Asia on Tuesday, as a looming escalation in the Sino-US trade skirmish continued to cast a long shadow. Even yen-weakness was unable to lift Japanese markets, with the Nikkei 225 (-0.05%) and the Topix (-0.12%) pulling back somewhat. In Hong Kong though, the Hang Seng managed to climb by 0.75%. In Europe, futures tracking all the major benchmarks were flashing green, pointing to a higher open today.

COMMODITIES: Oil prices edged higher on Tuesday, extending gains from yesterday. WTI rose by 0.19% to trade at $70.35 per barrel, while Brent was up by 0.09% at $78.22/barrel. The latest leg higher is seemingly owed to reports that two oil platforms in the Gulf of Mexico were evacuated in anticipation of a hurricane, likely amplifying speculation for temporary supply disruptions. In precious metals, gold is down by 0.29% at $1196 per troy ounce on Tuesday, weighed on by a recovery in the US dollar. Since the yellow metal is denominated in dollars, a stronger greenback renders it less attractive for investors using foreign currencies, and vice-versa.

Major movers: Pound extends losses, looks to BoE-talk for relief; dollar bounces

The British pound extended its recent losses on Monday, with euro/sterling crossing back above the 0.9000 handle after disappointing UK manufacturing PMI data for August provided traders another reason to limit their sterling exposure. Market attention will likely remain on the UK today, as several BoE officials including Governor Carney and chief economist Haldane are due to testify before Parliament at 1215 GMT. In the midst of Brexit worries, investors have pushed back the anticipated timing of the next BoE rate increase to November 2019, according to UK OIS. Any hints from policymakers suggesting a hike may come earlier than that could provide some temporary relief to the battered pound. More broadly though, Brexit worries may continue to cap any sustained rallies in sterling, after the EU’s Barnier implicitly rejected the UK’s plan on trade recently.

In Australia, the RBA kept its policy unchanged overnight, as was widely expected. Policymakers appeared slightly more optimistic than previously on the the labor market, while they also brushed aside some worrisome developments, like rising mortgage rates in commercial banks. The officials’ overall neutral tone likely came as a surprise to investors anticipating a more cautious bias, causing aussie/dollar to jump on the decision, erasing earlier losses that came on the back of lackluster current account data for Q2.

Meanwhile, the dollar is higher across the board on Tuesday, with little in the way of fresh news behind the move – recall that the US and Canada were closed for a public holiday yesterday. Ahead of the payrolls report on Friday, the US currency will likely stay sensitive to any potential escalation in trade tensions between the US and China, with any increase in frictions possible to divert safe-haven flows into the greenback.

Elsewhere, the loonie continued to lose ground after Trump tweeted over the weekend that Congress should not interfere with the NAFTA talks, otherwise he will terminate NAFTA entirely – which interestingly he cannot do without Congressional approval. Dollar/loonie broke back above 1.3000, with the US-Canada talks set to resume tomorrow.

Day ahead: US manufacturing PMI, eurozone producer prices and UK construction PMI due; trade and EM angst lingers

