Challenges

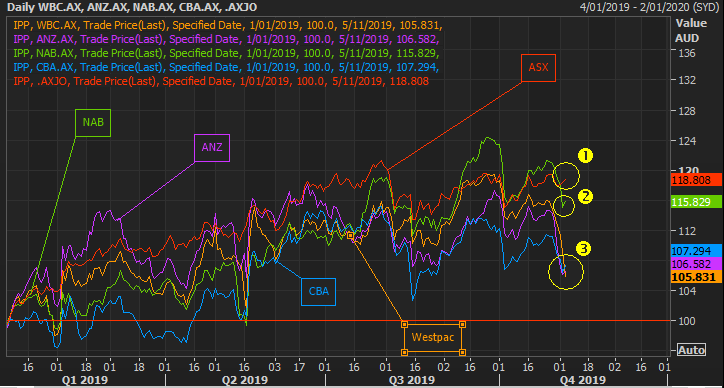

A cloud of near-term uncertainty hangs over the Aussie banking sector as a result of the low growth, low-rate environment which has so far garnered disappointing earnings across the Big 4. As a consequence, this has seen the likes of ANZ, CBA and Westpac significantly underperform the ASX 200, with NAB only marginally behind.

Indexed price performance of Aussie Big 4 banks starting Jan 1, 2019. Banks have underperformed. Source: Eikon

We flag a couple of profitability headwinds that might continue to put bearish pressure on the banks. This includes weak Aussie housing turnover and softer consumer credit growth which has driven smaller mortgage books. Not to mention the fierce competition competing for a smaller pool of mortgage loans – a key source of revenue. To add to that, lower net interest margins and therefore lower profitability has been a persistent concern off the back of the RBA’s easing cycle. It’s clear banks are also suffering from the customer remediation expenses that followed the government-backed inquiry into misconduct in the banking sector.

Opportunities

Despite the near-term challenges, we ask the question could Aussie banks be a worthwhile investment in the long-run at current prices – a question that inherently asks whether one thinks the Australian economy can pick-up beyond this year. After all, a strong Aussie economy tends to translate to a more robust banking sector.

And so, judging by the recent improvement in Aussie employment, inflation and the seemingly gradual pick-up in the Aussie housing market, we would think that it is entirely possible. We might for example see improved employment drive less slack in the labour market, higher wages, and in turn more demand for housing. Constrained housing supply combined with the current uptick in Aussie house prices also could incentivise more supply to come online. Mix that in with the potential of QE (better transmission of low interest rates to consumers) stoking housing demand; it’s not all doom and gloom.

At face value, ANZ seems relatively underpriced against its peers trading at a 6.7 EV/Rev, 9.68 P/CF and 12.39 PE.

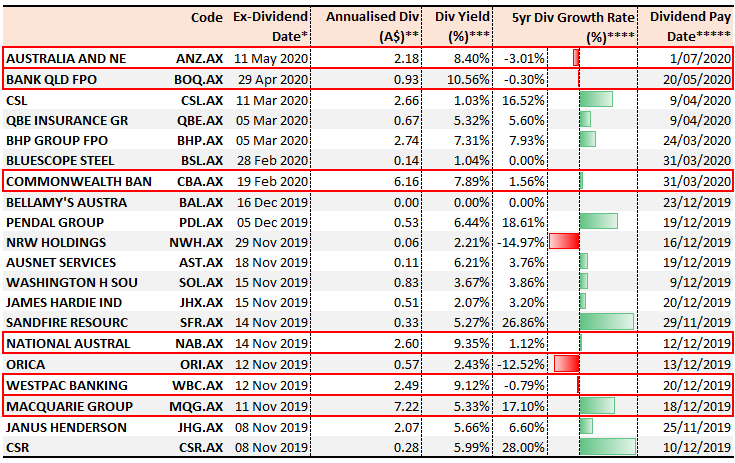

Upcoming dividends for Aussie bank stocks

We outline in red some Aussie banks stocks that are going ex-dividend in the next few months. They include Macquarie (11/11/19), Westpac (12/11/19), NAB (14/11/19), CBA (19/2/20), Bank of Queensland (29/4/20) and ANZ (11/5/20).