Highlights

- With interest rates at near record lows in major advanced economies and signs of a deteriorating global outlook, there are concerns that central banks have limited room to provide stimulus in the event of a recession.

- Central banks will need to consider a wider scope of policy options than in past downturns. Negative policy rates combined with asset purchases and forward guidance will play a prominent role in easing monetary conditions. That said, major central banks will tailor the implementation of these policies according to local economic conditions and the health of the domestic banking sector.

- There are limits to what can be achieved by monetary policy measures alone. Reducing interest rates deeper into negative territory will have diminishing returns and at some point become counterproductive in providing additional stimulus.

- Fiscal policy will be called upon to do most of the heavy lifting, especially in Japan and the Euro Area where central banks have gone deeper in the monetary policy toolkit.

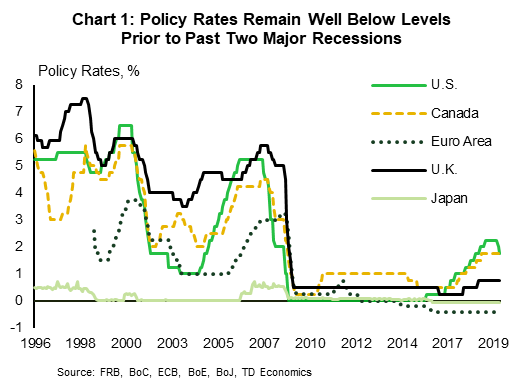

The global growth outlook has deteriorated amid heightened uncertainty surrounding trade and geopolitical tensions. This has occurred even though monetary policy settings in the U.S., the Euro Area, Japan, Canada and the UK are highly stimulative. Policy rates in these five regions sit well below levels at the onset of the past two major recessions (Chart 1). During prior cycles, central banks were able to respond aggressively to signs of a downturn with a rapid series of rate cuts. In the case of the U.S., the fed funds target rate was reduced by 550 bps over the course of 2001 downturn and by 525 bps over the course of the downturn that began in 2007.

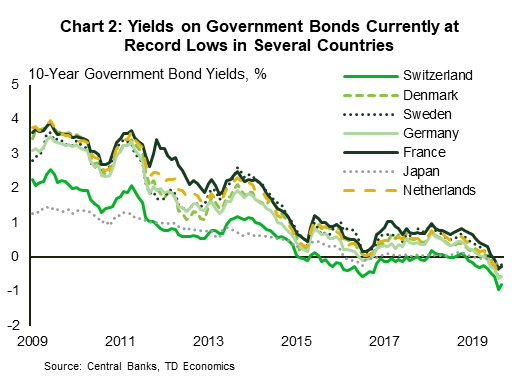

Today, rate cuts of this magnitude are not an option should a major downturn materialize. This is of particular concern in the Euro Area and Japan where policy rates are already negative. The Bank of Japan (BoJ) and the European Central Bank (ECB) will continue to rely on unconventional channels to ease monetary conditions. The BoJ and the ECB have been able to reduce interest rates to record lows through a combination of negative policy rates, asset purchases and forward guidance (Chart 2). So far the transmission mechanism has been largely effective, but there are limits to what can be achieved through such measures. Reducing interest rates deeper into negative territory has diminishing returns and will become counterproductive at some point.

The U.S. Federal Reserve (the Fed) and the Bank of Canada (BoC) have some scope to cut rates, but they too would be faced with providing further stimulus through unconventional channels in the event of a major downturn.

How much lower can policy rates go?

The European experience over the past few years (Appendix Box 1) has provided an opportunity to improve our understanding of how the bank lending channel operates in a prolonged, negative interest rate environment.

In a positive interest rate environment, the outcome is straightforward. Policy rate cuts are transmitted by the banking sector through lower lending and deposit rates. In a negative rate environment, the outcome carries greater complexity. The economic transmission linkage can become muted or break down altogether. Reducing deposit rates below zero would give businesses and households an incentive to substitute to cash, eroding banks’ deposit base and the primary source of funding for the banking system.

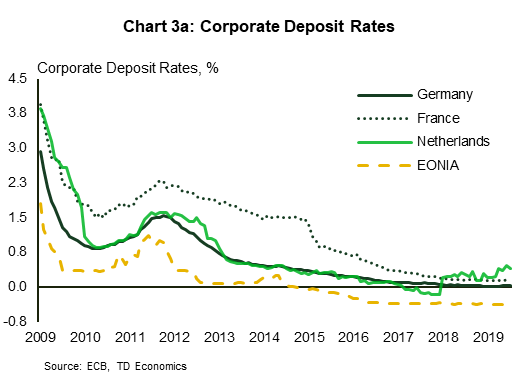

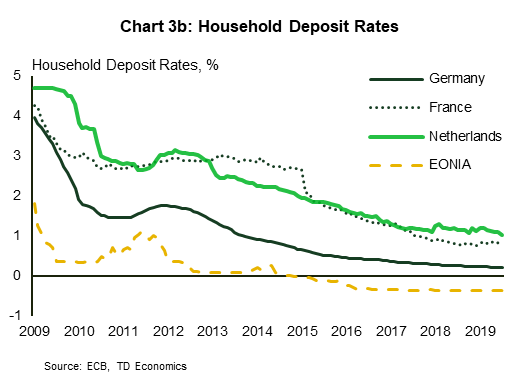

Europe’s experience offers some comfort that banks rarely reduce retail (household and small business) deposit rates below zero. Some Euro Area banks have “charged” interest rates on large corporate deposit accounts, but to a limited degree.1 Deposit rates are nonetheless at record lows throughout most of Europe. In Germany, corporate and household deposits currently earn just 0.03% and 0.22%, respectively as of this past July (Charts 3a and 3b), while banks can borrow and lend on the interbank market overnight at close to -0.4% (shown by the Euro overnight index average EONIA).