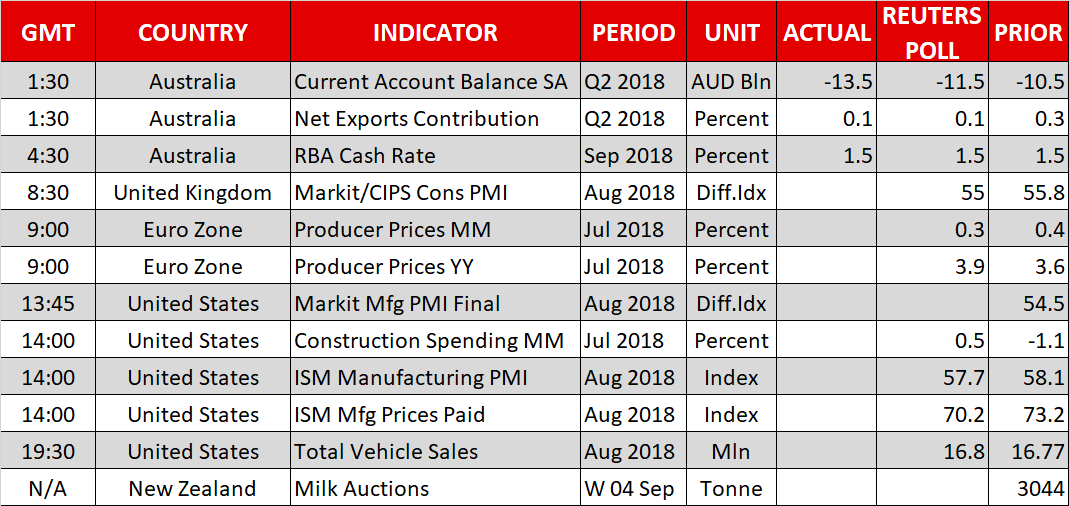

Tuesday’s economic releases include manufacturing PMI and total vehicle sales out of the US, as well as eurozone producer prices and UK construction PMI numbers. Investor focus though will continue to remain on ongoing trade and emerging market worries.

On the trade front, the US and Canada will be looking into whether they can enter into a new North American trade deal; an agreement by the US and Mexico already materialized last week. As regards China, President Donald Trump last week showed willingness to push forward with tariffs on $200 billion in additional Chinese products as soon as Thursday.

In terms of data, construction PMI data due out of the UK at 0830 GMT are anticipated to show the gauge weakening to 55.0 in August from July’s 55.8. Yesterday’s respective data for the manufacturing sector showed the relevant measure unexpectedly falling to its lowest since July 2016 – immediately after the Brexit referendum – and acted as a drag on sterling. The PMI print for the all-important services sector will be released tomorrow.

At 0900 GMT, eurozone producer prices for July will be made public. The monthly pace of growth is projected to ease to 0.3% from June’s 0.4%, though this is still enough to push the year-on-year rate to 3.9% from 3.6% in June.

The ISM’s manufacturing PMI for August will be hitting the markets at 1400 GMT. The measure is forecast to weaken for the third straight month, though still – at 57.7 – comfortably remain in expansion territory above 50. It will be interesting to see whether the lingering trade disputes will weigh on the print to a significant extent. The numbers on manufacturing prices paid for August and July’s construction spending are due at the same time, while the final reading on Markit’s manufacturing PMI for August will be released a little earlier (1345 GMT).

Also out of the US are August’s total vehicle sales, scheduled for release at 1930 GMT. A small recovery in sales is predicted, specifically to 16.80 million, from July’s 16.77m which was the weakest since August 2017. Higher interest rates are a negative for auto sales.

Dairy products are New Zealand’s largest goods export earner, and in this respect the outcome of today’s bi-weekly milk auction may move the local dollar; higher prices are generally seen as kiwi-positive. The results of the auction lack a specific time of release.

RBA Governor Philip Lowe will be making some comments at 0930 GMT, following the central bank’s policy decision earlier today.

Elsewhere, at 1200 GMT, Bank of England Governor Mark Carney will be testifying on the August inflation report and policy decision to raise rates by 25bps. He will be accompanied by MPC policymakers Andy Haldane, Silvana Tenreyro and Michael Saunders. Important for sterling will be any updates on Brexit; PM May’s Brexit proposal was criticized both at home and in Brussels.

In EM, the Argentine peso is losing ground on Tuesday even as the government took steps to boost investor confidence and the central bank considerably bumped up rates last week. The Turkish lira, South African rand, Brazilian real, and Indian rupee are some other EM currencies that have come to the fore in recent weeks.

