There isn’t much on the calendar next week other than economic data, so it may be a relatively calm period as a turbulent summer draws to a close. The G7 summit in France could grab some headlines, but markets usually ignore such events. Instead, the focus may fall mainly on any trade news, as the US prepares to unleash new China tariffs on September 1.

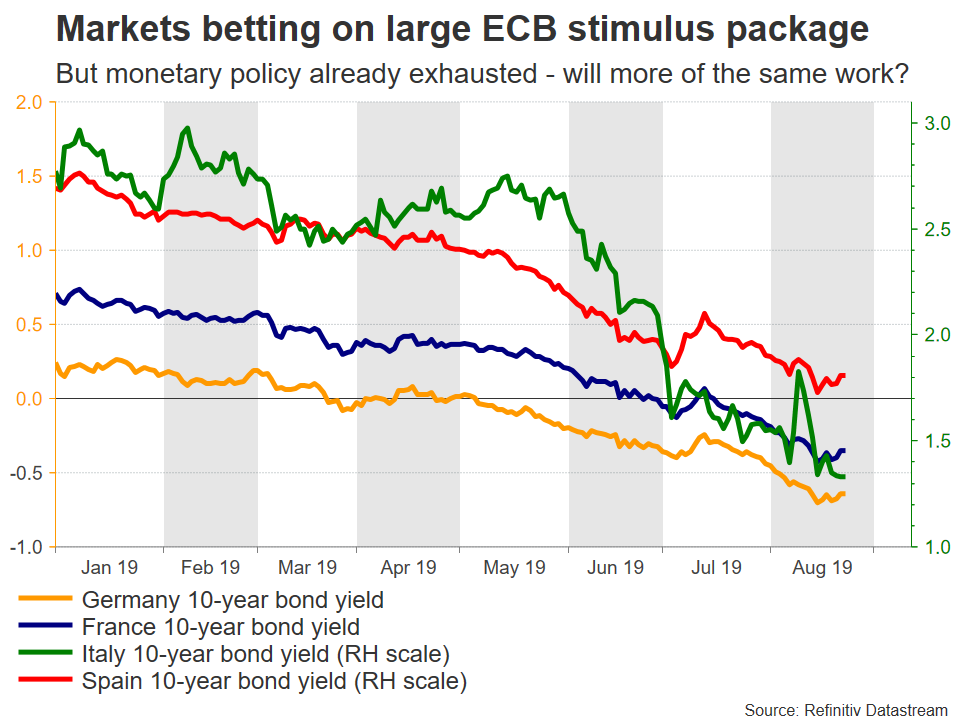

Euro area inflation numbers in sight as Draghi prepares for ‘last act’

In the euro area, the week kicks off with several German releases. The Ifo business survey for August is due on Monday, and investors will look for clues on whether Europe’s largest economy is indeed headed for a technical recession. The final estimate of GDP for Q2 on Tuesday is set to confirm that the economy shrank slightly, while preliminary CPI data for August on Thursday are forecast to show a mild slowdown in inflation.

Attracting more attention will probably be Friday’s flash CPI stats for the Eurozone as a whole. Inflationary pressures have cooled in recent months as the economy slowed, and inflation expectations have also declined dramatically, threatening to drag actual inflation even lower. That is why investors expect the European Central Bank to act with force in September and cut rates deeper into negative territory, as well as launch another round of Quantitative Easing.

As for the euro, the near-term outlook is not bright. The Eurozone – even if it avoids a recession – is slowing down drastically, as global trade tensions take a toll on German exports and worries of a chaotic Brexit hold back business investment. Meanwhile, monetary policy is already exhausted after years of heavy money printing, and any meaningful fiscal stimulus probably won’t be delivered anytime soon. Taken together, these imply that the worst may not be over for the single currency.