While the economic transmission may face little direct friction through this path, there is an indirect mechanism at work. Net Interest margins are squeezed as banks pass policy rate cuts through to lower lending rates while maintaining deposit rates at the zero floor. The deterioration in profitability could require capital-constrained banks to curtail lending, which would offset the intended expansionary impact of lower interest rates.

Empirical studies generally support the widely-held view that very low interest rates reduce net interest earnings.2 The more contentious issue is how this constraint affects bank profitability and lending. In sum, lower net interest margins can be offset by higher fee income and lower deposit and wholesale funding costs.

The line of research that has focused on bank profitability indicates that the “ultra-low” or negative interest rate environment in Japan and Europe had a benign effect on bank profitability. The Riksbank concluded that the low interest rate environment had “no unequivocal effect on banks’ profitability” by pointing to the contradiction of low bank profitability in the Euro Area versus high profitability in Sweden.3 One widely-cited paper found that lower net interest earnings are wholly offset by higher non-interest income and lower deposit expenses.4 Other studies have found the offset coming through lower wholesale funding costs and higher fee income.5

A closely related line of research focuses on whether banks modify their risk appetite in a negative interest rate environment. There is ample evidence that financial institutions (and investors more generally) respond to ultra-low/negative returns on “safe assets” by taking on riskier investment strategies. There is some evidence that banks adopt such “search for yield” behavior to compensate for waning profitability. An empirical study by Basten and Mariathasan (2018) found that Swiss banks have been able to offset squeezed net interest margins by raising fees and taking on higher credit and interest rate risk.

Diminishing Returns Kick In

Other research has focused on how diminishing returns materialize as rates are cut deeper into negative territory. Banks may be able to offset squeezed interest margins at moderate negative rates, but there are limits to how much revenue can be raised from non-interest sources and how far expenses can be reduced. The ability of banks to substitute from deposit to wholesale funding and take on more interest rate and credit risk is constrained by regulatory requirements and their internal risk appetite. To the extent that banks are able to preserve profitability by maintaining loan margins, reductions in policy rates would not result in lower borrowing rates for households and businesses. The intended expansionary impact of lower policy rates would not then be transmitted through the bank lending channel.

A good example is provided by Eggertsson et al. (2019) who found that when the Riksbank cut the policy rate to -0.25%, lending rates declined in tandem. But, when the policy rate was cut further to -0.50%, lending rates hardly declined.6 The passthrough from negative policy rates to lending rates was found to be especially low for banks that are highly dependent on deposits for funding, since they would benefit less from lower wholesale funding costs.7 As negative policy rates decline, these banks become less willing to reduce interest margins. In other words, their lending rates decline by less than banks with low deposit bases, subsequently leading to a loss in market share. Profitability is subsequently undermined and the pass through from policy rates to lending rates gets weaker. Further cuts beyond some point would have no impact on lending rates, making the bank lending channel ineffective.

Where is the limit set?

There is no consensus on the point at which negative policy rates begin to disrupt the bank lending channel. Several factors are at play, many of which vary across countries. Countries where banks are heavily dependent on deposits for funding are more vulnerable, as are countries where the non-financial sector is more reliant on bank financing. Economic structure is also important. For example, the exchange rate plays a prominent role in the monetary policy transmission mechanism in small, open economies. Policy rate cuts accompanied by an exchange rate depreciation provides additional stimulus through the trade channel, offering some offset to the disruption in the bank lending channel.

The operational framework of monetary policy can also play a role. Central banks in Denmark, Sweden, Switzerland, Japan and the Euro Area have implemented a tiered system for reserve remuneration to reduce the cost of holding reserves in a negative policy rate environment.8 This is of importance in countries where central banks have implemented negative policy rates in conjunction with large scale asset purchase programs (Japan in particular). In the absence of a tiered system, asset purchases would essentially act as a tax on the banking sector by raising interest payments on excess reserves.

Central banks can also mitigate the impact of negative policy rates on bank profitability by providing banks with more favorable financing. The ECB introduced targeted longer-term refinancing operations (TLTROs) in 2014 that offered financing terms 10 bps above the rate on main refinancing operations. In September 2019, a third series was announced with even more favorable financing terms (as low as the average deposit facility rate over the life of each operation, which is currently -0.50%).

TLTROs provide participating banks with more favorable financing than what is available from other sources (mainly deposits and wholesale financing). There is also an indirect channel – as participating banks reduce their financing needs from conventional sources, funding costs decline for the banking sector. Analysis by the ECB indicates that TLTROs have reduced funding costs for banks across the Euro Area, successfully increasing lending in vulnerable countries where banks were experiencing financial pressures.

Taken to the logical extreme, there is no limit to the extent to which central banks could provide such funding. A central bank could set interest rates on excess reserves and provide direct funding to ensure that the bank lending channel operates effectively in a negative interest rate environment. However, such measures would deplete the central bank’s equity. In theory, central banks can operate as viable institutions without equity (as issuers of fiat money). In practice, conventions govern central banks’ equity and risk exposures (in part to help maintain central bank independence on formulating monetary policy).

What other policy options are open to central banks?

As already demonstrated through various central bank programs, negative policy rates are but one of the unconventional tools that central banks have adopted. Experience has shown that asset purchase programs and forward guidance can also enhance the expansionary economic impact of lower policy rates.

Asset purchase programs will play a more prominent role in setting monetary conditions

The Fed, ECB, and Bank of England introduced large-scale asset purchase programs (also known as “quantitative easing”) in the aftermath of the global financial crisis (Appendix Box 2). The motivation at the time was to quell the panic and alleviate the risk of a financial meltdown. Over time, asset purchase programs have been undertaken to meet broader objectives, such as addressing weaknesses in the monetary policy transmission mechanism and influencing monetary conditions more generally.9

The Bank of Japan began experimenting with asset purchase programs in the late 1990s. Economic growth has since been anemic, with inflation well below the target. The massive scale of the BoJ’s QQE program in April 2013 was followed by a marginal improvement to the economic and inflation outlook. The counterfactual scenarios could have been much worse. Yet, one can conclude that asset purchase programs alone cannot provide the stimulus needed to support a robust recovery under any circumstances (especially if the root causes of anemic growth have important structural elements).

