The New Zealand dollar was knocked down in late March when the country’s central bank surprised markets by saying that the next move in interest rates will likely be down rather than neutral. The disappointment following the policy meeting and the lack of clarity about the future of the global economy allowed sellers to take control since then, with the spotlight turning now to NZD inflation to be delivered on Tuesday at 2245 GMT for any new rate signals.

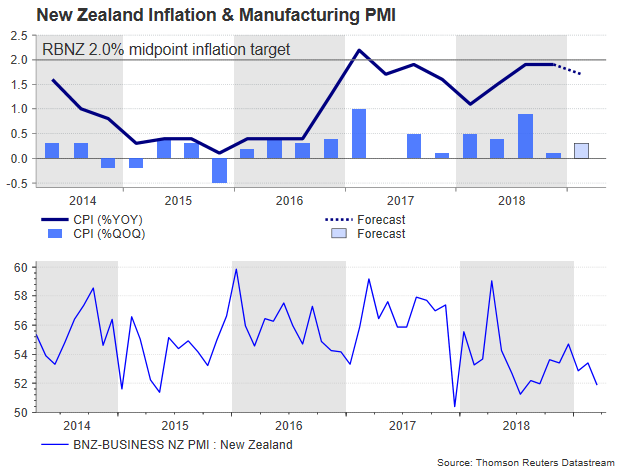

According to forecasts, the headline Consumer Price Index (CPI) for the first quarter of 2019 is expected to have ticked up by 0.2 percentage points to 0.3% on a quarterly basis. Year-on-year however, the gauge is said to have eased to 1.7% after holding steady at 1.9% in the second half of 2018. Such an outcome could boost thoughts that a rate cut might be indeed seriously considered as soon as next month when policymakers gather again to decide on monetary strategy as only a CPI above the RBNZ’s 2.0% midpoint inflation goal would fairly justify higher borrowing costs.

Weaker-than-expected manufacturing and services PMI data for the month of March released last week have already opened the window for a rate cut this year, with the overnight indexed swaps displaying a 27% chance for a 0.25 bps rate reduction in May and almost 80% by November. But a Bloomberg interview with the RBNZ governor Adrian Orr on Thursday brought some confusion to markets after the head of the central bank questioned whether a rate cut is appropriate in May, fueling speculation that policymakers may decide to wait a little longer before taking any action.

Renewed optimism that the US-Sino trade talks are approaching a final lap, and upbeat exports and bank loan data out of China have also forced investors to rethink their rate views this week. A potential solution to trade issues and a sustainable growth recovery in China would brighten the economic outlook for the kiwi economy that is heavily dependent on resource mining and commodity activities, but a domestic rebound would undoubtedly be more precious for the local currency. Hence, while nothing is certain in the outside world yet, investors will closely follow CPI readings this week to predict the RBNZ’s next move.

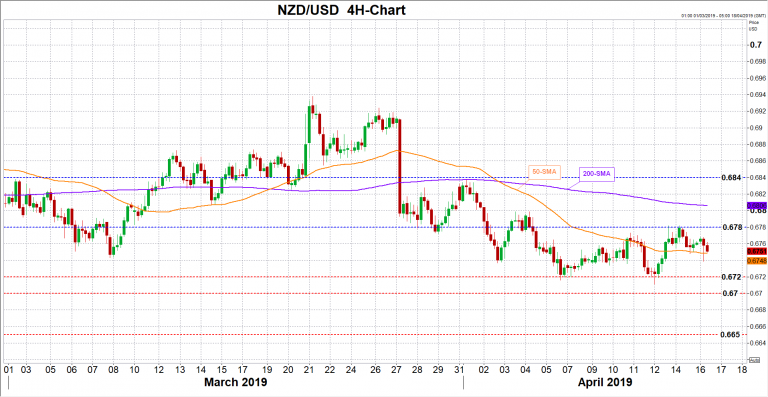

The market reaction could be negative if inflation numbers miss forecasts, with kiwi/dollar probably correcting lower towards 0.6720. Further down, the bears may test the 0.67 handle before meeting support near 0.6650.

In the alternative scenario, a stronger inflation number could help the pair to reach its previous highs around 0.6780, while a bigger surprise may also open the door for the 200-period SIMPLE moving average (SMA) currently at 0.6800. In case of steeper increases resistance could also stretch towards the 0.6840 mark.

Chinese GDP growth figures released a few hours after New Zealand’s inlflation readings could also impact the market.

{kind=link}