The IMF presented its World Economic Outlook (WEO) on Tuesday, a survey that is released every six months, with economic activity estimates being updated in between. In its report, the organization stresses that downside risks to global growth have risen lately, with special mention made to threats stemming from intensifying trade tensions. Consequently, for the first time in more than two years, it has revised its global growth projections downwards, specifically to 3.7% for the years 2018-19 from 3.9% previously for both. The commentary that follows focuses on certain aspects of the report that relate to major economies and summarizes the IMF’s findings, blending them with our own views wherever deemed necessary.

US strength to linger amid fiscal impulse, but fade into 2020

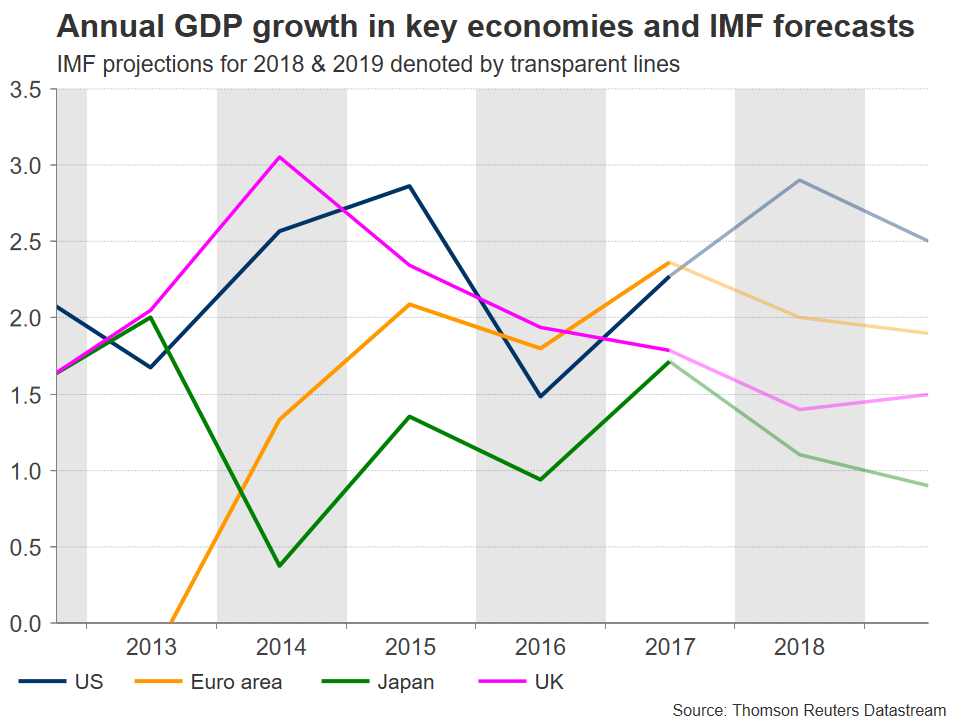

The IMF wasn’t particularly downbeat on the outlook for the US. The Fund kept its GDP estimates for 2018 unchanged from July at an elevated 2.9%, citing strong fiscal stimulus supporting growth. It did however, revise modestly lower its 2019 forecast, mainly due to the recently announced trade tariffs against China. Perhaps most striking, was a warning that US growth will decline in 2020 as fiscal stimulus begins to unwind at a time when monetary policy tightening may be at its peak.

On another interesting note, the Fund observed that despite the US economy operating above full employment, markets are pricing in less tightening than signaled by the Fed itself. This suggests an upside inflation surprise could trigger an abrupt repricing of expected rate increases, in turn catapulting US bond yields and the dollar higher. Besides boosting the dollar, such an outcome would also imply pain for riskier assets, most notably stocks. Yet, it’s perhaps puzzling that the IMF marked its US inflation forecasts lower both for 2018 and 2019, even in the face of tariffs that will add to consumer prices.