Even on a smaller scale, there is no consensus on the potential benefits of asset purchase programs. Reviews of the vast empirical literature conclude that QE1 in the U.S. reduced the 10-year US Treasury yield by between 35 to 123 bps.10 More importantly, there is high uncertainty about how long the impact persisted. Skeptics argue that those estimates capture the immediate announcement effect, which dissipates over time.11

There is also a debate about the underlying transmission mechanism. One view is that large-scale asset purchases bid up bond prices by increasing demand. This should be observable in financial markets where risk-free assets are in short supply and a significant portion of the investor base has a “preferred habitat” (in part due to regulatory requirements and maturity matching objectives). U.S. Treasuries were not in short supply when QE1 was implemented. On the contrary, public sector borrowing requirements outstripped Fed asset purchases by a wide margin – the Fed purchased only $300 billion of $1.5 trillion in net Treasury issuance in 2009.

Forward guidance can help reduce longer-term interest rates

An alternative view is that asset purchase programs are effective in reducing interest rates primarily through forward guidance. Asset purchase programs typically include a fixed schedule for making purchases that is not conditional on future developments. The unconditional nature of the program serves as a commitment device that enhances the creditability of the central bank’s commitment to keep the policy rate “lower for longer” even if economic conditions were to improve sooner than expected. The supply of government bonds does not play a role in the forward guidance channel. Hence, a debt-financed fiscal stimulus package (increasing the supply of government bonds) would not curtail the effectiveness of an asset purchase program.

Other studies focus on the so-called portfolio rebalancing channel. According to this view, asset purchases reduce yields on “safe assets” (government bonds in particular) to induce investors to shift to riskier investment strategies, which entails taking on more risk. Such “search-for-yield” behavior has potential implications for financial stability, an issue we return to later in the paper.

Forward guidance on an asset purchase program is one means to lower yields. Another, often used in parallel, is to anchor down market expectations for the policy rate in order to influence lower yield curve expectations. This is particularly important when the policy rate is constrained at the lower bound. A key aspect of central banks’ communication strategy is to convince financial markets that the policy rate will be “lower for longer”, with the aim of reducing longer-term rates.

One strategy involves issuing explicit policy statements on the future path of policy rates. The best example is the FOMC target fed funds rate projections that provide an explicit time path for the fed funds rate as well as dispersion across participants. Other central banks rely on statements that are less explicit and hence more open to interpretation. For example, the July 2019 ECB monetary policy decision laid out a timeframe:

- “The Governing Council expects the key ECB interest rates to remain at their present or lower levels at least through the first half of 2020, and in any case for as long as necessary to ensure the continued sustained convergence of inflation to its aim over the medium term.”

This was followed by the September (2019) decision conditional on an outcome:

- “The Governing Council now expects the key ECB interest rates to remain at their present or lower levels until it has seen the inflation outlook robustly converge to a level sufficiently close to, but not below, 2%…”

The ECB’s communication strategy underlying both decisions provided financial markets with guidance on the sense in which policy rates will be “lower for longer”. The shift from a time-dependent to an outcome-dependent commitment served to inform markets on how they were managing the risks surrounding the medium-term projection.

In the case of the latter, market reaction was subdued. This was in part because less stimulus was announced than expected. However, it may also be the case the ECB is starting to come up against diminishing returns with regards to this policy tool, which only time will tell.

This general approach to forward guidance operates primarily through the so-called “Delphic channel”. Explicit policy statements can be effective in so far as the central bank is communicating new information about future developments that then gets incorporated into financial markets (serving as the Oracle of Delphi). However, they have little impact through the “Odyssean” channel – policy statements which do not commit the central bank to a future course of action (unlike Odysseus who bound himself to the mast of his ship).12 Financial markets expect the central bank to raise the policy rate earlier than planned if economic conditions were to improve significantly.

The yield curve control policy introduced by the Bank of Japan in January 2016 is an example of a commitment device that binds the central bank. The BoJ stands ready to purchase Japanese government bonds so that the 10-year yield remains at “around zero percent”. The commitment reduces the risk of a capital loss on long-term bonds due to interest rate risk, resulting in lower yields.

Longer-term rates are influenced in part by the probability that policy rates may be constrained by the lower bound at some point in the future. Central banks have an incentive to make explicit policy statements on the effective lower bound pre-emptively, rather than waiting until policy rates reach zero. Central banks in the U.S., Canada and the UK have analyzed the feasibility of negative policy rates. Only Canada has yet to make official statements on whether negative policy rates would be adopted should circumstances warrant. Recent statements both by the Fed and the Bank of England dismiss the idea of negative interest rates of being deployed as a tool in the next downturn. That said, this issue would likely play a prominent role in monetary policy discussions in all three countries during the next major economic downturn.

Examining modifications to inflation targeting frameworks

Much of what has been discussed is already in play in some form among various central banks. To address possible limitations on the persistent use of these approaches, central banks are exploring how inflation targeting can be adapted to enhance the effectiveness of monetary policy when the policy rate is at the lower bound. One option sparking interest is the adoption of a temporary price level target.13 In its simplest form this would entail the monetary authority committing to maintain accommodative conditions until a predetermined level on the price index is achieved (as opposed to the percent change in the price level). The mechanics of this would maintain a defined target for growth, say 2% per year. But, inflation outcomes below 2% during the early disinflationary phase of the downturn would then have to be offset by a period above 2% in order to return to a designated price level. This would allow market participants transparency on a “lower for longer” policy rate. By contrast, an inflation growth-target treats “bygones as bygones” and hence, the monetary authority begins to unwind its accommodative stance once inflation reaches 2%.

