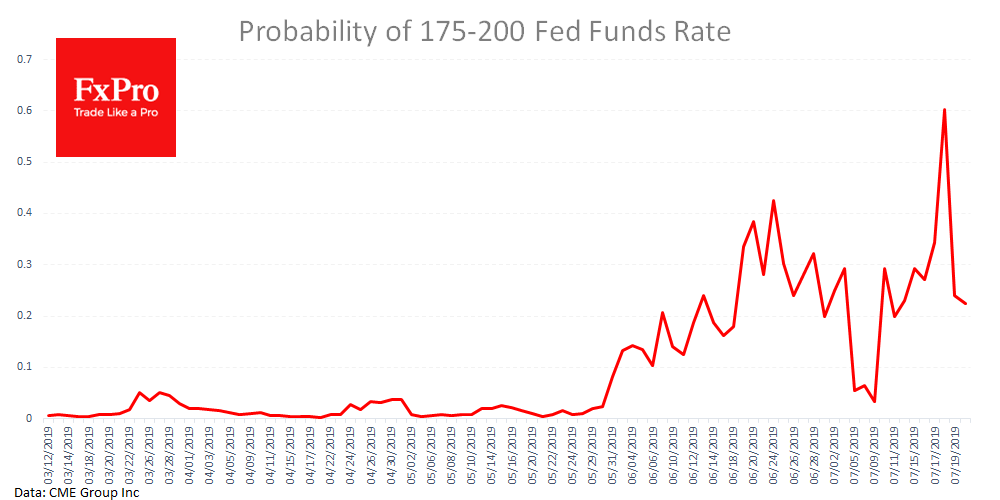

Markets have started the week under pressure. Expectations that the Federal Reserve will cut interest rates by 50 points in July collapsed from 60% to 23%. This occurred after the NY Fed clarified that the speech of John C. Williams was not about the FOMC move at the next meeting. Such a turn is rather positive for the US currency, since there is an opportunity to increase short-term interest rates. Also, the dollar gains additional attractiveness as a safe haven amid the return of tension in the Persian Gulf.

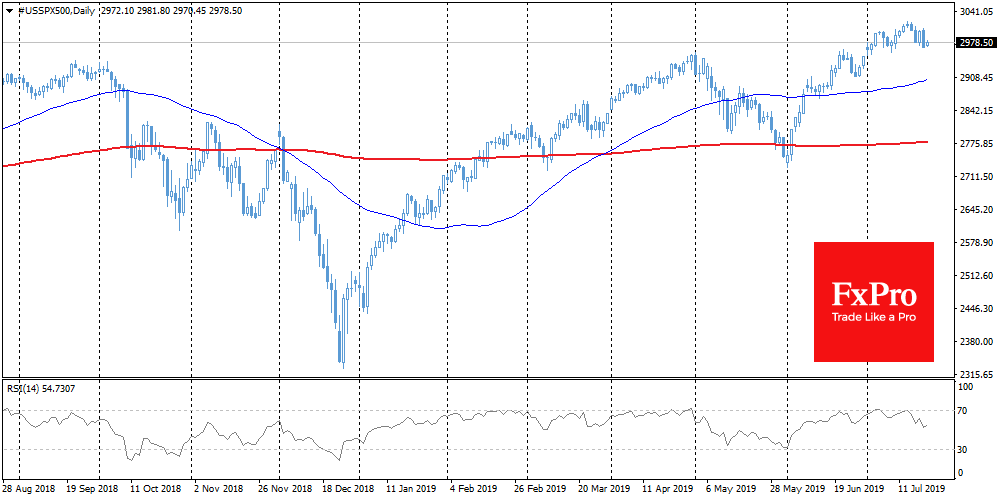

Stocks

The markets’ mood for a less aggressive policy easing triggered a sell-off on stocks. At the end of the previous week, the S&P500 fell by 0.6%, while index futures dropped to two-week lows. Asian markets are mixed, with the Nikkei225 grew by 0.6% after the yen weakened.