Worsening trade, weakening credit availability threatening Chinese economy

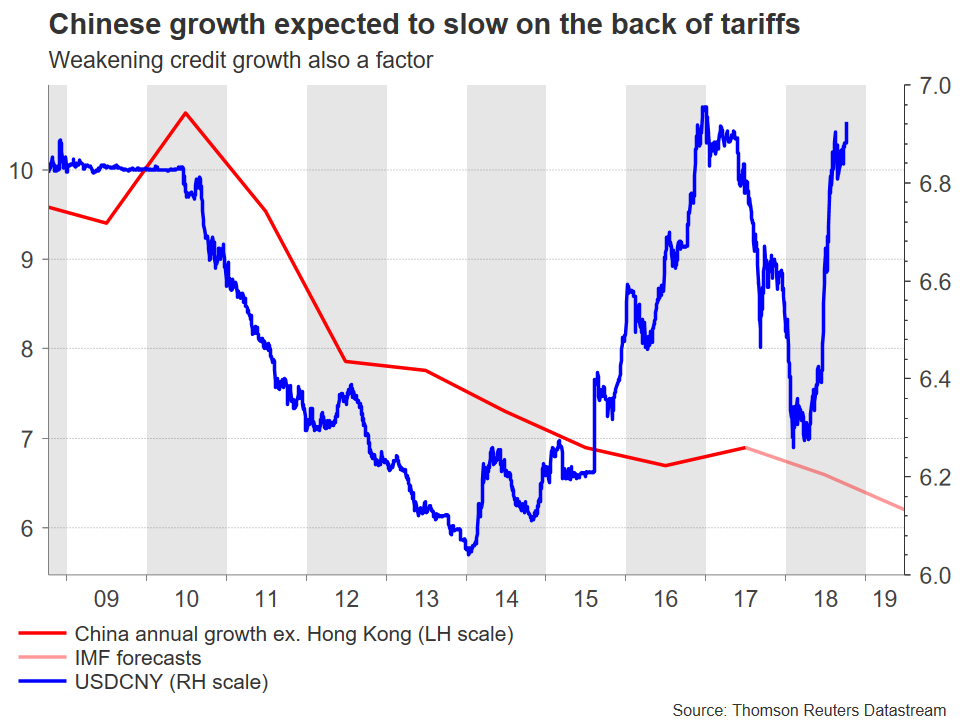

The international organization has maintained its 2018 growth forecast for the world’s second largest economy at 6.6% in 2018, which compares to 2017’s 6.9%. However, it revised its projections for 2019 to 6.2% from the previous 6.4%, as it anticipates that much of this year’s tariff actions will be felt next year. Overall, the IMF expects Chinese economic activity will remain robust moving forward but gradually decline.

Beyond trade risks, weakening credit growth is also cited as a drag to the economy. Given growing considerations for a debt crisis on the back of loose credit conditions in the past, this may well be long-term positive for China though, leading to a higher quality and less “fragile” growth outlook. In fact, the IMF states that the country should continue limiting credit expansion and address financial risks.

It bears mention that the aforementioned rely on base-case assumptions, which are not predicated on an all-out trade war between the US and China. The organization modelled the effects of a full-blown trade confrontation as well, with the negative outcome on the Chinese economy – and the US for that matter – being much more profound in that case, to state the obvious.

On the FX front, both the onshore (depicted above) and offshore yuan are currently trading not far below their weakest since January 2017 hit in mid-August. Despite China continuing to have relatively strong fundamentals, its currency is likely to come under increased pressure, at least during the remainder of the year. This is based on the fact that investors have so far opted to penalize the yuan whenever tensions between the two superpowers escalate, under the assumption that China has more to lose from the standoff.

Euro area seen weaker in 2018, unchanged further out

In Euro land, growth projections for 2018 were also pushed lower to 2.0%, from 2.2% in July’s estimates, as a streak of disappointing data releases earlier in the year dimmed the short-term outlook. For 2019, the IMF kept its forecasts unchanged from July, signaling that the bloc’s broader prospects haven’t changed radically.

