Stable, but for how long?

Equities overnight have somewhat settled and are trying to recover losses from a significant Monday sell-off which saw major benchmarks gap down at the week’s open. Risk-off flows seem to be slowly unwinding, headlined by Gold’s pullback into US$1,570, off session highs of some US$1,580 and USDJPY’s climb back into the 109 handle. Though, not for the lack of Coronavirus news flows.

It’s worth noting that there’s still plenty of concerns about Coronavirus’ end-game with travel between mainland China and Hong Kong suspended in the past 12 hours, and reports surfacing that Japan found the virus in a person who had not visited Wuhan. However, markets have clearly balanced this with a positive soundbite from a renowned Chinese respiratory scientist who says the outbreak may peak in 7-10 days.

Either way, it remains an incredibly tricky situation to trade and price-in the unknown nature of the virus. Confirmed cases are in the region of 4,500, but based on China’s track record for truth-telling – it’s likely to be understated. Our view is that risk meanders until there’s a clear path forward for China containment, or a far bigger distraction comes along.

Earnings season the cure?

S&P 500 futures have just about closed the gap overnight, climbing back to 3,280. As have most other benchmarks. ASX is poised to rally in the morning, though to a smaller extent of only ~38pts, likely as a result of its proximate nature to the epicentre of the virus. With markets in the thick of the busiest week of reporting season – how majors collectively report could be the impetus for a greater push back to all-time highs. But, in saying that, we favour US equities over SE Asia benchmarks given greater regional concerns at the present time.

Risk sentiment looks to be supported for now after a respectable beat from Apple (APPL), with the tech giant climbing 2% on beat revenue fuelled by strong iPhone demand and higher gross margins. However, the outlook for Q2 revenues was wider than expected at $63-67bn given Coronavirus uncertainties. This seemed to be the case as well with Starbucks (SBUX), which cited material earnings disruptions after having closed half of its stores in China.

Reports from Advanced Micro Devices (AMD) and eBay (EBAY) also hit the wires, but markets were less than impressed as extended trading saw both share prices lower.

Aussie calendar focus

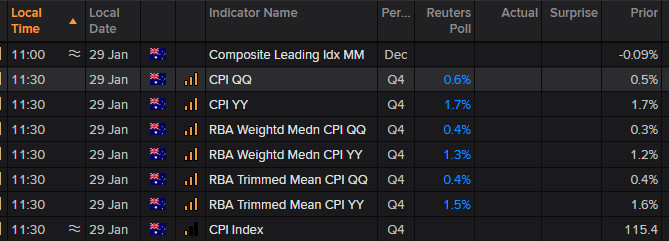

Stepping away from macro, the calendar looks quiet except for CPI risk (11.30am AEDT) ahead for Australia. After NAB business conditions slumped to a five-year low in Dec. from 0 to -2, AUDUSD continues to test November lows of ~0.6752 on the daily chart.

A big beat here cements the RBA on hold come February in line with market pricing, which only has ~6bps priced-in after modest job and wage growth numbers. It would take something disastrous to materially shift pricing such that the RBA would need to take notice. But it might be worth sitting on the bid at multi-month resistance if we get a beat here.

Downside risks and 2020 confidence should continue to be closely monitored, with expectations for a full rate-cut now fully priced into the RBA’s June meeting.