Here are the latest developments in global markets:

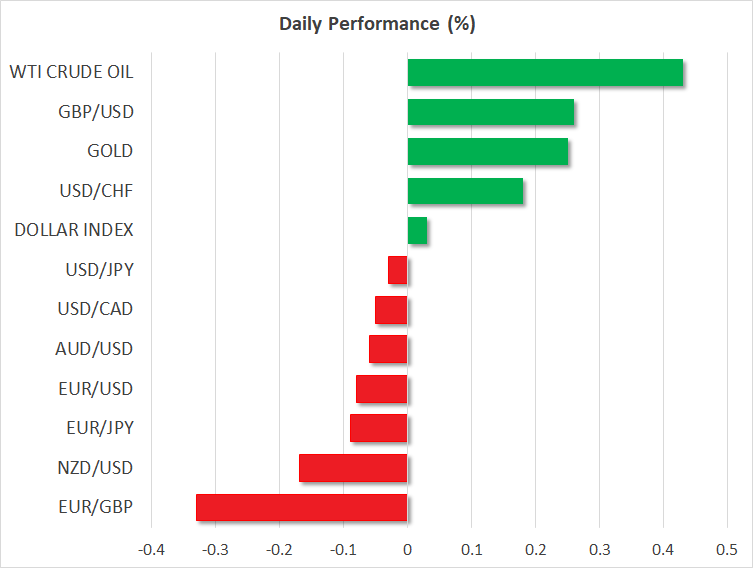

- FOREX: The US dollar held steady against the Japanese yen on Friday, as investors turned their attention to the monthly US Nonfarm payrolls report due later today. The pair was last trading around 113.87. However, the US dollar index, which tracks the dollar’s strength against six major currencies, edged higher by 0.13% and is set to complete the second consecutive green week. Turning to Brexit news, European Union Brexit negotiators see a deal with Britain in the near future, a hint that pushed pound/dollar as high as 1.3059 today, though it soon slipped back to 1.3040 (+0.15%). Euro/dollar was unable to extend yesterday’s gains,.retreating a touch below 1.1500 (-0.13%) as tensions between the EU and Italy resurfaced, with the Italian Deputy Prime Minister expressing his dissatisfaction over the European Commission’s methods on Friday. The antipodean currencies maintained a bearish mood for the fourth straight day, with aussie/dollar inching down by 0.10% and kiwi/dollar falling by 0.25%. These pairs recorded new multi-year lows earlier in the day at 0.7051 and 0.6457 respectively. Dollar/loonie jumped by 0.05%. It is worth noting that overnight index swaps give an 84% probability for a BoC rate hike this month.

- STOCKS: Major European benchmarks traded lower on Friday as US 10-year Treasury yields held near 7-year highs. German and Japanese government bond yields also spiked higher, though to a smaller extent. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were down by 0.61% and 0.45% respectively. Meanwhile, the UK’s FTSE 100, German DAX and the French CAC 40 were trading lower by 0.79%, 0.76% and 0.45% correspondingly. Also, the Spanish IBEX 35 retreated by 0.51%. In Asia, stocks closed in negative territory, while futures tracking US indices such the S&P 500, Dow Jones and Nasdaq 100 were slightly down, pointing to a negative open today.

- COMMODITIES: WTI crude oil was marginally up at $74.4/barrel and Brent was down at $84.26/barrel (-0.38%). On the one hand, traders expected a tighter market due to US sanctions against Iran’s crude exports next month. However, reports today said that India, the third largest crude importer, is planning to buy 9 million barrels from Iran in November, bringing some relief that US sanctions might not be as severe as markets anticipated after all. Note that India was among the countries which cut oil purchases from Iran in previous months, complying somewhat with US demands. In precious metals, gold slowly returned above $1,200/ounce, last seen at $1,203 (+0.32%). The dollar-denominated yellow metal will likely move according to the quality of the US jobs data today. A strong employment report could boost the dollar and thereby weaken gold, and vice versa.