What can we expect in the event of a major downturn?

This answer varies depending on the region. The scope on monetary policy within the ECB and BoJ is more limited than in the U.S., the UK and Canada.

ECB cut its deposit facility rate by 10 bps on September 12th (to -50bps), suggesting there is likely less scope on the downside before diminishing returns and unintended consequences come into play. The September meeting also brought in further details on the third series of TLTROs, and an open-ended asset purchase program amounting to €20bn per month. Concerns have been raised that the ECB’s holdings of government bonds issued by Germany, Portugal and Finland are approaching the (self-imposed) limit of 33%. While this might be an issue at the current juncture, it is unlikely to be a binding constraint in the event of a major downturn. The ECB could waive its right to veto a debt restructuring offer on all its holdings of Euro Area sovereign bonds if circumstances warrant further easing.

In contrast, Japan’s experience with a low interest rate/inflation rate environment over the past 20 years serves to demonstrate the limitations of implementing monetary policy through unconventional channels.14 The risk of deflation remains an ongoing concern. Core CPI in July (the most recent data available) registered a 0.6% year-on-year increase, which is up from a mild deflation experienced in late 2017, but well below the 2% target.

The ultimate message is that already low monetary settings and the persistent use of other unconventional tools today suggest that both the Euro Area and Japan will need to rely more on fiscal policy in the event of a major downturn. Countries able to implement a credible medium-term fiscal stimulus plan in a timely manner are more likely to build the confidence needed to support a robust and sustainable recovery. Countries already burdened with high public debt levels will likely face a difficult challenge in this regard, potentially leading to an extended period of low economic growth or recession dynamics. That’s because an ambitious fiscal stimulus package could raise concerns about long run debt sustainability (not to mention domestic political concerns about intergenerational equity). This is of particular concern in Japan where net general government debt is currently at 153% of GDP, and to a lesser extent in Euro Area countries with elevated debt levels.

The wide variation in public debt levels across the Euro Area could lead to a two-speed recovery. Financing conditions in countries such as Italy, where net general government debt is currently close to 120% of GDP, could come under severe pressure if the government were to propose an ambitious fiscal stimulus package in the absence of a credible medium-term fiscal plan. At the other extreme, moderate public debt burdens in Germany, Finland and the Netherlands give policymakers more leeway to implement a major fiscal stimulus plan without undermining market confidence.

Central banks in the U.S., Canada and the UK have time to prepare

Central banks in all three countries still have room to reduce policy rates before having to take a stance of the effective lower bound. As mentioned earlier, making a pre-emptive policy statement on their willingness to implement negative policy rates would serve to ease monetary conditions. Asset purchase programs would be tailored to the circumstances, with the overall design of the programs (the total amount and composition of sovereign and corporate debt and equity purchases) largely determined to address weaknesses in the monetary policy transmission mechanism.

In some cases, this might require legislative changes to give central banks the mandate to purchase risky assets. In the case of Canada, the zero reserves system would need to be modified to accommodate asset purchases and negative interest rates.15 Experience has shown that legislative changes along such lines are made when circumstances warrant – desperate times call for desperate measures. For example, in the U.S. the policy on paying banks interest on reserves, originally scheduled to come into effect in October 2011, was introduced in October 2008 to “address conditions in credit markets”.16 However, the effectiveness of monetary policy would also need to be enhanced by fiscal policy. Having more room on monetary policy than the ECB and BoJ doesn’t mean having ‘lots of room’. Every country is starting from a lower base than prior episodes of recessions, offering less economic impulse from this channel alone.

Beyond the next downturn

As the old economic adage goes: there is no such thing as a free lunch. Persistently low and/or negative rates has already raised concerns about excessive risk taking. As an intuitive example, yields on Greek sovereign debt are currently below those on U.S. Treasuries despite having a non-investment grade rating and a public debt burden exceeding 180% of GDP. There are even a few examples of “high yield” corporate bonds currently trading with negative yields. These anomalies raise concerns that a further or prolonged “ultra-low” interest rate environment may have unintended consequences for financial stability. Assessing vulnerabilities to safeguard financial stability should play a prominent role in policy discussions.

The series of TLTRO programs adopted by the ECB is another case in point. Providing banks with more favorable funding could have unintended consequences. Bank’s cost of funding from market sources reflects their risk profile and risk appetite, which can vary greatly across institutions and over time particularly during periods of stress. It is not clear how (and if) central banks could provide financial institutions with similar incentives to limit their risk appetite.

The portfolio rebalancing channel underlying asset purchase programs also merits careful consideration. A prolonged, “ultra-low” interest rate environment gives banks incentives to take on riskier funding, investing and lending strategies. As noted earlier in this paper, recent empirical evidence already indicates Euro Area banks are exhibiting “reaching for yield” behavior in response to the negative interest rate environment.17 While there are regulatory constraints on how far banks can move in this direction, one should keep in mind why the regulator requirements were adopted in the first place. The net stable funding ratio introduced by the Basel Committee on Banking Supervisory in 2014 (an element of “Basel III”) was designed to reduce the risk that banks encounter a disruption in funding during periods of stress.

A prolonged ultra-low interest rate environment also raises financial stability concerns in other segments of the financial system, notably insurance companies and pension funds. A lengthy period of underperformance in investment returns would cause funding pressures for businesses with defined benefit pension plans. Moreover, it can create strong incentives for businesses to migrate to defined contribution plans, or perhaps reduce pension offerings within the private sector altogether.

