Here are the latest developments in global markets:

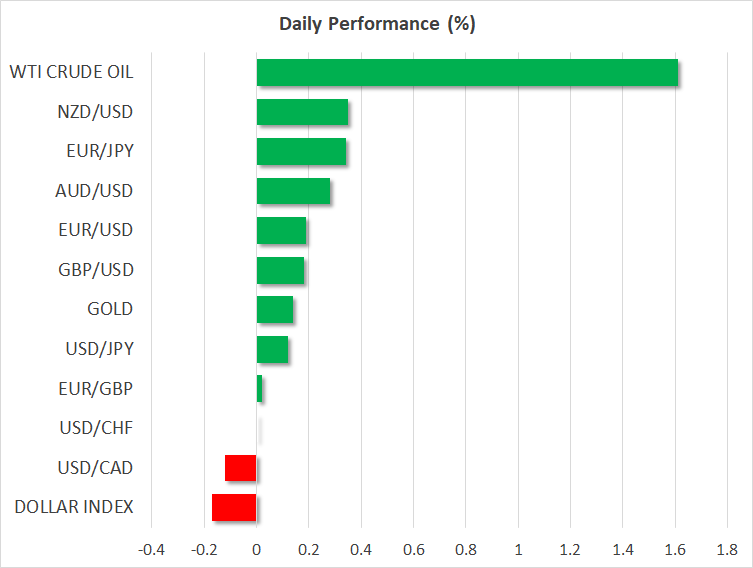

FOREX:The dollar index is somewhat lower on Wednesday (-0.17%), giving back some of the significant gains it recorded in the previous session as investors sought the safety of the world’s reserve currency. The loonie was the biggest underperformer, weighed down by another plunge in oil prices. Meanwhile, the yen and the franc attracted inflows amid the broad-based risk aversion, though both are today, as sentiment seems to have turned around somewhat.

STOCKS: US markets recorded another day of substantial losses, with the retail, technology, and energy sectors bearing the brunt of the pain. The Dow Jones (-2.21%) suffered the most, while the S&P 500 (-1.82%) and the Nasdaq Composite (-1.70%) did not fare much better. That being said, the mood seems to have turned around somewhat, as futures tracking the Dow, S&P, and Nasdaq 100 are all pointing to a higher open today. Asia was mixed on Wednesday, with Japanese indices falling but Chinese benchmarks ticking higher. In Europe, all the major indices were set to open higher today, futures suggest.

COMMODITIES: The carnage in crude accelerated, with WTI falling by a dramatic 6.6% on Tuesday, while Brent plunged 6.4%, with both benchmarks touching one-year lows. Prices rebounded somewhat today, with WTI settling near $54.50 per barrel and Brent at $63.40/barrel. The trigger appears to have been a combination of Trump ruling out sanctions against Saudi Arabia, subdued risk sentiment, and a stronger dollar. In precious metals, gold edged lower yesterday after testing the downtrend line drawn from the peaks of May, as a surging dollar rendered the dollar-denominated metal more expensive to buy for investors using foreign currencies.

Major movers: Risk aversion intensifies; dollar outperforms on haven demand

Market sentiment remained in the doldrums for a second session on Tuesday, with sustained weakness in heavyweight tech names – including the likes of Apple (-4.78%) – dragging the broader markets lower, even in the absence of any fresh catalyst or news. Soft earnings and downbeat forecasts by major retailers didn’t help the situation, nor did the renewed carnage in oil prices, which pushed energy shares lower. As is typical in such an environment, commodity-linked currencies such as the loonie, aussie, and kiwi all underperformed, while haven assets such as the yen and Swiss franc saw an influx of demand as investors turned defensive.

Strikingly, the US dollar was the star performer in the session, outshining both the yen and franc as haven buying trumped the recent concerns that the Fed may be set to pause its hiking cycle. The move once again underscores that the greenback is currently an “all weather currency” in the sense that it can shine both in risk-off sessions given its status as the world’s reserve asset, and on risk-on days as wide yield differentials brighten its carry appeal. Separately, after the latest dovish repricing of Fed rate-hike expectations in 2019, the dollar seems more attractive from a risk-reward perspective, as the bar to price out even more hikes – and hence weaken the currency – is probably quite high; it may require concrete evidence of a US slowdown.

In the UK, Brexit continues to dominate, as the testimony by BoE Governor Carney yesterday delivered nothing new. The pound has been quiet as Brexit headlines have taken a break over the past two days; attention remains on whether or not a Tory leadership challenge against May will be triggered, especially in light of the DUP’s support for her government fading.