G7 summit unlikely to move markets, but risk is to the downside

Staying in Europe, the G7 summit in France will take place over the weekend. Markets typically overlook such events, but in the Trump era, there is always scope for surprises. Last year, the US President stormed off before the meeting finished, and refused to sign the joint statement. He also threw some ‘jabs’ at the Canadian PM, who he was trying to pressure into renegotiating NAFTA, threatening Canada with tariffs.

While this gathering may not be as eventful, the risks are clearly tilted towards an escalation in trade tensions – but this time with Europe. Trump has threatened Brussels with car tariffs multiple times, and there is a small risk that he doubles down on those warnings when he meets the European leaders in person. If so, risk appetite would probably take a hit and stock markets could open with gaps lower on Monday, while haven currencies like the yen and franc extend their recent gains.

Upcoming US data unlikely to dissuade Fed from September rate cut

In America, there’s a slew of potentially key data on the agenda. Durable goods orders for July are out on Monday, before the second estimate of GDP for Q2 will hit the markets on Thursday. Personal income and spending data, as well as the core PCE price index for July, will all be released on Friday.

While these are all important indicators, they are unlikely to be a game changer for the dollar, as a Fed rate cut in September is practically a done deal. Even if these figures are stellar, the central bank is still certain to slash rates next month, as it tries to safeguard the US economy from the negative effects of trade tensions. Indeed, the Fed has made it clear it’s not cutting rates because the economy is in trouble, but rather so it doesn’t get into trouble in the first place.

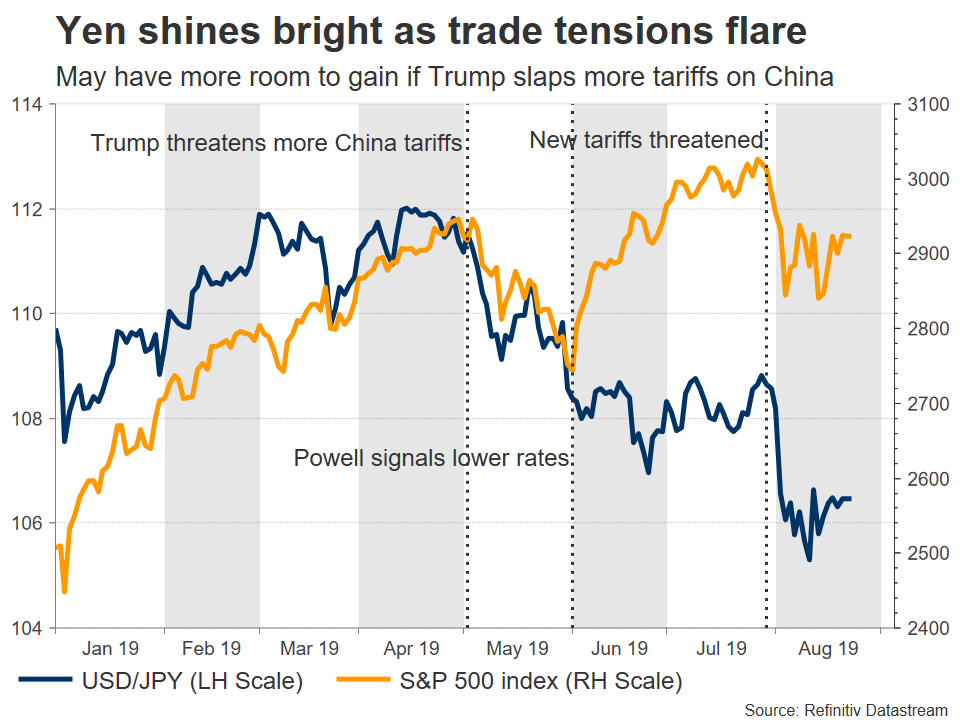

Therefore, the most crucial factor for how aggressively the Fed will act may be whether the White House proceeds with slapping new tariffs on China on September 1. Judging by Trump’s raise-the-stakes negotiating style, further escalation is very likely, and Beijing will be forced to retaliate. Such an outcome may drag the dollar lower, but only against haven currencies like the yen and franc, not versus risk-sensitive assets like the aussie and kiwi.