On the fiscal policy front, public debt burdens in several countries have not recovered to lower levels prior to the global financial crisis, now ten years in the past. For most countries, this does not preclude a fiscal stimulus plan in the event of a major downturn. But clearly, the ratcheting up of public debt levels cannot continue indefinitely. At some point, concerns about debt sustainability will be a limiting factor. In cases where there’s a collision of limitations on both fiscal and monetary policy options, inflationary finance (i.e. helicopter money, modern monetary theory, standard emergency fiscal facility) would likely gain some popularity and could be the last resort, that is for countries not in a currency union.

Bottom Line

With interest rates are at near record lows in major advanced economies, monetary policy will not be able to provide the amount of stimulus as in past downturns. All policy options will be on the table in the event of a major downturn. Central banks will experiment with negative interest rates, asset purchases and forward guidance to explore the limits of easing monetary conditions through unconventional channels. Recognizing that such measures have diminishing returns, fiscal policy will ultimately dominate policy discussions.

End Notes

- Around 20% of corporate deposits in the Euro Area currently have negative rates, with about 50% of corporate deposits in Germany facing negative deposit rates (Altavilla et al. 2019).

- Borio, Gambacorta and Hofmann (2015).

- Riksbank (2016).

- Lopez, Rose and Spiegel (2018)

- Turk (2016).

- Erikson and Vestin (2019) found that when the policy rate in Sweden was reduced to -0.5% there was complete passthrough to lending rates for businesses but not households.

- Eggertsson et el. (2017) and Heider et al. (2018).

- The Danmarks Nationalbank limits the amount that individual banks can hold in current accounts (which current incur an interest rate of zero); The remainder of commercial banks’ assets are held in certificates of deposit which currently have an interest rate of -0.65%.

- Appendix II provides a detailed account of the objectives underlying asset purchase programs.

- Borio and Zabai (2016, Table 4) and Kuttner (2018, Table 2).

- Greenlaw et el (2018).

- The Delphic / Odyssean dichotomy of forward guidance was introduced by Campbell et al (2012).

- Eberly, Stock and Wright (2019).

- The Bank of Japan reduced the overnight rate to close to zero back in early 1999. Core CPI inflation has not exceeded 1% since early 2016.

- Asset purchases by central banks create excess reserves (the liability counterpart on the central bank’s balance sheet). The zero reserves system currently in place in Canada has no facility to pay/charge interest on excess reserves.

- Board of Governors of the Federal Reserve System press release, October 6, 2008.

- Bräuning and Wu (2017), and Demiralp et al. (2019).

Appendix Box 1:

Central banks have adopted negative policy rates under diverse circumstances

Taking a walk down memory lane, there were legitimate concerns within the central bank community that negative interest rates could disrupt financial market operations amid the high volatility and heightened uncertainty during the financial crisis (Appendix 1 goes through detailed timeline of negative interest rates). The Federal Reserve reduced the fed funds rate to the “zero lower bound” (the 0 to 25 bps target range) in December 2008, yet disinflationary pressures continued to intensify. The unemployment rate reached a peak of 10% in October 2009, with core PCE inflation hovering dangerously low at around one percent. Conventional monetary policy rules indicated that reducing the fed funds rate well below zero would have been appropriate in this circumstance.

Back then, it was unclear how legal contracts referencing interest “payments” would be interpreted and enforced. The existing legislation governing interest on reserves (the Financial Services Regulatory Act of 2006) refers to Federal Reserve Banks making interest payments but not receiving interest payments. Reducing the interest rate on excess reserves below zero would therefore require legislative changes. Financial systems were set up to process bond coupon payments from borrowers to creditors, but not the reverse. Negative interest rates could have created havoc with IT systems, especially if the transition was done on short notice.

There were also concerns that negative interest rates would distort the asset holdings of commercial banks, which could show a preference to hold currency rather than pay interest on their reserves held at the central bank. As major participants in large interbank payment systems, banks are willing to pay for the convenience of settling via accounts with the central bank. It was unclear how low the discount rate could go before substitution to currency became a viable option and began to undermine the ability of the Fed to maintain short-term interest rates below zero over a prolonged period.

Finally, there was some uncertainty about whether monetary policy operations and linkages to the financial system would function effectively in a negative policy rate environment. This was perhaps the biggest issue of all that held back many central banks from experimenting with negative policy rates during the 2009 crisis when the aim was to stoke a recovery by rebuilding a banking sector that had been ravaged by the financial crisis.

What has changed?

Since then, financial institutions, regulators and policymakers have had time to address these concerns. Financial institutions have been able to test how their accounting and IT systems would function in a negative interest rate environment. In particular, the 2016 DFAST/CCAR stress testing exercise included a supervisory scenario with negative interest rates (the 3-month U.S. Treasury yield declined to -0.5%), which enabled regulators to assess the performance of risk management models.

Central banks in Europe and Japan have been experimenting with negative policy rates over the past decade. Denmark became the first country to explore negative policy rates in mid-2012, followed by the ECB in June 2014, Switzerland in January 2015, Japan in January 2016 and Sweden in February 2016. The decision to reduce policy rates below zero was made under diverse circumstances in each case (Appendix I), but their experiences demonstrate that monetary policy operations and linkages to the financial system can function effectively in a negative rate environment over a prolonged period.

Central banks in each region have been able to reduce short-term market rates below zero over a prolonged period. In the case of Switzerland, the yield on 3-month treasury bills has fluctuated between -0.75% to -1.25% since January 2015. Their experiences also provide insight into the limitations of reducing policy rates further into negative territory.