Elsewhere, the loonie crumbled under the weight of collapsing oil prices, touching a fresh 5-month low against the powerful greenback. The catalyst behind the latest wave of selling in crude was seemingly the US President, who said his nation has no intention of sanctioning the Saudi regime for the killing of journalist Khashoggi, easing worries around supply disruptions. It remains to be seen whether speculation for an OPEC supply cut will be enough to put a floor under prices as we draw nearer to the December 6 OPEC meeting.

Day ahead: Italian budget in focus; US durable goods orders due; tech rout eyed

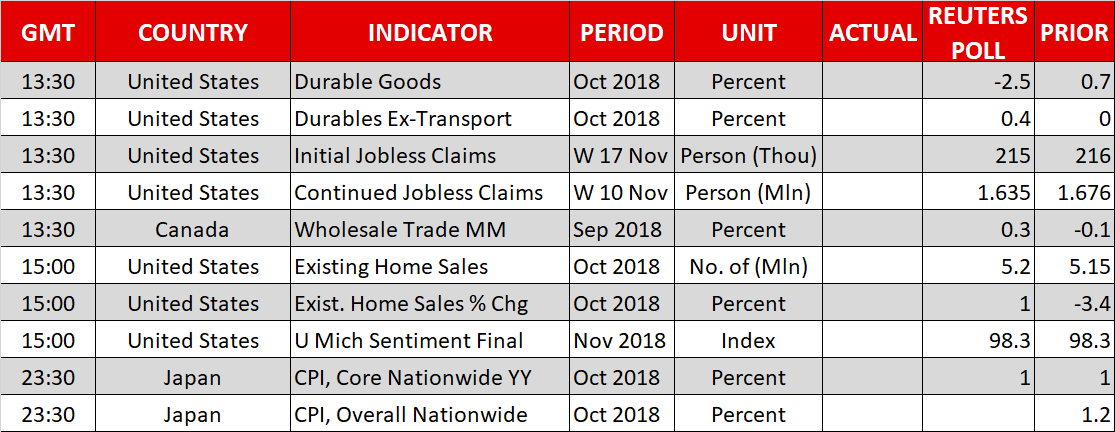

Wednesday’s calendar features numerous releases out of the US, including on durable goods orders. However, perhaps having the greatest capacity to move FX markets will be developments having to do with Italy’s budget, with a European Commission report on the matter due later today. Meanwhile, any headlines on Brexit or the US-China trade dispute will also be attracting interest.

The European Commission will be releasing its report on all eurozone draft budgets later today (around 1100 GMT). The Commission may have no choice but identify Italy as violating the budget rules, which would constitute the first step in the EU’s excessive deficit procedures, something that in turn could theoretically result in fines. The Italian government’s response to the report may prove instrumental in determining the direction in the single currency – a confrontational stance is expected to lead to a weaker euro, and vice versa.

On the data front, monthly data on durable goods orders and weekly jobless claims are due out of the US at 1330 GMT. These don’t tend to move the greenback much, though given some unexpected weakness in recent figures, they’re getting some additional attention. A disappointment could fuel the narrative of a Fed that will slow down its rate normalization plans in 2019, thus hurting the US currency.

Also out of the US will be monthly readings on existing home sales and the University of Michigan’s final survey on November’s consumer sentiment. These will be made public at 1500 GMT. Earlier, Canadian wholesale trade numbers for September are slated for release at 1330 GMT.

On trade, the US Trade Representative’s office accusing China of continuing to support intellectual property theft may be an indication that next week’s meeting between Presidents Trump and Xi at the G20 summit will not provide much of a breakthrough in the trade relations of the two economic superpowers.

In equities, the tech rout that among others saw Apple lose roughly a quarter of its value relative to its October peak is generating interest. Does this provide an opportunity to buy the dip or do the fundamentals justify an extension of the selloff?

After yesterday’s massive decline in oil prices, traders will be paying attention to EIA numbers on US crude stocks due at 1530 GMT. Those are projected to show an inventory buildup of around 2.9 million barrels during the week ending November 16, marking the ninth straight weekly increase, following a rise by approximately 10.3m in the previously tracked week.

Lastly, Japan will be on the receiving end of inflation prints during Thursday’s Asian session (Wednesday at 2330 GMT).