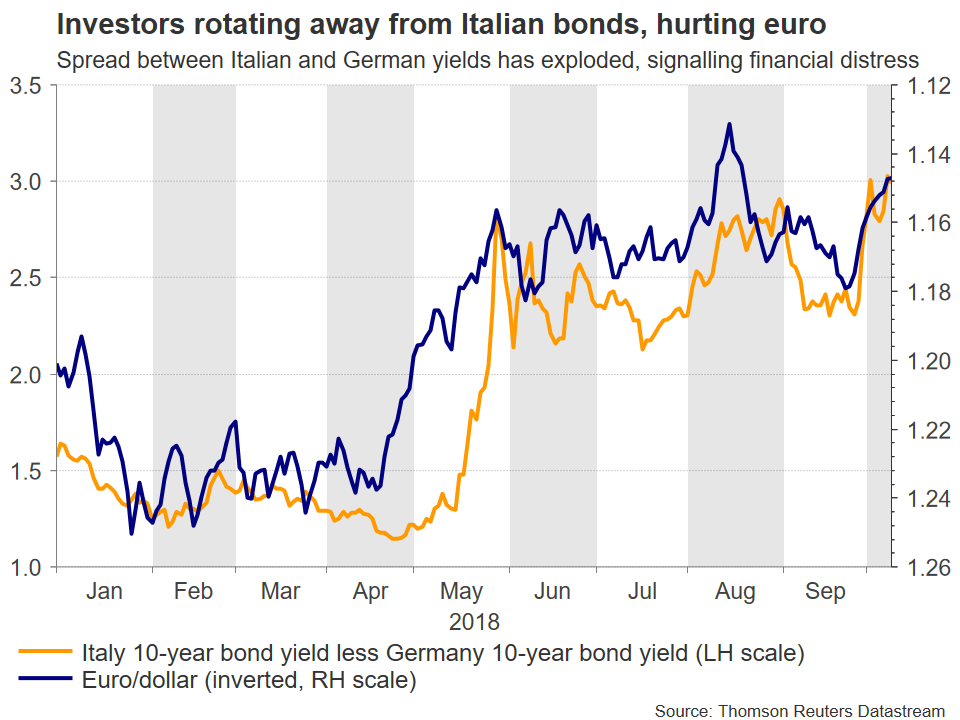

In the short-run, the euro’s path will hinge on how the Italian budget situation plays out. A risk premium has been priced into the currency amid jitters that Italy and the EU are headed for a clash over the budget deficit’s size. The details will be known by October 15, at which point the European Commission must approve or reject the budget; the euro will probably move accordingly. Separately, ratings agencies like Moody’s and S&P will be reviewing Italy’s credit position at the end of October, with a potential downgrade – and thus more pain for the euro – being in store if Italy sticks to its large deficit.

Brexit remains a key UK consideration

The Fund continues to believe that the UK economy will grow by 1.4% in 2018. However, this reflects a downgrade from April’s forecast of 1.6% and a slowdown compared to last year’s pace of 1.7%. In 2019, the respective projection has remained unrevised at 1.5%.