Appendix Box 2:

Asset purchase programs have been tailored to the circumstances

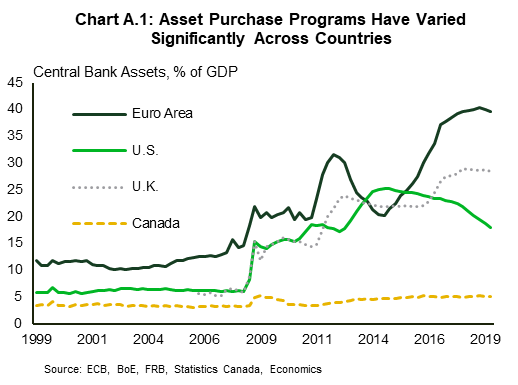

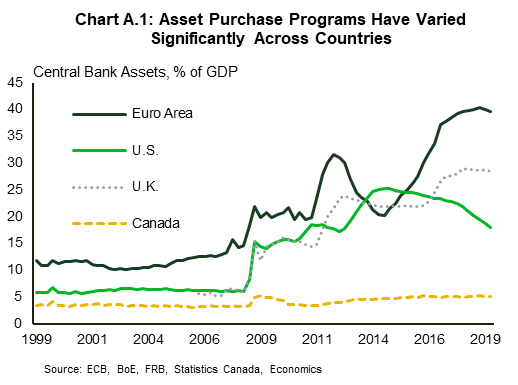

In the case of the U.S., asset purchases were initially designed to support the U.S. mortgage market. This was in large part due to the origin of the crisis. In November 2008, just two months after Fannie Mae and Freddie Mac went into conservatorship, the Fed initiated a program to purchase direct obligations of housing-related government-sponsored enterprises (GSEs) and mortgage backed securities (MBSs). This was followed by additional purchases announced in March 2009 (referred to as “QE1”), which increased its total assets from just over 6% of GDP in mid-2008 to close to 15% (Chart A.1). By contrast, the Bank of Canada did not initiate any asset purchase programs and its total assets have remained relatively stable as a share of GDP.

Subsequent asset purchase programs were initiated largely for country-specific reasons. For example, the Securities Markets Program (SMP) introduced by the ECB in May 2010 was designed to address “severe tensions in certain market segments which had been hampering the monetary policy transmission mechanism”. Purchases undertaken under the SMP increased the ECB’s total assets from 20% of GDP to a peak of 31.5% in mid-2012 when the program was terminated. The purchased assets were allowed to run off over the next two years as turmoil surrounding the sovereign debt crisis abated. Another example is the announcement by the Bank of England in August 2016 to initiate its third asset purchase program after the economic outlook deteriorated significantly following the “Brexit” referendum results in June.

Central bank asset holdings in the three regions have diverged over the past few years. The Fed began reducing its security holdings in June 2017 as part of its “Policy Normalization Principles and Plans”, bringing its asset holdings down to 18% of GDP in 2019Q2. Meanwhile, ECB assets increased from just over 20% of GDP in mid-2014 to 40% and are expected to increase further in the months ahead due to a new asset purchase program that is expected to purchase at least €240bn over the next twelve months. The Bank of England is currently somewhere in the middle, but this could change given the high uncertainty surrounding Brexit.

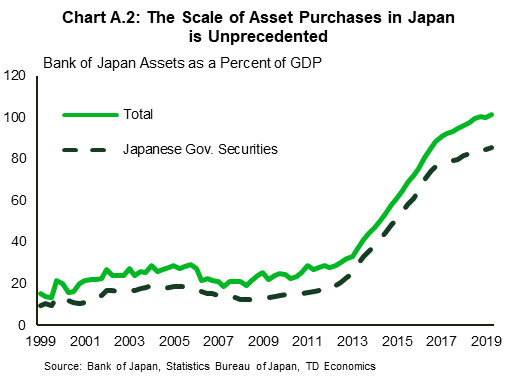

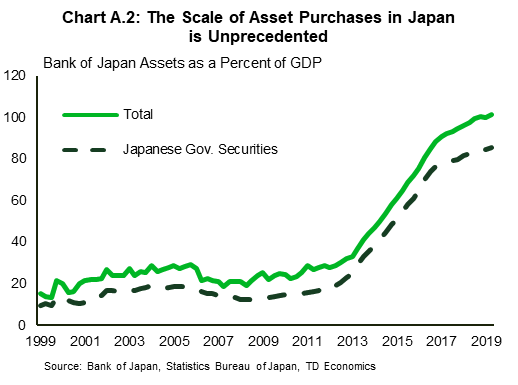

The Bank of Japan began experimenting with asset purchases all the way back in 1998, a full ten years before the global financial crisis. The initial programs were designed to address weaknesses in the banking sector that originated from the dramatic decline in real estate and equity prices nine years earlier. What really differentiates Japan from the other countries is the scale of the current “quantitative and qualitative easing” (QQE) program introduced in April 2013. Prior to that, the Bank of Japan’s assets were equal to 32% of GDP, comparable to the Euro Area (30%) at that time. Subsequent purchases have expanded the Bank of Japan’s assets to 100% of GDP (Chart A.2), well above current levels in the Euro Area (40%), the UK (28.5%) and the U.S. (18%). Purchases have been largely comprised of Japanese government securities, raising the Bank of Japan’s holdings to almost one half of the total amount outstanding (48.5% as of 2019Q2). Current holdings of corporate paper and bonds are relatively minor by comparison (less than 1% of GDP), but equity exchange traded fund (ETF) holdings have increased significantly (reaching 4.7% of GDP).

Appendix I: A brief history of negative policy rates

Denmark became the first country to explore negative policy rates in mid-2012.i The European sovereign debt crisis was at a critical juncture in late 2011 and into 2012 as Greece faced the possibility of exiting the Euro Area. Capital flows into “safe havens” brought short-term market rates close to zero in Germany and below zero in Switzerland. Capital inflows into Denmark and widening interest rate differentials put upward pressure on the krone against the euro, jeopardizing the fixed exchange rate regime. Denmark’s Nationalbank (central bank) responded by dropping the interest rate on its certificates of deposit to -0.20% to alleviate the pressure on the krone. It later made further reductions in its policy rate in step with the ECB, maintaining the fixed exchange rate regime.