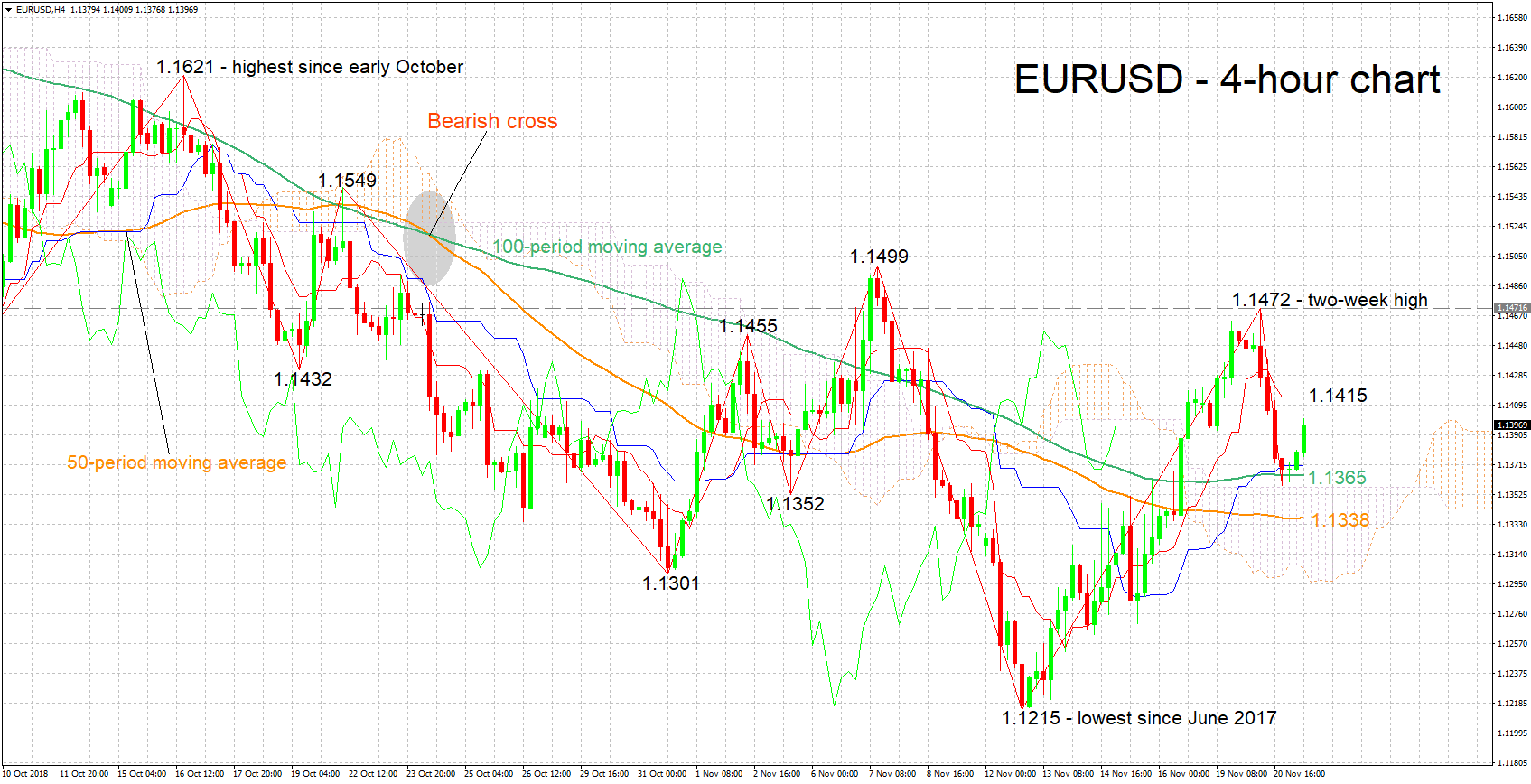

Technical Analysis: EURUSD looks bullish-to-neutral in the short term

EURUSD has retreated a bit after touching a two-week high of 1.1472 on Tuesday. The Tenkan- and Kijun-sen lines remain positively aligned in support of a positive bias in the short term, though they have both flatlined, overall projecting a bullish-to-neutral picture.

An easing of worries over Italy’s budget is likely to see the pair heading higher. Immediate resistance to gains could take place around the current level of the Tenkan-sen at 1.1415. Higher, yesterday’s high of 1.1472 would be eyed; the 1.15 handle lies not far above, while the area around this yesterday’s peak captures a couple of tops from the recent past as well. More bullish movement would turn the attention to the 1.1549 top.

Growing concerns over an EU-Italy clash are expected to exert selling pressure on EURUSD. Support to declines could take place at 1.1365, the 100-period moving average line; the zone around this includes the Kijun-sen (1.1371), the Ichimoku cloud top (1.1357) and a bottom from previous weeks (1.1352). Not far below lies the 50-period MA at 1.1338, while lower still, the 1.13 handle would come within scope – this is also where the Ichimoku cloud bottom is roughly situated.

US data due later on Wednesday can also lead to some positioning on the pair.