Equities sagged and the US surged overnight as the European Central Bank (ECB) spooked global markets by releasing the monetary doves instead of the hounds. European and North American Indices all ended up in the red, on currencies the US dollar Index hit its highest level since June 2017 while bond yields in Europe and the US all fell again.

The ECB left rates unchanged at 0% but was surprisingly downbeat, slashing Eurozone growth forecasts from 1.70% to 1.10%, lowering inflation forecasts with ECB President Draghi bemoaning “pervasive uncertainty” in the global economy. The ECB launched a new round of cheap bank financing and said it would fully reinvest its maturing bond holdings.

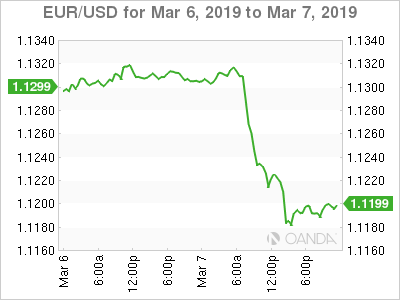

With the Euro-zone likely the next target for President Trump’s trade-talk embrace, a slowing economy, a central bank very low on monetary bullets, an inability by members to mount a joint fiscal response and an impending Brexit by the U.K, it is no surprise that the Euro (EUR) fell out of bed. The single currency fell 1% from 1,1305 to 1.1195, a 20-month low.

The sombre mood flowed into North America with the S&P 500 and Dow Jones falling 0.8% and the Nasdaq 1.1%.

Asia is unlikely to escape Europe’s hangover either following a dismal day on North Asian stock markets yesterday. Local markets will anxiously await China’s trade balance at 1100 am Singapore (USD26.4 exp), followed by German Factory orders (+0.50% exp) before the week’s highlight, the US non-farm payrolls. After last month’s monster 300,000 gain, expectations are more tempered today with the street forecasting 180,000 jobs added. Watch for extensive revisions of the previous months print, with a substantial downward revision potentially holing fragile sentiment below the water line.

FX

The US dollar reigned supreme overnight as haven flows poured into the greenback and onto US treasuries. The EUR dipped below 1.1200 with the pound (GBP) falling 0.7% to 1.3085.

The Australian dollar (AUD), New Zealand dollar (NZD) and Japanese Yen (JPY) all trod water overnight as the news stayed European centric. The China trade data should provide some volatility for all three with sellers emerging on a low print.

The same scenario is likely for regional currencies, with traders likely to reduce holdings on a lower print. Local currencies, in particular, are vulnerable to safe-haven outflows ahead of the weekend.

Equities

Regional stock markets are unlikely to enjoy a happy start to the day with investors likely to see the price action in China, Europe and the US overnight and hit the sell button. We would have expected some lightening of positions anyway ahead of crucial US data and the weekend but overall, the mood will be sombre today.

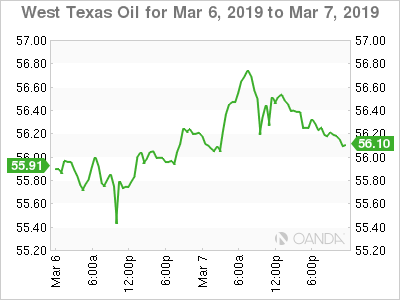

Oil

Brent crude and WTI both traded sideways overnight with oil out of the headlights for now. With attention focused elsewhere, oil seems balanced between OPEC cuts and increasing US shale production, at least in the short term. The world talking itself into a recession has the potential to change that balance materially.