The ECB adopted negative policy rates in June 2014 when the deposit rate was cut from zero to -0.1%, primarily to curtail disinflationary pressures (core CPI inflation at the time was at 0.7%, well below the 2% target).

Capital inflows and exchange rate pressures also played a central role in Switzerland. The Swiss franc appreciated against the euro by 13% between April and August 2011. In September, the Swiss National Bank (SNB) introduced a floor on the exchange rate to stem further appreciation. The floor held until the ECB adopted negative rates in June 2014. Exchange rate market intervention by the SNB could not contain pressures on the Swiss franc. In January 2015 the SNB was forced to abandon the exchange rate floor and reduced its policy rate to -0.75% to offset the economic impact of an impending appreciation. The Swiss franc appreciated by 13.7% against the euro over the subsequent four months.

The negative interest rate environment in Switzerland, Denmark and the Euro Area eventually spilled over into Sweden. The Riksbank (Sweden’s central bank) planned a gradual transition into negative territory, reducing its policy rate to -0.50% in February 2016 in three steps over a 12-month period. In December 2018, the Riksbank raised its policy rate to -0.25%, citing an improvement in the economic outlook.

The Bank of Japan was far more reluctant to explore negative policy rates as an additional element in their struggle to overcome deflationary pressures, which has been ongoing since the mid-1990s. In January 2016 the Bank of Japan introduced a tiered system for calculating interest on reserves that requires banks to pay interest (currently set at -0.1%) on reserves above a specified level.ii This had a relatively minor impact on short-term market rates, which remain well above rates in Switzerland, Denmark and the Euro Area. The Bank of Japan has left the door open for a deeper move into negative territory, if judged necessary.

- The Sveriges Riksbank (Sweden’s central bank) lowered its deposit rate to -0.25% from July 2009 to September 2010 but the amounts on deposit were very small and did not result in negative market rates.

- Japan actually has a three-tiered system, the middle tier of reserves has an interest rate of zero.

Appendix II: Key elements of asset purchase programs

The large scale asset purchase programs undertaken in the U.S., Euro area, UK and Japan were designed to different objectives which varied across countries and over time.

United States

The FOMC announced the first asset purchase program In November 2008, comprised of purchases of up to $100 billion in direct obligations of housing-related government-sponsored enterprises (GSEs) and $500 billion in mortgage backed securities (MBSs). The program designed to “reduce the cost and increase the availability of credit for the purchase of houses, which in turn should support housing markets and foster improved conditions in financial markets more generally”.

This was followed by additional purchases of $100 billion in agency debt, $750 billion in agency MBSs, and $300 billion in longer-term Treasury securities in March 2009 (which became known as “QE1”); the latter element was undertaken to “help improve conditions in private credit markets”.

“QE2” was introduced in November 2010, consisting of additional purchases of up to $600 billion in longer-term Treasury securities (QE2) to bolster the recovery. Core PCE inflation at the time declined below 1%, raising concerns of a deflationary trap.

In September 2011 the FOMC announced purchases to extend the average maturity of its holdings of securities (“Operation Twist”), undertaken to “put downward pressure on longer-term interest rates and help make broader financial conditions more accommodative”.

A year later the FOMC announced additional purchases of MBSs and further extended the average maturity of its security holdings (QE3) to “put downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative”

Euro Area

The ECB launched its first asset purchase program in July 2009, consisting of €60 billion in purchases of covered bonds undertaken over a 12-month period with multiple objectives:

“(a) promoting the ongoing decline in money market term rates;

(b) easing funding conditions for credit institutions and enterprises;

(c) encouraging credit institutions to maintain and expand their lending to clients; and

(d) improving market liquidity in important segments of the private debt securities market”

The Securities Markets Program (SMP) was introduced in May 2010 to address “severe tensions in certain market segments which had been hampering the monetary policy transmission mechanism”

A second covered bond purchase program was launched in November 2011, comprised of €16.4 billion in purchases over a 12-month period, with two objectives:

(a) ease funding conditions for credit institutions and enterprises; and

(b) encourage credit institutions to maintain and expand lending to their clients.

A third covered bond purchase program was launched in October 2014 to “further enhance the transmission of monetary policy, facilitate credit provision to the Euro Area economy, generate positive spillovers to other markets and, as a result, ease the ECB’s monetary policy stance, and contribute to a return of inflation rates to levels closer to 2%”

The public sector purchase programme (PSPP) was introduced in January 2015 “as part of the single monetary policy in view of a number of factors that have materially increased the downside risk to the medium-term outlook on price developments”

Purchases of corporate bonds were introduced in June 2016 to complement targeted LTROs in “further enhancing the transmission of monetary policy, facilitating credit provision to the Euro Area economy, easing borrowing conditions for households and businesses.”

United Kingdom

The Bank of England introduced its first asset purchase program in February 2009 by drawing on the Asset Purchase Facility (APF) to “enhance liquidity in financial markets and support credit growth”. The APF was a special fund indemnified by the Treasury, authorizing the Bank of England to purchase up to £150bn, £50 bn of which was earmarked for corporate bonds, the remainder for gilts (UK government bonds). The Monetary Policy Committee (MPC) initially authorized £75bn in purchases over a three-month period in March 2009.

The APF was replaced by the Asset Purchase Program (APP), which was expanded on three occasions, reaching £200bn in November 2009, to support household and business spending and attenuate downside risks stemming from weaknesses in the banking system and fiscal consolidation. The APP was expanded on three occasions, reaching £375bn in July 2012, to counter significant downside risks to the inflation outlook over the course of the European sovereign debt crisis. The APP was expanded to £435bn in August 2016, accompanied by an additional £10bn in purchases of UK corporate bonds, to provide stimulus as economic conditions deteriorated following the “Brexit” referendum result in June.