Day Ahead: US Nonfarm payrolls take the stage; Canada reports on employment too

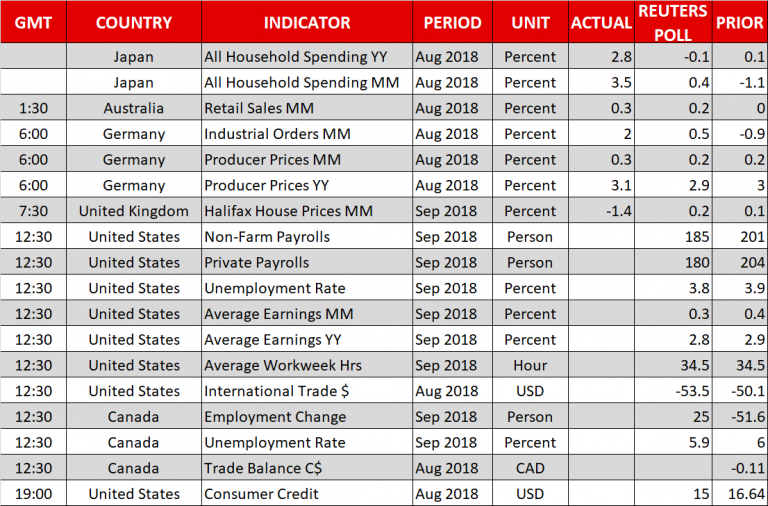

Friday will be jobs day for the US as the government is scheduled to release the all-important nonfarm payrolls report (1230 GMT), which could give a helping hand to the dollar if the numbers pop up better than forecasts, justifying optimism on the US economy and thus the Fed’s plans for tighter monetary policy in the coming years.

Analysts believe that the economy created 185k new job positions (private and public) in September, fewer than in August when payrolls increased by 201k. Average hourly earnings which tend to attract greater attention due to their inflationary impact are also expected to lose steam, with the yearly measure estimated at 2.8%, below the 2.9% tracked in August, while the monthly gauge is seen lower at 0.3% from 0.4%.

Yet, the unemployment rate could be good news to US consumers and Fed policymakers as the rate is projected to inch back down to 3.8% after remaining at 3.9% in the past two months.

At the same time the Bureau of Economic Analysis is expected to show that the US international trade deficit widened for the third straight month in August, increasing by $2.4 billion to $53.5 billion. If that is the case and specifically the trade deficit with China rises as well, the US President may unleash more bitter rhetoric against Beijing, making investors wonder whether Trump’s tariffs have any impact at all on narrowing the trade deficit.Not to mention that the US-Sino dispute has stretched into other areas as well given US’s blames for China’s meddling in US midterm elections and the recent tense standoff between US and Chinese warships in the South China Sea. Besides these, the US also accused Beijing of stealing US technology.

In other data out of the US, consumer credit for the month of August will be available for review at 1900 GMT. The figure could give an insight on consumer confidence.

Meanwhile in Canada, employment and trade readings will also come under the spotlight today at 1230 GMT. As in the US, forecasts are for the unemployment rate to decline in September, from 6.0% to 5.9%. Regarding the job creation, the Canadian labour market is said to have employed 25k additional people after letting out 51.6k in August, the biggest loss since February. Should the employment change rise by more than expected and/or the unemployment rate retreat by more than analysts think, the loonie could recoup earlier losses.

Potential comments on the Irish border, a key issue in the Brexit story, may trigger further movements in the pound. Headlines today stated that the EU negotiators are optimistic about reaching a compromise on the Irish backstop. Any progress on the matter before the EU summit on October 17-18 would be pound-positive. Note that the UK Prime Minister, Theresa May, has promised to provide the EU with new proposals to break the border deadlock.

In energy markets, Baker Hughes will report on the number of active US rigs for oil drilling at 1700 GMT, probably bringing some volatility to oil prices and the commodity-linked loonie.

In terms of public appearances, regional Fed Presidents Kaplan (non-voting FOMC member in 2018) and Bostic (voter) will be talking at 1430 GMT and 1440 GMT respectively. Moreover, during the weekend, US Secretary of State Mike Pompeo will be visiting Japanese Prime Minister, Shinzo Abe. Then he will fly to North Korea to meet the nation’s leader, Kim Jong-Un.

Early on Monday at 0145 GMT, investors will be looking at the Chinese Caixin Services PMI. The aussie could move if the data deviate from forecasts given the close economic relationship between China and Australia.

{kind=link}