Raft of Japanese figures due, but risk appetite more important for yen

The world’s third-largest economy will see the release of multiple indicators on Friday, including the forward-looking Tokyo CPIs for August, and July’s employment data. As usual though, the yen is unlikely to react to economic data.

Instead, the best-performing currency of 2019 will probably be driven by any changes in global risk sentiment. In that sense, another round of escalations in trade tensions seems imminent, if not this week at the G7, then next weekend when Washington introduces fresh tariffs on Beijing. At this point, the only factor that may be able to stop the yen from gaining more ground – outside of a trade deal – would be clear signals for more easing by the Bank of Japan.

Even then though, it’s questionable whether this would be enough for a trend reversal, as the Bank’s policy ammunition box is very limited after years of extraordinary stimulus measures.

Australian capex and Canadian GDP also on the docket

Turning to the commodity-linked currencies, Australia’s capital expenditure for Q2 is coming out on Thursday, and forecasts point to a rebound. If so, that could dispel some expectations for more RBA rate cuts this year, and perhaps help the battered aussie recover some losses. That said, the currency’s overall fortunes are linked to the trade war.

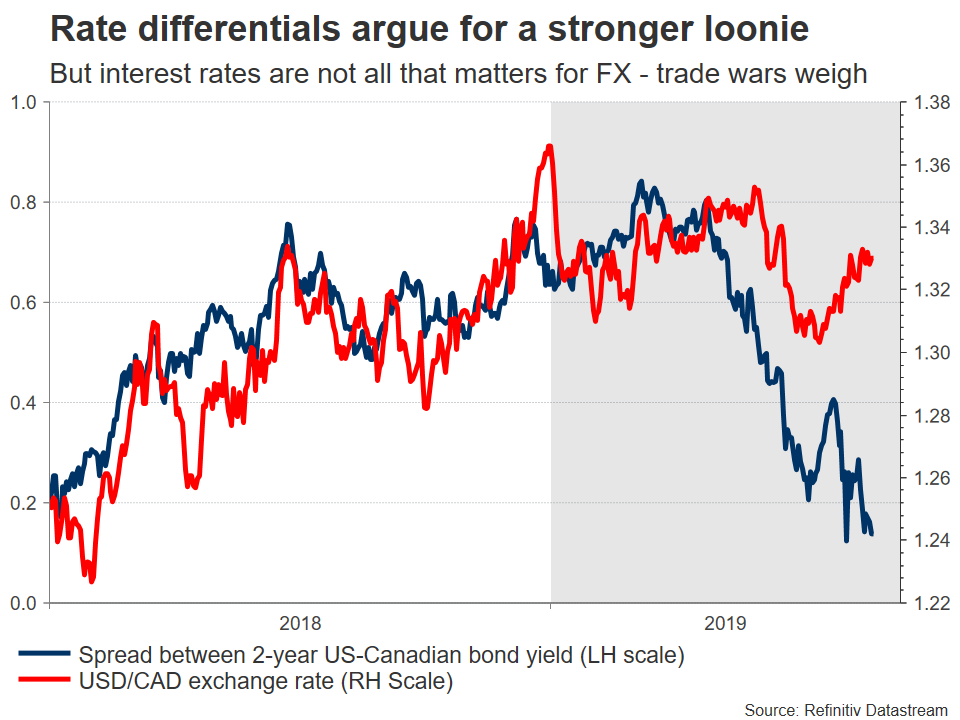

In Canada, GDP numbers for Q2 are due on Friday. While the Canadian economy remains solid, the loonie has been losing ground in recent weeks, as markets started having doubts on whether the BoC will actually stay neutral in an environment where every other central bank is adding stimulus. The escalating trade war has also left its marks on the currency, and the outlook seems to be turning bleak, as the BoC may indeed put rate cuts on the table before long.

{kind=link}