Japan

The Bank of Japan’s experience with asset purchase programs can be grouped into three periods.

The first program, initiated in November 1998, entailed purchasing commercial paper issued by financial corporations to support their efforts in reducing non-performing loans (legacy of the dramatic decline in real estate and equity prices dating back in the crash in 1989). This was followed by purchases of short-term sovereign bonds in October 1999, undertaken to enhance liquidity in the financial system. The program was expanded to include long-term government bonds in March 2001 when the economic outlook deteriorated with the policy interest rate already at the “zero lower bound”.

In March 2006 the Bank of Japan began reducing its asset holdings based on the (mistaken) view that the medium-term economic outlook had improved significantly, and a robust recovery was underway. The optimism turned out to be short-lived, especially when the global outlook deteriorated in late 2008 in the wake of the global financial crisis. By December 2008, the Bank of Japan initiated purchases of corporate bonds to improve financing conditions in the corporate sector. In December 2009 the Bank of Japan began purchasing Japanese government bonds and corporate paper under repurchase agreements, to instill confidence in financial markets and ease credit conditions in the wake of the global financial crisis.

The current “quantitative and qualitative easing” (QQE) program was introduced in April 2013 to address the risk of a deflationary trap, by reducing longer-term interest rates and instill investor confidence by supporting equity prices through purchases of domestic exchange traded funds (ETFs) and real estate investment trusts (REITs).

References

- Albertazzi, U., B. Becker, and M. Boucinha (2018), “Portfolio rebalancing and the transmission of large-scale asset programmes: evidence from the euro area”, ECB Working Paper No 2125..

- Altavilla, Carlo, Mariassunta Giannetti, Sarah Holton and Lorenzo Burlon (2019), “Is there a zero lower bound? The effects of negative policy rates on banks and firms”, ECB Working Paper Series No 2289.

- Basten, Christoph, and Mike Mariathasan (2018), “How Banks Respond to Negative Interest Rates: Evidence from the Swiss Exemption Threshold”, CESifo Working Paper 6901.

- Borio, Claudio, and Anna Zabai (2016), “Unconventional monetary policies: a re-appraisal”, BIS Working Paper No 570.

- Borio, Claudio, L Gambacorta and B Hofmann (2015), “The effects of monetary policy on bank profitability”, BIS Working Paper No 514.

- Borio, Claudio, and Leonardo Gambacorta (2017), “Monetary policy and bank lending in a low interest rate environment: diminishing effectiveness?”, BIS Working Paper No 612..

- Bräuning, F., and B. Wu (2017), “ECB Monetary Policy Transmission During Normal and Negative Interest Rate Periods”, Available at SSRN.

- Campbell, Jeffrey, Charles Evans, Jonas Fisher, and Alejandro Justiniano (2012). “Macroeconomic effects of Federal Reserve forward guidance.” Brookings Papers on Economic Activity 2012, no. 1 (2012): 1-80.

- Demiralp, Selva, Jens Eisenschmidt, and Thomas Vlassopoulos (2018), “Negative interest rates, excess liquidity and retail deposits: banks’ reaction to unconventional monetary policy in the euro area”, ECB Working Paper No 2283.

- Eberly, Janice, James Stock and Jonathan Wright (2019), “The Federal Reserve’s Current Framework for Monetary Policy: A Review and Assessment”, paper prepared for the Conference on Monetary Policy Strategy, Tools and Communication Practices, June 4-5, 2019, Federal Reserve Bank of Chicago.

- Eggertsson, Gauti, Ragnar Juelsrud and Ella Getz Wold (2017). “Are Negative Nominal Interest Rates Expansionary?,” NBER Working Paper No. 24039..

- Eggertsson, Gauti, Ragnar Juelsrud, Lawrence Summers and Ella Getz Wold (2019), “Negative Nominal Interest Rates and the Bank Lending Channel”, NBER Working Paper No. 25416..

- Eggertsson, Gauti, and Lawrence Summers (2019), “Negative interest rate policy and the bank lending channel”, VoxEU.org, 24 January 2019.

- Engen, Eric M., Thomas Laubach, and David Reifschneider (2015). “The Macroeconomic Effects of the Federal Reserve’s Unconventional Monetary Policies,” Finance and Economics Discussion Series 2015-005. Washington: Board of Governors of the Federal Reserve System, http://dx.doi.org/10.17016/FEDS.2015.005..

- Greenlaw, David, James Hamilton, Ethan Harris, and Kenneth West (2018). “A Skeptical View of the Impact of the Fed’s Balance Sheet.” National Bureau of Economic Research working paper 24687 (2018)..

- Heider, Florian, Farzad Saidi, and Glenn Schepens (2018), “Life below zero: bank lending under negative policy rates”, ECB Working Paper Series No 2173, August 2018..

- Kiley, Michael, and John Roberts (2017). “Monetary policy in a low interest rate world.” Brookings Papers on Economic Activity (2017).

- Kuttner, Kenneth (2018), ” Outside the Box: Unconventional Monetary Policy in the Great Recession and Beyond”, Journal of Economic Perspectives, Fall 2018, pp. 121–146.

- Lopez, Jose, Andrew Rose and Mark Spiegel (2018), “Why Have Negative Nominal Interest Rates Had Such a Small Effect on Bank Performance? Cross Country Evidence”, Federal Reserve Bank of San Francisco Working Paper 2018-07.

- Riskbank (2016) “How do low and negative interest rates affect banks’ profitability?”, Monetary Policy Report April 2016, pp. 20-23..

- Turk, Rima (2016), “Negative Interest Rates: How Big a Challenge for Large Danish and Swedish Banks?”, IMF Working Paper WP/16/198..

- US Board of Governors of the Federal Reserve System (2019), “Monetary Policy Rules and Their Interactions with the Economy”, Monetary Policy Report June 2019.

{kind=link}