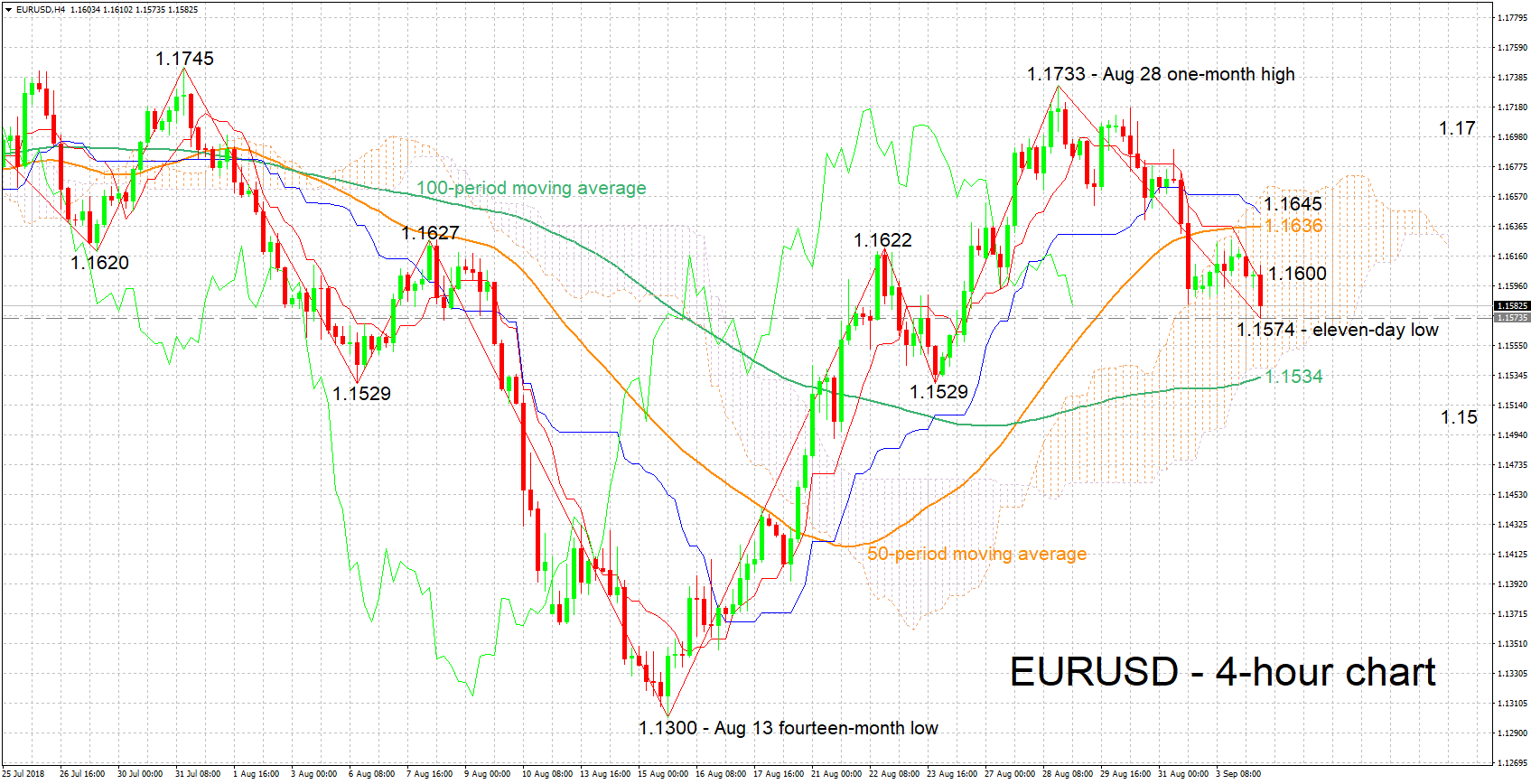

Technical Analysis: EURUSD looking bearish in the short-term, touches 11-day low

EURUSD is trading not far above the 11-day low of 1.1574 hit earlier in the day. The Tenkan-sen line is below the Kijun-sen in support of a bearish short-term picture. Today’s releases out of the eurozone and the US do not usually act as major market movers, but they could still lead to some positioning on the pair.

Upbeat eurozone releases or downbeat US ones may boost EURUSD. Given a move above the 1.16 round figure which is where the Tenkan-sen also lies, resistance may come around the current level of the 50-period moving average line at 1.1636; the Kijun-sen (1.1645) and Ichimoku cloud top (1.1664) are also part of the area around this level. Further above, the 1.17 handle would be eyed and then the one-month high of 1.1733 from late August.

Conversely, weak eurozone numbers or overall strong US figures are likely to exert pressure on EURUSD. A move below the earlier recorded 11-day low of 1.1574 may find support around the 100-period MA; this is where the Ichimoku cloud bottom roughly lies as well, while the zone around this also includes a couple of bottoms from the recent past. Steeper losses would bring the 1.15 mark within scope.

{kind=link}