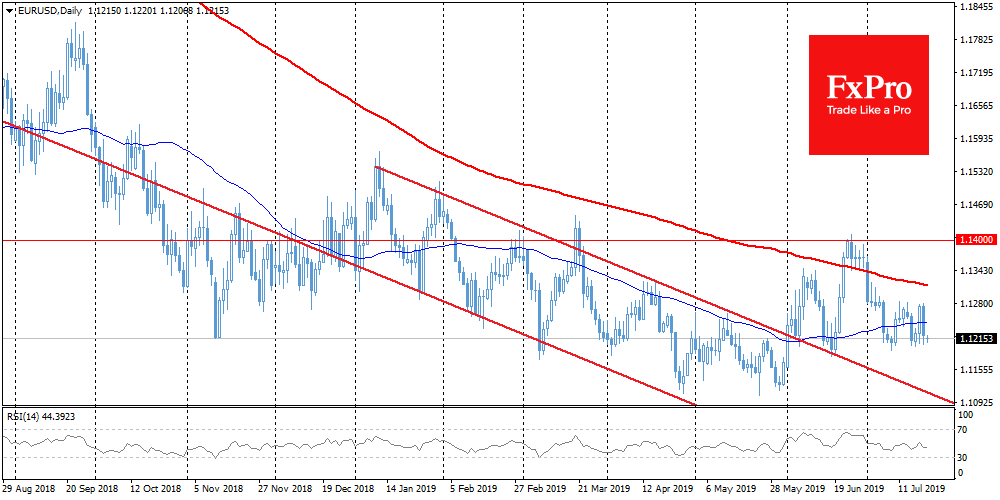

EURUSD

The single currency failed to develop on the offensive, returning to the 1.1200 area. This week, the ECB meeting will be held, from which analysts expect mainly transparent hints of policy easing in September. According to FxPro analysts, in the light of weaker growth and inflation the European Central Bank has many more reasons to act immediately. The risks of an unexpected rhetoric softening look real enough, making the euro potentially vulnerable to a sell-off.

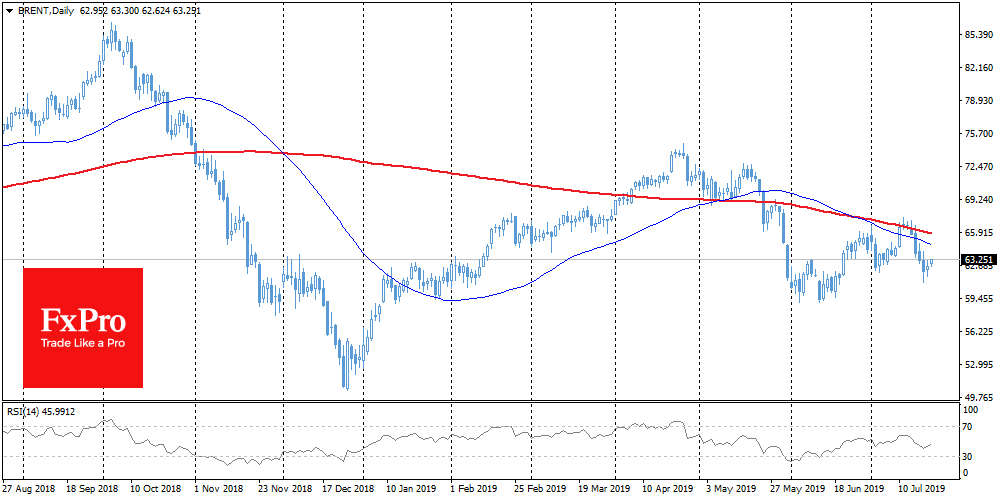

Brent

Oil is back on the agenda amid increased geopolitical tensions, following reports that Iran seized a British tanker. In addition, Libya announced the suspension of work at the largest field. These events brought fears of down-production to the markets, which helped the oil rate to return to growth. On Monday morning, Brent is trading above $63, rising to $61 after Thursday’s slump. However, oil remains below the 50 and 200-day Moving Averages. It is considered to be a bearish signal, suggesting an increase in the chances of further decline.