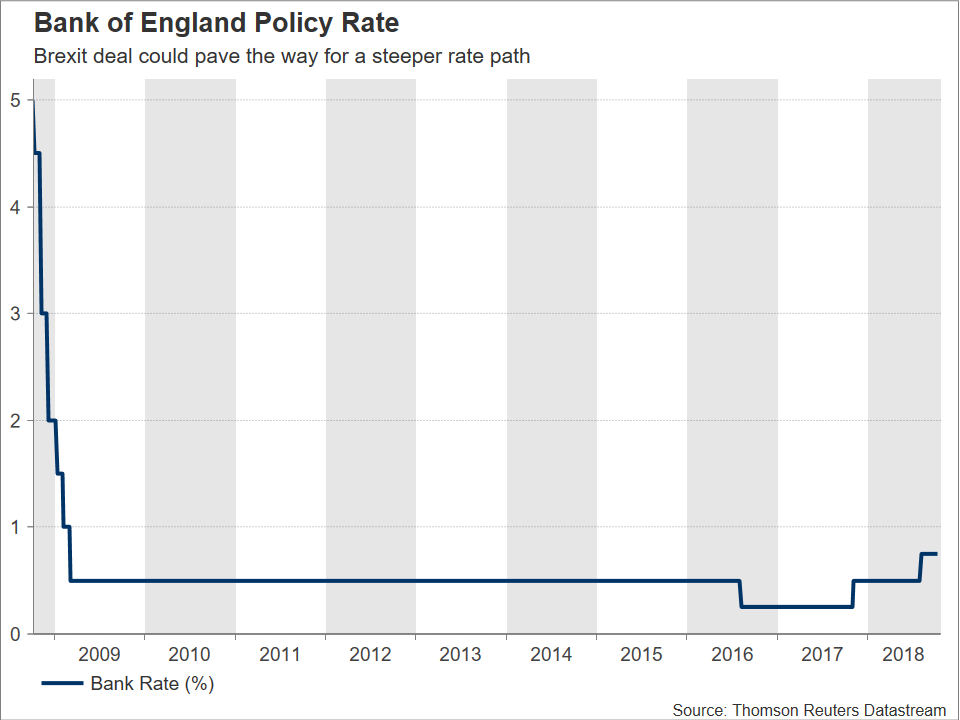

To the surprise of no one, Brexit and the possible failure in negotiations for an orderly exit from the EU bloc was cited as a risk. In this respect though, the market is currently pricing a relatively conservative BoE rate path, of roughly one hike per year. Should the no-deal cloud be lifted, something which recent news flow suggests is getting more and more probable, then sterling is likely to rally on the expectation of a steeper rate outlook.

In terms of price pressures, the IMF sees annual CPI easing in 2019, though still remaining above the Bank of England’s target of 2%. Of note is the revision of 2018’s CPI figure to 2.5%, from 2.7% previously.

Japanese growth seen treading water, inflation to remain below BoJ target

Japan’s economic growth is expected to slow to 1.1% this year, which represents an upgrade from July’s projection of 1.0%, but a downgrade from the 1.2% in April. The dimmer outlook from April was attributed to the contraction the economy suffered in Q1. Yet, the rebound in Q2 showed the dip was likely temporary, hence the slight upward revision from July. The estimates for 2019 were kept unrevised.

On the inflation front, although projections were revised a touch higher to 1.2% this year and 1.3% in 2019 on the back of higher energy prices, the broader picture remains bleak. The IMF expects inflation to remain below the Bank of Japan’s (BoJ) 2% target for the entire of its 5-year forecast horizon. Accordingly, the report highlighted that maintaining accommodative monetary policy is a “necessity”.

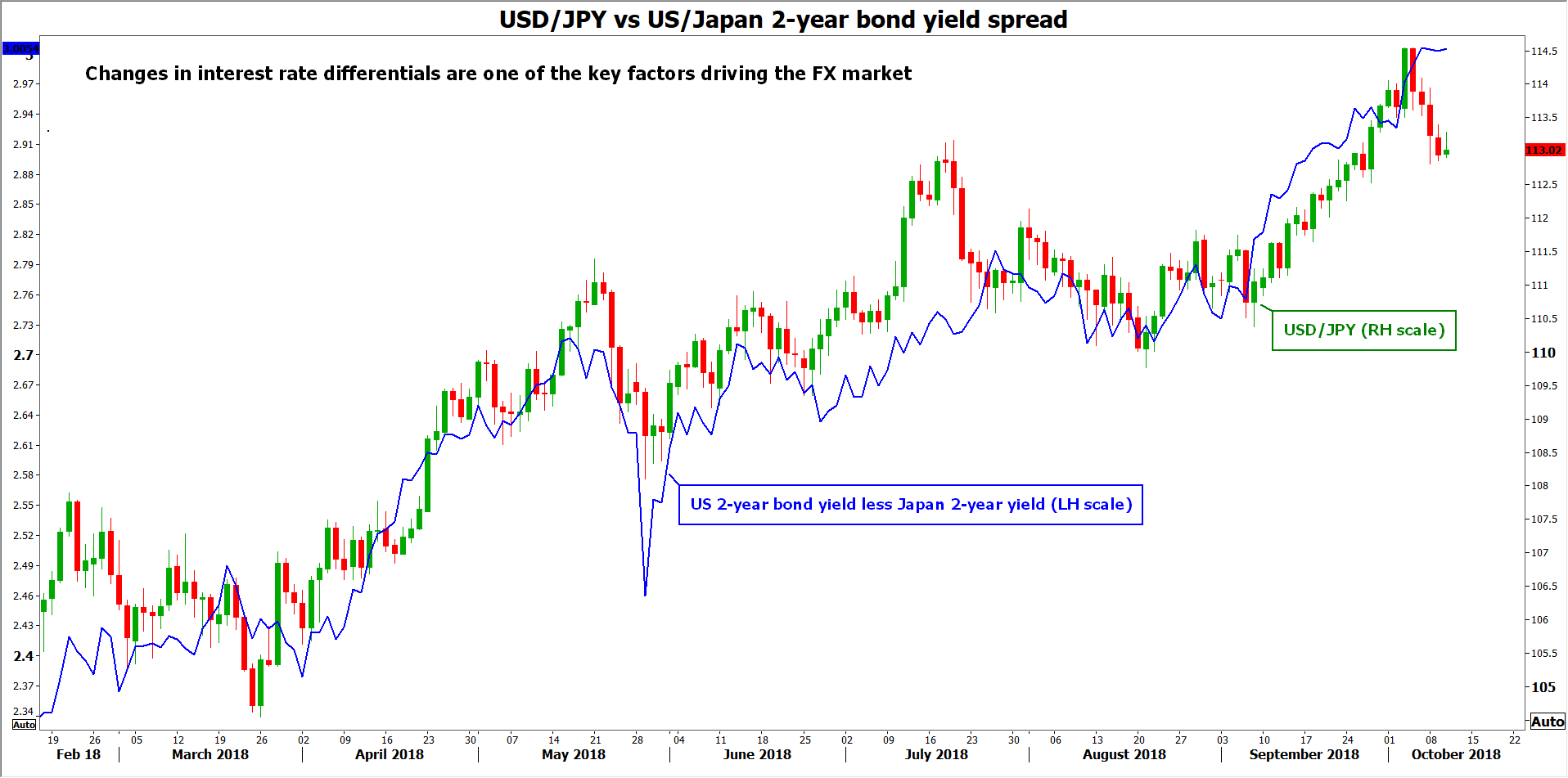

Indeed, the BoJ looks unlikely to materially modify its ultra-loose framework, under which it keeps the yields on 10-year Japanese bonds fixed around 0%. With the BoJ holding longer-dated yields capped near 0% while other major central banks like the Fed are raising rates, interest rate differentials between Japan and the US are widening, rendering the yen less attractive from a relative rates perspective. That said, the Japanese currency could always – and unexpectedly – attract safe-haven flows.

Market implications

In the big picture, the IMF placed enormous emphasis on the mounting risks presented by trade tensions, and their potential adverse effects on the global economy. In terms of market effects, higher trade barriers would probably trigger a defensive rotation towards haven-perceived assets, and away from riskier ones. Specifically, the Japanese yen – and to a lesser extent the US dollar – are likely to post gains in such an environment, particularly against currencies of economies that run substantial trade surpluses, like China and the Euro area. Beyond FX, equity markets are also expected to be vulnerable to greater trade frictions. Case and point, China’s CSI 300 index is already down by 18.6% year-to-date, and that trend may well continue should the confrontational rhetoric heat up further.

Now, as for the probability that the situation escalates, it appears to be relatively high, especially considering the recent rhetoric from both the US and China, the upcoming US midterm elections, and reports of tensions on noneconomic fronts as well. Moreover, the fact that China eased monetary policy and plans to do so with fiscal policy as well suggests it expects the standoff to be a prolonged one, and is “digging in” for the long haul.

{kind=link}